Hey mate! Have you written a post about what happens if you don’t reinvest your dividends? And the difference in account value over many years if you do or don’t reinvest?

-Joel

Awesome question, Joel. I haven’t written that. But after digging into the numbers, it could be a millions of dollar difference. So let’s dive in.

Highlights

- Dividend reinvestment is a simple idea with huge consequences.

- A typical investor – like you and me – is likely to see a 6- or 7-figure difference over our investing careers if we ensure we’re always reinvesting our dividends.

What are Dividends?

In May 2022, I wrote a take down of “dividend bros” who irrationally believe that high-dividend stocks are a panacea for investors. Yes, dividends are important. But the dividend bros are still wrong. I won’t beat that horse here, but you can read it for yourself via the link above.

An important stanza from that article will help us define dividends:

The fundamental value proposition in general stock investing is two-fold:

- First, we hope a company’s capital value increases. We want them to invent valuable intellectual property, buy land, build factories, earn more cash, etc. All this growth comes from them investing money, including their own earnings, wisely. We can then sell our stocks for capital gains.

- Second, we hope a company’s earnings increase. Some of those earnings will flow to us as part-owners of the company. Those payments to shareholders are called dividends. The dividends we receive today, tomorrow, and every day in the future add up to increase the net present value of the company.

Dividends, in short, are the profit payments that we receive as owners of a company. Dividends are one of the two main pillars of wealth creation for stock investors.

How are Dividends Received?

Dividends are typically paid out quarterly, and you might receive your dividends in a few different ways.

In the old days, you would have received a check straight from the company whose stock you owned. That doesn’t happen much anymore. Instead, you’re much more likely to receive a cash deposit straight into your brokerage account or IRA account.

If you own mutual funds or ETFs, the stocks in that fund will pay their dividends to the fund itself, and then you, as a fund owner, will receive your fraction of the dividends from the fund.

When you receive dividends in Taxable accounts, you owe taxes on those payments (recorded on a 1099-DIV tax statement). When you receive dividends in Qualified accounts (IRA, 401k, HSA, etc), you owe no taxes. Nice!

What is Dividend Reinvestment?

Investors have long faced a dilemma when receiving dividends: should they take the cash out of their investment account, or use the cash to buy more shares? This second option is called dividend reinvestment.

Some types of accounts automatically reinvest your dividends for you. Most 401(k) plans, for example, automatically reinvest dividends for their investors. But many IRA accounts and Taxable accounts do not reinvest automatically. Instead, you need to opt in to automatic dividend reinvestment. You might read or hear the term “DRIP” – dividend reinvestment plan – in these conversations. Check your accounts, and make sure you’re enrolled in DRIP (assuming you want to reinvest your dividends automatically).

But why? Why is dividend reinvestment so important? What’s wrong with taking my cash dividends and…ya know…buying that vintage armoire on Facebook Marketplace?

The Power of Dividend Reinvestment

Let’s dive into some data. Let’s look at the difference between two long-term investors (the best kind of investors), one who reinvests their dividends and one who doesn’t. As usual, I’m using the S&P 500 index as a proxy for “the stock market.”

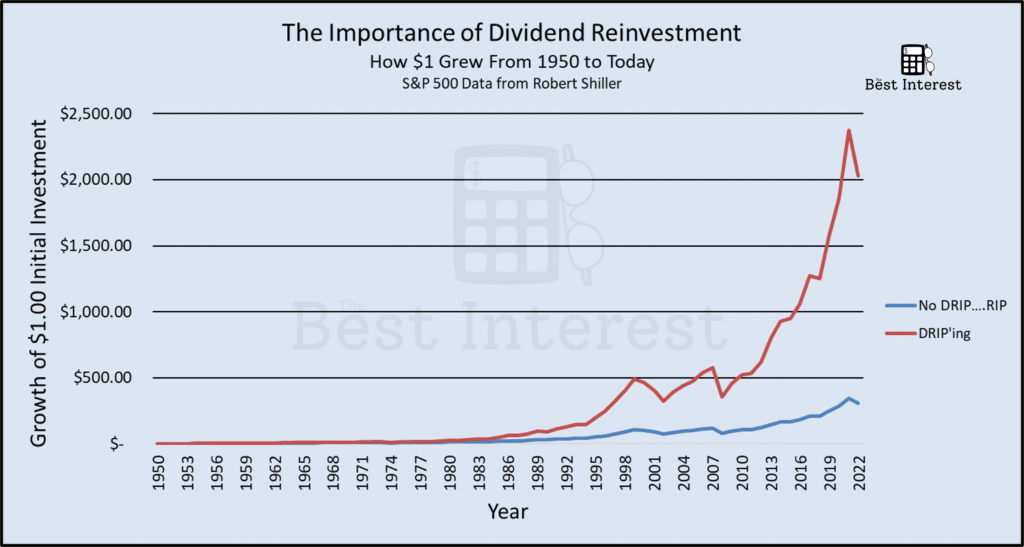

First, some grounding information. From 1950 to today, the S&P 500 price has grown at 7.8% per year, with an additional 3.2% per year paid out as dividend payments. Math majors, you’ll recognize that this sums to 11.0% total return per year. Nice! Of course, we know this 11.0% average belies a far more volatile market. The worst year for total returns was -38% and the best year was +46%. As this favorite-chart-of-mine reminds us: the average is not the actual.

But back to the topic at hand – 7.8% per year in price, plus 3.2% per year in dividends. How would that affect our two investors?

If our first investor invested $1.00 in 1950 and did not reinvest his dividends, his dollar would have grown to $236 in the stock market and he would have earned $68 in dividends, presumably now sitting as cash in his wallet. Not bad, right?

Our second investor, who does reinvest his dividends, would have seen that same dollar grow to $2026 in the stock market. Sure, he doesn’t have $68 in cash. But I think I’d take the $1790 extra in the stock market.

Note…these two charts show exactly the same data. But using a Log scale on the y-axis helps us understand their difference a bit better.

That’s the power of dividend reinvestment. That’s the power of compound interest. Small differences, when magnified over decades, turn into huge differences.

DRIPing and DCA

But here’s the thing: most of us don’t approach investing with an attitude of “here’s $1, let me wait 73 years.” Instead, we make regular contributions to our accounts (a.k.a. dollar-cost averaging, or DCA) and think in terms of a normal lifespan/workspan (e.g. a few decades.)

So how much does dividend reinvestment matter to an investor like that? Like us?

Let’s look at the same data as before – the S&P 500 from 1950 until today – and measure the returns of a two DCA investors, one dividend reinvestor and one not. Let’s assume both of our investors save $10,000 per year. Our non-DRIP investor ends up with a nice stock portfolio and a wad of dividend cash. The DRIP investor has only stocks…but a larger portfolio, we expect.

Over the various 30-year periods (e.g. 1950-79, 1951-80, etc.), the DRIP investor outperforms the non-DRIP investor (including both his stocks and his wad of cash dividends) by an average of $703,000, or roughly ~43%.

So yes – dividend reinvestment matters to everyday investors like you and me.

As I wrote earlier, your 401(k) is most likely already reinvesting dividends for you, but it’s worth double-checking. Your other accounts – IRAs, taxable accounts, etc. – might not be reinvesting your dividends. Go fix that! Because while dividend payments might feel like “free money” or a nice bonus income, I’d rather have the extra $703K.

Wouldn’t you?

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

100% agree with this article’s point on the power of dividend reinvestment. However, to generate substantial residual income through dividends, one would need to build a diversified portfolio of dividend-paying stocks and consistently reinvest those dividends – not to mention have the free-cash/capital to fully realize the benefit of a sustainable passive income. It takes time and disciplined investing, but it’s a proven strategy to boost long-term wealth.

Time and consistency – 100% agree with you, Jonnie.