Don’t miss an episode of our podcast, Personal Finance for Long-Term Investors. Available on all podcast players.

Here’s the latest episode:

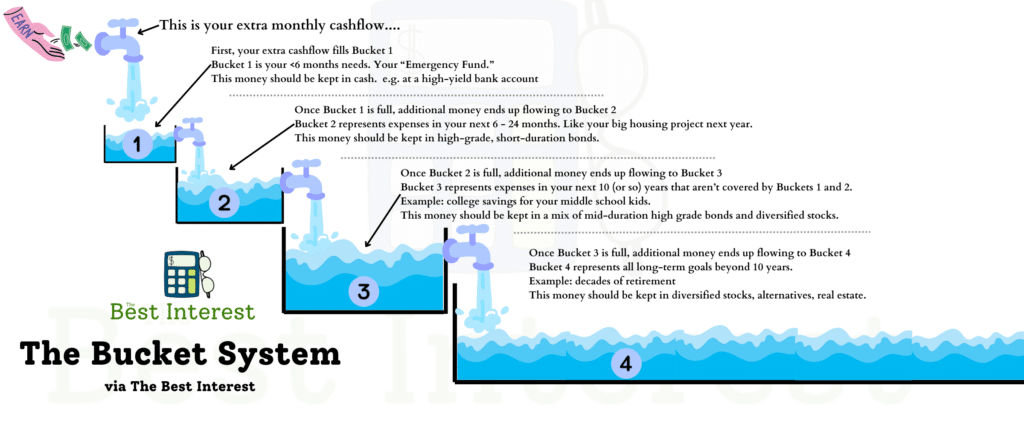

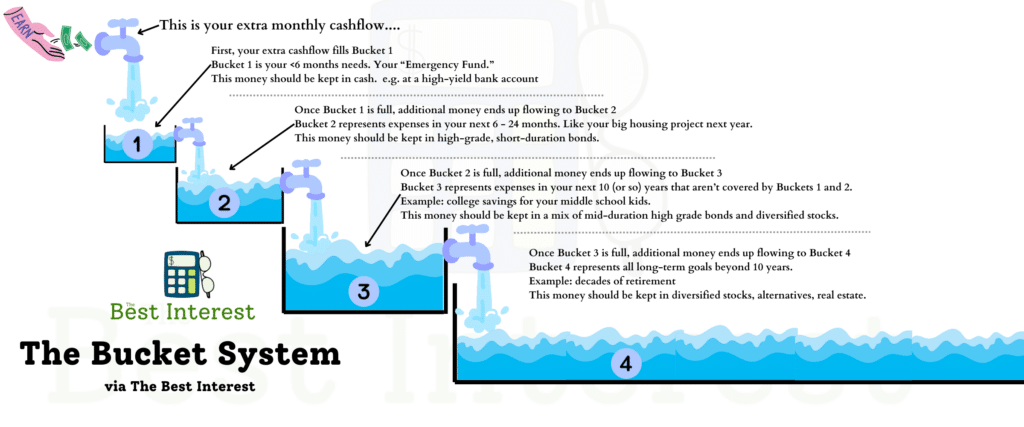

An easy way to level up your finances is to bucket your money.

What’s bucketing? It’s a mental accounting trick that helps both your objective financial plan and your subjective financial mindset.

And it’s really simple to implement.

We’ll start by dividing your liquid net worth (cash, stocks, bonds, etc., but not your home equity, car, or other material goods) into four buckets. These buckets look slightly different if you’re still working or retired, so let’s start with someone who’s still working.

Still Working

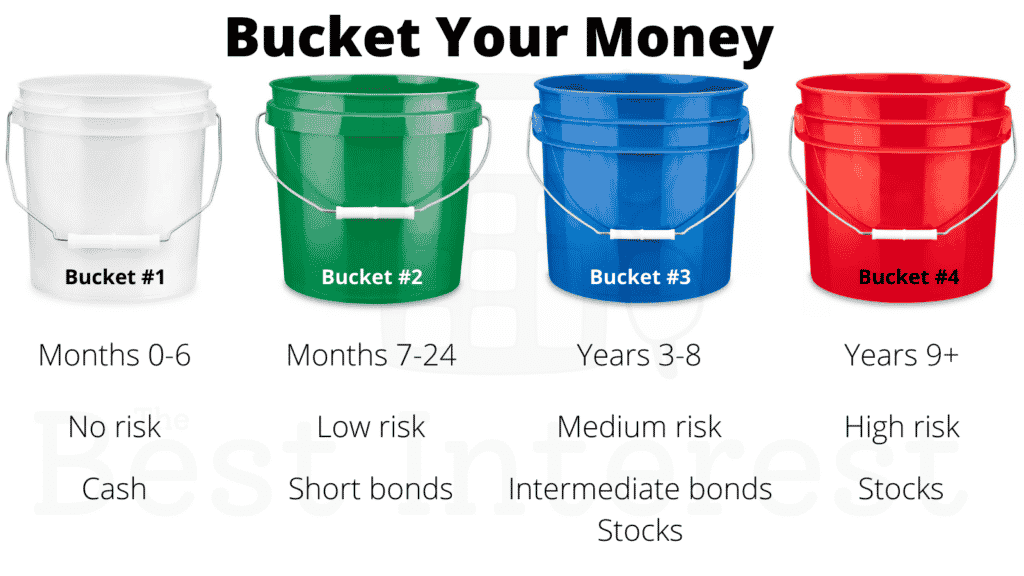

If you’re still working, your buckets are:

- Bucket #1: your next ~6 months’ expenses

- Bucket #2: any big savings goals for the next 1-2 years.

- Bucket #3: any big savings goals for the next 3-10 years.

- Bucket #4: all money beyond 10 years, including retirement savings

If You’re Retired

And if you’re retired, your buckets are:

- Bucket #1: the next ~6 months’ expenses

- Bucket #2: month 7 through Year 2’s expenses

- Bucket #3: Year 3 through Year 10’s expenses

- Bucket #4: all money to be spent beyond Year 10

What To Do With The Buckets?

Now you’re asking: what do we do with each bucket?

We invest them. But we don’t invest them equally. The timeline of the bucket dictates the investment risk we can take. Short-term buckets should be invested in a low- or no-risk manner. Long-term buckets should be invested with more risk, pursuing more reward.

Bucket #1 is about near-term spending. It should be cash. It needs to be liquid and dependable since you need that money in the short term. You can’t put these dollars at risk.

Bucket #2 (next 2 years) can take some risk, but not too much. You need to feel confident that your investment will maintain value (or grow slightly larger) in just two years. Short-term bonds or certificates of deposit make sense here.

Bucket #3 permits even more risk. We have 3 to 10 years to achieve investment growth. A mix of intermediate-term bonds and stock funds can be appropriate here.

And Bucket #4’s long timeline permits the most risk. Most of this money won’t be spent for multiple decades. Stocks are an ideal asset in this bucket.

My Money Don’t Wiggle…

There’s wiggle room on the timeline for each bucket.

Some people think Bucket #1 only needs to be 3 months’ expenses. Others argue it needs to be at least 12 months.

Similar arguments can be made for each bucket. A year here or there. More or less risk in each bucket. This is the soft science of financial planning.

Feel free to tweak your buckets. But maintain the overall idea.

Let’s walk through a few examples.

Example #1: A Typical Young Family

Let’s talk about the Johnsons, a 40-year-old couple.

- They have two children, ages 12 and 8.

- Their household spends $6,000 per month.

- Both parents are still working.

- They expect one of their cars has ~2 years of life left

- Their older child will be starting college in 6 years.

Based on this information, Bucket #1 contains 6 months of spending, or $36,000. It’s in a high-yield savings account (cash) at a bank.

Bucket #2 contains about $35,000 for their next car. That money is invested in 2-Year Treasury notes (AAA-rated, backed with the full faith and credit of the U.S. government) earning 3% per year.

Bucket #3 has $150,000 earmarked for the first 3 years of college payments (years 6, 7, and 8 from now). That money is split between 5-year Treasury notes earning 3.3% per year and stock index funds.

Bucket #4 has another $300,000—the rest of the Johnsons’ liquid assets, including their IRAs and 401(k) accounts. It’s 100% invested in stock index funds—about 70% US-based companies and 30% international companies. Most of this money is retirement money that can’t be touched for another 20 years.

Since the Johnsons maintain a budget, they know their dual incomes can cover all of their day-to-day spending.

Bucket #1 is there in case of emergency. It’s a safety net.

The remaining 3 buckets are allocated based on the Johnsons’ clear-cut goals and timelines. If their goals or timelines change, the dollar amounts in these buckets will change.

You might wonder, “What about the Johnsons’ earnings? Where does ‘new’ saved money go?”

Great question. The answer is:

- Go bucket by bucket, starting with Bucket #1

- Ask, “Is the money needed here?”

- If it’s not needed in Buckets #1-3, then it goes to Bucket #4

The Johnsons’ first three buckets are fully funded for their goals. Their new savings don’t need to go into those buckets. So it’s placed into Bucket #4 and invested in the stock market.

We can zoom out on the Johnsons’ total portfolio allocation:

- $36,000 cash, or 7% of their liquid net worth

- $135,000 bonds, or 26%

- $350,000 stocks, or 67%

This portfolio is in-family with a traditional 70/30 portfolio, but we built it from the ground up based on the Johnsons’ unique circumstances.

Example #2: The New Retirees

The Smiths, age 62, just retired. Here are some of their stats:

- They have $1 million in their 401(k)s and IRAs.

- They plan on spending $50,000 per year in retirement.

- For their first five years of retirement, 100% of their spending will come from their savings.

- They’ll start collecting Social Security at age 67 (“full retirement age”), which will cover half of their spending needs thereafter.

The Smiths’ Bucket #1 contains $25,000 in cash for the next 6 months of spending.

Bucket #2 contains $75,000 for the following 18 months of spending, and it’s invested in 2-Year Treasury notes.

Bucket #3 contains $275,000 total. $150,000 is for Years 3-5, before the Smiths start collecting Social Security. $125,000 is for Years 6-10, when half of their income will be supplied by Social Security. This $275K is split between 5-Year Treasuries and stock index funds.

Bucket #4 contains their remaining $625,000 and is invested in stocks.

If we zoom out on the Smiths’ portfolio, we see:

- $25,000 cash, or 2.5% of their liquid net worth

- $250,000 bonds, or 25%

- $725,000 stocks, or 72.5%

After their $25K emergency fund, the rest of their investments are roughly 75/25 portfolio—which is traditionally aggressive for two retirees.

But we must consider that their Social Security can be considered fixed income, just like bonds. If we were to “add” their Social Security fixed income into their 25% bond allocation, we would see their portfolio ratio shift significantly.

$25,000 in Social Security income is equivalent to owning $700,000 in bonds paying 3.5% per year [here’s how to consider Social Security as a lump sum asset.]

$25,000 cash, or 2% of their net worth

$225,000 bonds + $700,000 equivalent in Social Security = $925,000 in fixed income = 54%

$750,000 stocks = 44%

Ah! The Smiths’ portfolio, including Social Security, resembles a 45/55 portfolio. That’s much more “in family” with traditionally prescribed retirement portfolios.

The difference, however, is that we built the Smiths’ portfolio from the ground up, using the bucket method.

How to Bucket Your Money

Use the examples of the Johnsons and the Smiths to bucket money in your life.

- Determine your goals

- Apply a timeline to them

- Allocate money to each goal

- Take risk based on the required timeline

Depending on your age and your goals, you might find a unique proportion of money inside your buckets. That’s ok! The point of this exercise is to build a portfolio unique to your life, using an objective, goals-based framework.

Every ~6 months, revisit your buckets to ensure your portfolio is still aligned with your buckets.

You’ll have an objectively smart financial plan, and a subjectively easy method of mental accounting.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

The bucket system worked great before retiring.

Now retired with a pension and social security.

These more then covers annual expenses with cash leftover…

Is it best to leave retirement accounts in index etf and let it ride?

If your fixed income (pension + SS) covers all your expenses, then you need to answer a fun question:

What are your plans with all the savings / investments you have? How will you spend that money, whether in life or in death?

You can’t look at social security as part of your portfolio as you dont have access to the entire amount.

Well Bill…yes and no. Please read this and let me know your thoughts:

https://bestinterest.blog/valuing-social-security-as-an-asset-in-your-retirement-plan/

Jesse,

Your bucket diagram above starts with “extra monthly cash flow.” If you are in retirement and your cash flow equals your cash flow need (e.g., you’re using SS + distributions from dividends & cap gains for living expenses. What is the recommended approach(es) to refill your buckets?