Let’s chat about the stock market. Specifically, let’s think about average investors like me and you. And let’s ask: how much money do we need to invest to become a millionaire?

First, we need to set some ground rules. It’d be easy to say, “If you invested in Apple stock in 2002, you could have 1000x‘d your money…boom, you’re a millionaire.”

But that’s not how reality pans out. In fact, we need to apply logical rules to our investing framework. The rules that I espouse on The Best Interest (and that matter for today’s article) include…

- Dollar-cost averaging. It’s too hard to determine when the market is overvalued or undervalued. Instead, the long-term investor should commit to a consistent investing schedule (e.g. $300 every month, or 10% of every paycheck, or $10,000 yearly). In fact, waiting to “buy the dip” is demonstrably dumb.

- Investing (in stocks) for decades. Simply put, stocks are not a short-term investment. They’re decades-plus. The data shows why.

- Diversifying, a.k.a. buying the whole market. History proves how challenging it is to find the “needle in the haystack” in the stock market. This article dives into further detail.

- Buy-and-Hold’ing. We don’t sell our investments when the headlines get scary. We hold. The past month has provided a terrific real-life example of why that is, as did the transition from 2022 to 2023.

- We reinvest our dividends. This rule is a bit in the weeds but a complete no-brainer.

Make sense? Let’s now put these rules to work. I went back to 1950 and grabbed all the S&P 500 data (which will act as our proxy for “the stock market”) through today.

Then I asked, “If an investor followed our rules, how much would they have needed to save and invest to become a millionaire?”

***Important note: I’m also inflation-adjusting all this data to 2023 values. Being a millionaire in 1950 was drastically different than being a millionaire today. Hence, everything you see below is adjusted to modern terms to make our understanding easier.

We know compound interest is a powerful tool, so we expect millionaire status to get progressively easier over longer investing periods. But we also know the market can be volatile. Two 20-year periods can provide drastically different investment returns.

So let’s compare 10-year periods against 20-, 30-, and 40-year periods. And we’ll look at all 10-year periods from 1950 to today (same for 20-, 30-, and 40-year periods) to show how much variability/volatility exists.

The Data: Becoming a Millionaire in the Stock Market

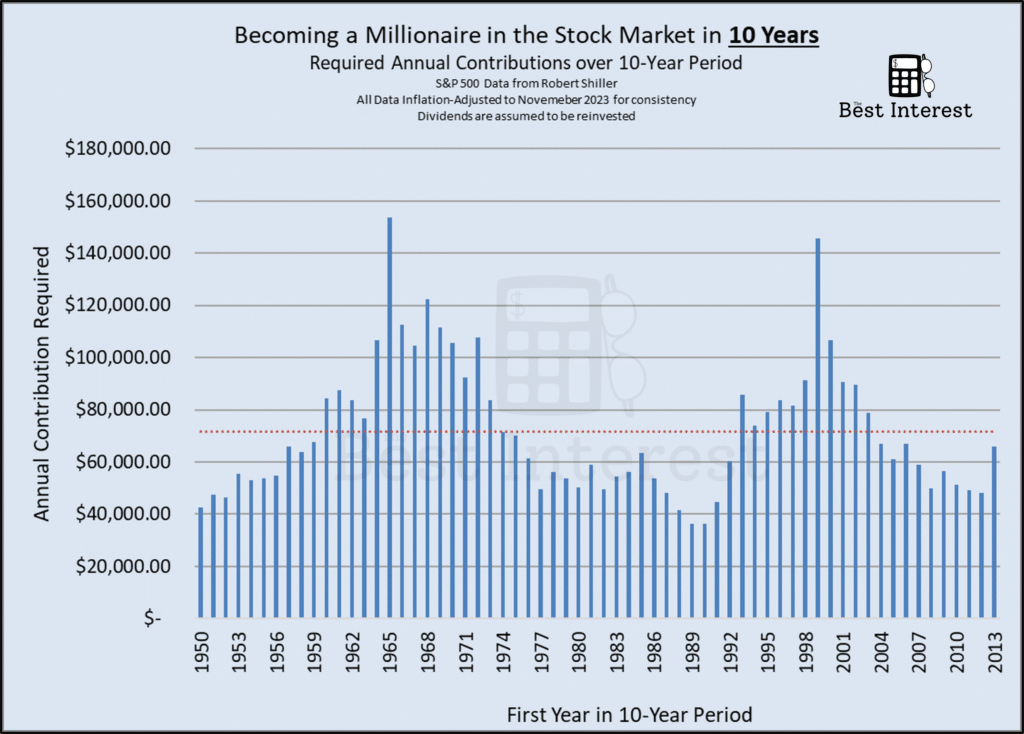

This chart shows every 10-year period from 1950 to today.

- We label each period by its first year; the X-axis shows that.

- We then look at the stock market returns for each period to ask, “What annual investment would have gotten us to $1 million over this period?” The Y-axis shows that dollar amount.

- e.g. the left-most bar represents the period from 1950 to 1959. Over that period, a $42,463 annual investment would have grown to a $1M portfolio.

For these 10-year periods, the average investor (the dotted red line) needed to invest $71,595 yearly to reach $1 million.

But the data that sticks out to me is the number of periods with a required investment above $100,000 annually. The 1965 and 1999 starting years are prime examples.

This is a glaring problem! If you’re investing ~$150,000 for 10 years (for a $1.5M total investment) and only end up with $1 million, you lost significant capital. Not good.

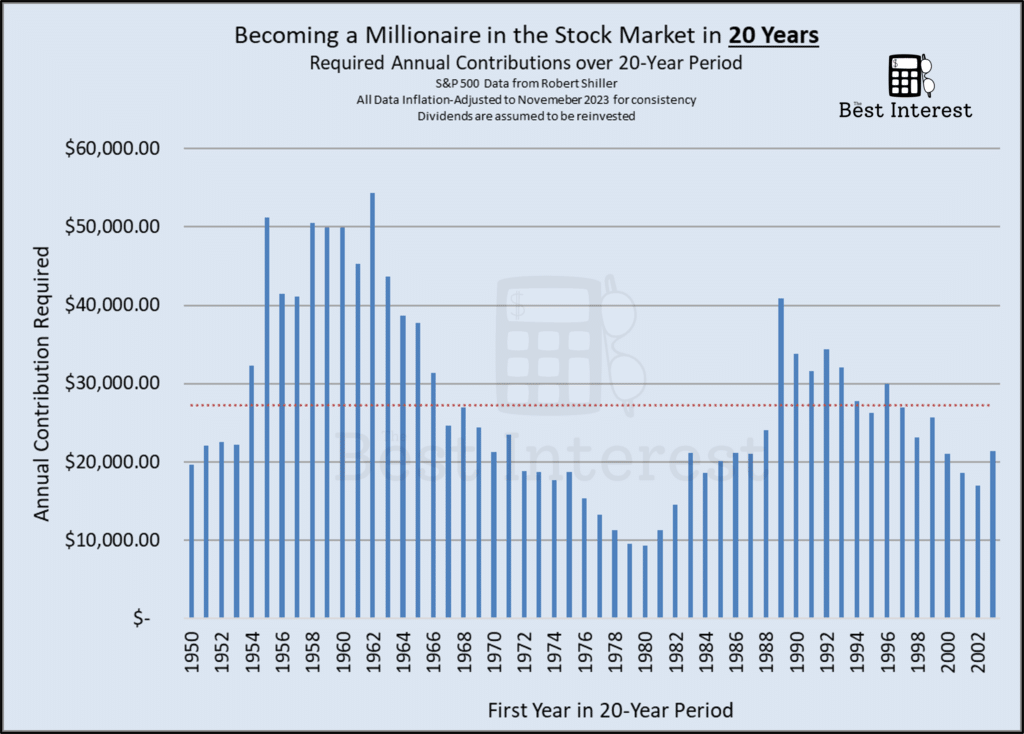

My takeaway: even over 10 years, the stock market can be volatile. We need to zoom out further. Let’s look at the 20-year data.

The average investor (in red) must commit $27,203 annually to become a millionaire. For those keeping track, that’s a $544,069 outlay over 20 years that grows into $1,000,000.

This data shows a few periods at or above the $50,000-per-year mark ($50K times 20 years = $1M). In other words, these periods showed near-zero, outright zero, or negative returns over 20 years. Examples include the period starting 1955, ’58-’60, ’62

But most periods provided legitimate, absolute returns. That’s great.

But can the average person save $27,203 per year? Then repeat that for 20 years? And this begs a bigger question that we won’t chase down today: is $1M the right goal in the first place. This is good food for thought.

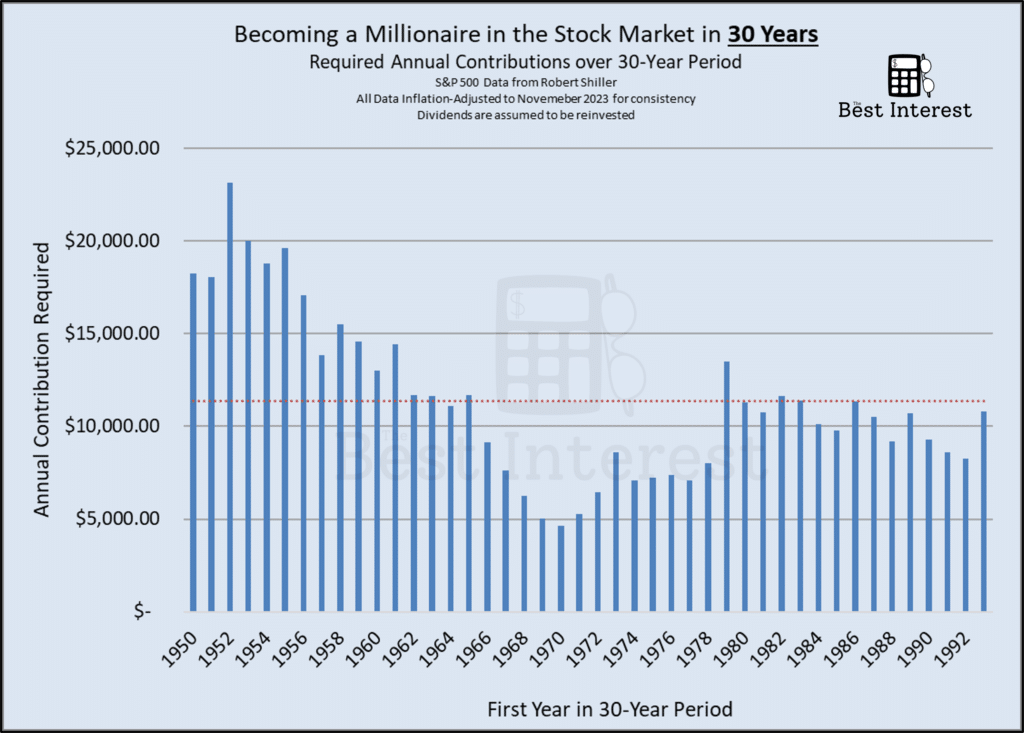

Let’s move on to the 30-year chart.

The average investor (in red) must commit $11,347 annually to become a millionaire. That’s a $340,432 outlay over 30 years that grows into $1,000,000.

None of these periods flirt with zero or negative returns. The “worst” period was 1952 – 1981, which required a ~$23K annual investment (or ~$695K total) to grow into $1M.

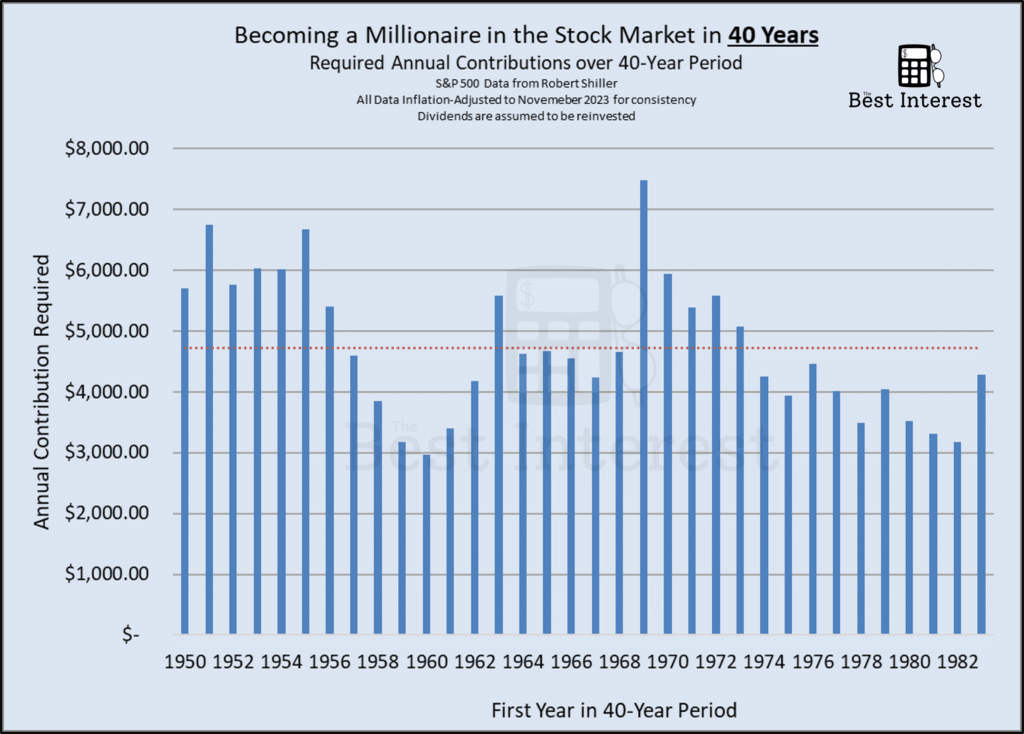

And finally, the 40-year data…

The average investor (in red) must commit $4725 annually to become a millionaire. That’s a $189K outlay over 40 years that grows into $1,000,000.

Again, none of these periods flirt with zero or negative returns. The “worst” period was 1969 – 2008, which required a $7500 annual investment (or $299K total) to grow into $1M.

The Power of Long-Term Investing

The 30-year and 40-year charts are particularly encouraging if you break them down into monthly terms.

$1000 per month is powerful.

- For most 30-year periods, $1000-per-month made you a millionaire.

- For all but three 40-year periods, $1000-per-month made you a multi-millionaire.

“But $1000 per month is a lot!”

I hear you. But between 401(k) contributions, employer matching, IRA contributions, after-tax investing, etc…$1000 per month is a reasonable goal.

If you’re in your 20s or 30s, set your baseline investing goal at $1000 per month. You’ll be setting yourself up for terrific long-term success.

What If You Don’t Have 3+ Decades?

If you’re reading this at age 50, you might not have 3 or 4 decades to wait for the stock market’s compound magic. What to do?

Let’s consult our trusty bucket method. Think about your current assets and savings based on when you’ll need them in the future…

- The money you need in your 50s –> Avoid the stock market. Too risky.

- The money you’ll need from age 60-65 –> you can introduce some stocks, but as we’ve seen today, positive returns aren’t guaranteed.

- The money you’ll need from age 66-70 –> stocks are becoming increasingly enticing…

- The money you’ll need from age 70+ –> 100% stocks is reasonable.

In summary, a fair portion of this 50-year-old’s assets should not be exposed to the stock market. Bonds, for example, are more appropriate.

Despite that, some of their money still has a 20-30+ year timeline. That money should be exposed to a risk asset like stocks.

Financial planning provides the backbone for these types of allocation decisions.

Just Start…

My investing journey started at age 22 with my first employer’s 401(k). Unsure what I was doing, I decided to learn.

11 years later, here I am.

There’s no guarantee the stock market will make me a millionaire. But history is on my side, and I’m controlling what I can (e.g. my monthly savings rate) to make it happen.

I encourage you to do the same.

Thank you for reading! If you enjoyed this article, join 8000+ subscribers who read my 2-minute weekly email, where I send you links to the smartest financial content I find online every week.

-Jesse

Want to learn more about The Best Interest’s back story? Read here.

Looking for a great personal finance book, podcast, or other recommendation? Check out my favorites.

Was this post worth sharing? Click the buttons below to share!