- High reward comes from taking risks

- Small risks or no risk lead to small rewards

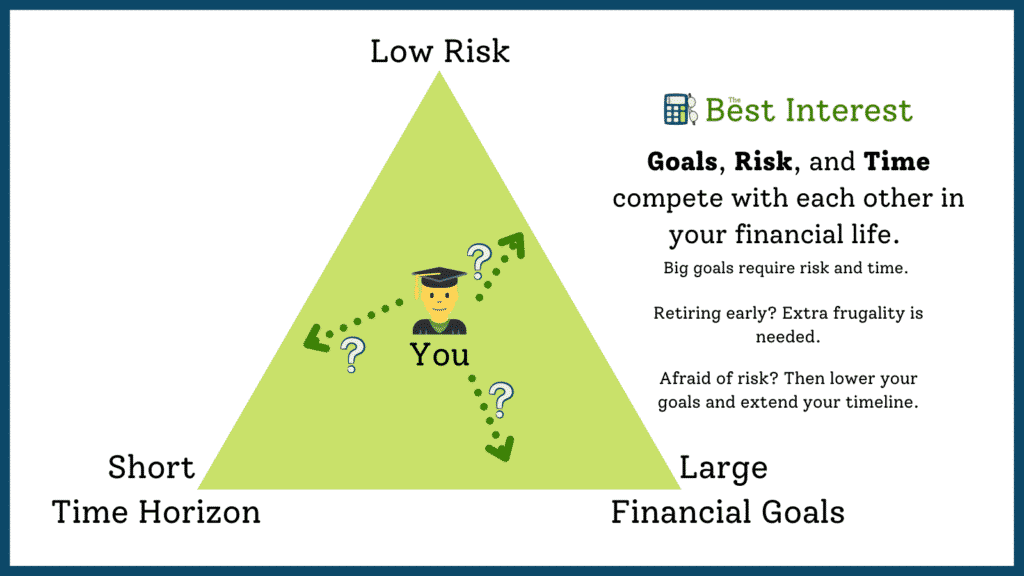

- You can control your risk preference, your time horizon, and your financial goals. But if you demand satisfaction from all three, you might be disappointed.

- People searching for the “low risk, high reward” investment are seeking the mythical “free lunch”

There ain’t no such thing as a free lunch.

– Common investment saying from the 1930s

- ……though diversification might be that free lunch you’re looking for

Risk and Reward are Correlated

All investments come with risk.

What does that mean? How do we define risk?

It varies. But the popular definitions are:

- Risk is the probability of permanent harm or injury.

- Risk is relative to time horizons. A choice can be risky in the short-term, but less risky long-term (or vice versa).

- Risk is related to volatility (though Warren Buffett disagrees)

Risk is scary. We don’t want to lose our money! And risk implies we might do just that.

So when faced with a risky investment, the intelligent investor says, “I demand a bigger reward. If I’m going to take this big risk, I need to earn a big return.”

This leads to an essential relationship in investing between risk, reward, and price.

Risk is built into the investment itself. Reward is something that investors must demand. And they make these demands via the price that they’re willing to pay.

When a reward overcompensates for the risk, intelligent investors will pour their money in. When a reward doesn’t justify the risk, intelligent investors will sit on the sidelines. This demand (or lack thereof) will push the price up (or down).

In other words, price acts as an equilibrium mechanism between perceived risk and expected reward.

The chart below (via Howard Marks) illustrates this relationship for popular asset types. Risk-free bonds (e.g. Treasury bonds) are backed up by the full faith and credit of the U.S. government, and are considered to have zero risk. They also have the lowest reward.

As we move towards the right, we encounter higher-risk assets. These assets could suffer permanent loss of capital, or even go to zero. Therefore, investors demand higher rates of return.

But there’s another way to view this same concept.

We can view the “risk equals volatility” definition below (again, from Howard Marks). Low-risk assets tend to have low volatility. Their values stay near their original purchase price. But as risk increases, so does volatility—even to the point where an asset could go to zero (crossing the x-axis of the plot), losing 100% of all investors’ dollars.

What Can You Control in the Risk vs. Reward Relationship?

You have financial goals and a preferred time horizon to meet those goals. Ideally, you can adopt a particular risk preference to do just that—to meet your goals on time.

But people—including my readers—have run into trouble when:

- Their goals are too lofty

- Their time horizon is too short

- Or their risk preference is too conservative.

Everyone wants a high return for no risk. They want the proverbial “free lunch.” But it doesn’t exist.

If you need high returns (due to lofty goals or a short time horizon), then you need to take risks.

If you can’t stomach the risk, then you need to soften your goals or lengthen your time horizon.

Robert is 30. He earns $80,000 a year and saves 20% of that. He wants to retire with $1.5 million dollars at age 60, and he doesn’t mind some volatility along the way.

He has a long time horizon, reasonable goals, and is willing to take on risks.

Robert’s in good shape. He has flexibility in the triangle diagram above. This spreadsheet shows how Robert can reach his goals—even after adjusting for inflation—by investing as simply and conservatively as a traditional 60/40 portfolio.

Diversification *Is* A Free Lunch

I’ve neglected to tell you one secret.

There is a way to reduce portfolio risk while maintaining returns. The secret is diversification.

“Diversifcation is the only free lunch.”

Harry Markowitz

A well-constructed portfolio is less risky than the sum of its parts. This is the essence of modern portfolio theory, for which Harry Markowitz won a Nobel Prize in Economics.

The idea is to create a portfolio of risky assets, but to ensure those assets are non-correlated or anti-correlated. In other words, to ensure that the various assets do not rise or fall in tandem with one another.

Markowitz proved that a diverse portfolio has the same expected returns as a non-diverse portfolio, but at significantly less risk. Less chance of going to zero. Less volatility. This can be measured using the Sharpe ratio, the most widely-accepted measure of risk and reward.

Portfolios on the “efficient frontier” represent the best possible expected return for a given risk level.

![Harry Markowitz's Modern Portfolio Theory [The Efficient Frontier]](https://www.guidedchoice.com/wp-content/uploads/2017/07/mpt-image-2.jpg)

Criticisms of Diversification and Modern Portfolio Theory

Diversification is not without detractors.

First, there’s the “math vs. reality” argument. Modern Portfolio Theory looks great on paper, in the world of pure math. But critics argue that MPT isn’t as effective in the real world, where the psychological irrationality of Mr. Market is at play.

Next, some claim that diversification isn’t enough. Nobel winners Eugene Fama and Ken French are proponents of factor investing. In short, factor investing says, “Rather than looking purely at risk, are there other variables that lead to extra rewards?” For example:

- Size: small-cap stocks tend to outperform large-caps

- Relative Price: value stocks tend to outperform growth stocks

- Quality: high profitability ratio companies tend to outperform low profitability ratio companies

- Momentum: rising stocks tend to keep rising, falling stocks tend to keep falling.

MPT ignores factor investing. That might not be smart.

There’s even criticism from investing legends like Warren Buffett and Charlie Munger. They claim that MPT is an invitation to buy sub-optimal stocks in the pursuit of diversification. Rather than own 50 companies, they say, just own the best three. Ignore the 47 worse ones.

(How to identify which three are the best three? That’s what makes Buffett and Munger unique investors.)

Risky Business

Risk and reward are intrinsically connected. As risk increases, investors demand more reward.

In your investing life, you can control your risk, your goals, and your time horizon. But it’s impossible to optimize all three. You’ll have to sacrifice one in pursuit of another.

And while there’s no free lunch, diversification comes close. A well-constructed portfolio can provide investment returns at reduced levels of risk.

Any questions? Don’t hesitate to reach out!

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

Question on this statement from above “When a reward overcompensates for the risk, intelligent investors will pour their money in. When a reward doesn’t justify the risk, intelligent investors will sit on the sidelines.”

1. What makes an intelligent investor, and how do they know when a reward overcompensate the risk or when to sit on the sidelines?

I think if there was an easy or right answer to that we could all be rich! The efficient market theory would suggest that if there was a right answer everyone would know it and the opportunity for profit would be gone.

Early in my investing career I wanted high rewards and was willing to let them ride for the long-term, but the companies I invested in went under. So in my experience a long time horizon was not very good at mitigating the risk. I agree with the idea that diversification is only free lunch in the investing world. My current investment plan of index investing provides that and corrects my problem of trying to pick companies that will not go under in the long-term. My returns are only going to be average, but I haven’t been able to see a better way to balance risk and reward.

An “intelligent investor” is a Buffett, a Graham, a Lynch…there aren’t many of them 🙂