Don’t miss an episode of our podcast, Personal Finance for Long-Term Investors. Available on all podcast players.

Here’s the latest episode:

All too often, I speak with current or future retirees who think along these lines:

- “We don’t want to assume Social Security will be there for us. Let’s just focus on the assets in our control.”

- “I know Social Security is there, but it’s so small. Let’s play it safe and ignore it for now.”

- “Social Security is only $2000 monthly, whereas my IRA has $900K. Social Security is a drop in the bucket.”

These ideas are not only wrong but perilously so. To overlook Social Security is an unreasonably conservative retirement assumption.

In fact, when I reframe Social Security in a different light, people change their minds (almost) every time. They realize, “Oh man – Social Security is huge. I never knew…” It’s a gift that keeps on giving.

I’m going to walk you through that reframing today. In your retirement plan, we must value Social Security as an asset (and a valuable one at that!).

Will Social Security Be There?!

Will Social Security still be there in 5, 10, 20+ years?

Yes. I have no doubts, and I’ll explain why. But will it look exactly the same as it looks now? Quite possibly not.

To understand why, we need a quick primer on Social Security:

- Most of the government’s annual Social Security outflows (~95% in 2022) are covered by current-year Social Security tax inflows.

- That difference (~5% in 2022) is withdrawn from the Old Age and Survivor’s Insurance (OASI) trust fund. It’s a band-aid to bridge the gap.

- That “band-aid” is growing each year and will continue to do so under current legislation.

- With ever-growing band-aids, the trust fund is on a trajectory to be fully depleted by 2034.

Most people hear those facts and think, “This is an unmitigated disaster…no more Social Security by 2034!?”

However!!!

They forget about the first bullet above. Most Social Security outflows are covered by annual taxes. As of 2034, roughly ~80% of the projected annual Social Security outflows will be covered by tax inflows. Social Security would not disappear completely; instead, the shortfall would only deliver 80% of what was promised.

Of course, paying less than full benefits is not an acceptable way to run this vital program, and Congress will need to act to fix it. My simple brain sees two solutions: increase inflows (more tax) or decrease outflows (higher Social Security age). But they haven’t asked me yet…

My point remains: Social Security will still be there.

The “Lump Sum” of Social Security

Now – let’s find a way to value Social Security as an asset in our financial plans.

The average Social Security benefit for a retired couple is $3800 per month. However, most assets on our balance sheets are lump sums, not income streams. How do we view our Social Security income streams as “lump sums” to make them comparable to an IRA or a bank account?

The 4% rule is a good start.

The 4% rule helps us equate a $1,000,000 portfolio to a $40,000 annual income stream. Let’s just use that math in reverse. Of course, there are caveats involved. Namely, the 4% rule is built for 30-year timelines and is conservative.

Does the average person live 30 years after starting to collect Social Security? No!

The average 65-year-old American male has another ~19 years of life left, and the average 65-year-old American female has another 22 years left. For more info, here’s a quick primer on life expectancy data. We’ll round those numbers to 20 years.

For that 20-year timeline, instead of the 4% rule, we’re better off using a 6% rule (which, if you’re curious, seems reasonable based on my playing around with Engaging Data’s X% Rule calculator).

When we do that math, our $3800 per month Social Security income stream (or $45,600 per year) is equivalent to a $760,000 portfolio that we’re drawing down at 6% per year.

That’s right. The average newly retired American couple’s Social Security payments are equivalent to having an additional $760,000 in their nest egg.

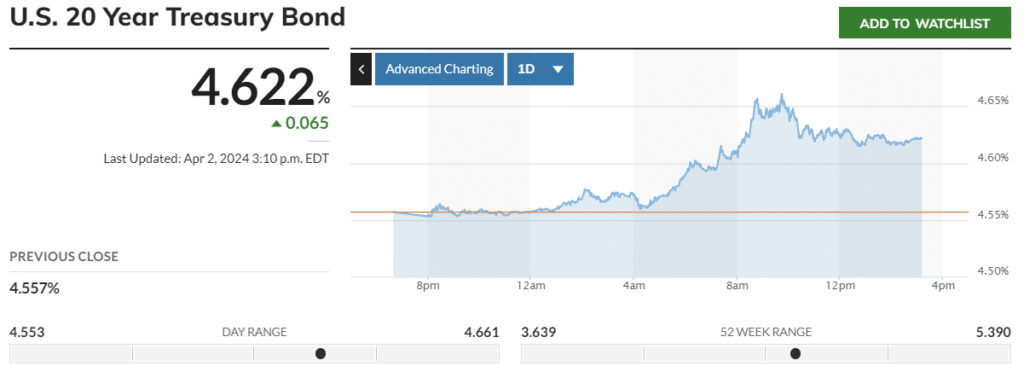

The Treasury Bond Method

But since Social Security is a guaranteed payment, perhaps a better proxy than the 4% Rule (or 6% Rule) is to use a U.S. Treasury bond, backed by the full faith and credit of the U.S. government? In other words, how do I recreate an average couple’s ~20-year Social Security income stream using 20-year bonds?

As of my writing this, the 20-year US Treasury rate is about 4.62%.

The question to ask is…

- If I had guaranteed 4.62% for the next 20 years…

- And I needed to pay myself $45,600 inflation-adjusted (like Social Security does) for the next 20 years…

- How much in bonds would I need to buy today?

The answer is ~$755,000. Here’s the Google sheet showing this math.

For what it’s worth, the fact that $755,000 is so close to our 6% rule answer of $760,000 is pure coincidence. While it’s nice the numbers are close together, I don’t think we should view that fact as evidence that the number must therefore be accurate.

For example, if today’s 20-year bond rate was 4.00%, the lump sum number would be $801,000

If the 20-year rate was 5.00%, the lump sum number would be $728,000

Does Delaying Matter?

What if a person decides to delay Social Security to a later age, thus increasing their monthly benefit? Or if they’re forced to draw Social Security earlier than desired, decreasing their monthly benefit? How does this affect the lump sum value?

In short, there’s minimal effect. The actuaries have you beat (mostly), though the actuarial data is a bit outdated.

As Wikipedia says, an actuary “is a professional with advanced mathematical skills who deals with the measurement and management of risk and uncertainty. The name of the corresponding field is actuarial science which covers rigorous mathematical calculations in areas of life expectancy and life insurance.”

The actuaries at the Social Security Administration have the job of making Social Security fair and un-rig-able. Your Social Security benefits will increase if you wait until age 67 or age 70 precisely because those actuaries know that, on average, you’ll have fewer years to collect them.

Higher rate x fewer years = lower rate x more years.

Now, the Social Security actuaries last updated this math in 1983. Life expectancies have increased since then. And because we’re living longer, the average person would benefit from delaying their Social Security until age 70. It’s not a huge difference, but it’s there. Until the actuaries update their math, this fact will remain true.

Of course, the joke in financial planning is, “Tell me when you’ll die, and I’ll tell you when to start collecting Social Security.” We just don’t know.

But the rough outline is:

- If you die before age 77, then collecting as early as possible would have been best.

- If you die between ages 78-80, then all scenarios are roughly equal (all within ~6% of one another)

- If you die after age 80, then waiting until at least “full retirement age” of 67 has distinct advantages

- If you die after age 84, then waiting until the maximum collection age of 70 becomes optimal, and it only gets better the longer you live. For example, if you die at age 90, then collecting at age 70 would have been ~28% better than collecting at age 62.

Here’s my Google sheet if you want to play around with it yourself.

Quick aside: there is another set of “hacks” worth knowing on this front.

If you have reason to believe you’re likely to live shorter than average (family history, preexisting conditions, etc.), you should consider collecting your Social Security income as early as possibly.

And vice versa. If you’re likely to live a long life, you should consider waiting on Social Security income until full age 70.

If a couple wants to hedge their bets, the lower earning partner should collect Social Security has early as possible, and the higher earning partner should wait as long as possible. This is because the lower earning partner will inherit the larger benefits should the higher earning partner die first.

Social Security As Part of a Portfolio

How does Social Security income fit into overall portfolio construction?

I like to think of portfolios from a bottoms-up, goals-based allocation perspective. From that point of view, Social Security income reduces the short-term income needs from our portfolio, thus pushing more of our portfolio into long-term investments (a.k.a. stocks, illiquid investments).

If a couple needs $10,000 per month to fund their retirement, their portfolio will be drastically different depending on whether they account for ~$3800 of that income coming from Social Security.

This Google Sheet shows what I mean. I looked at a $1.8M portfolio. The couple who wisely includes Social Security income in their math can reasonably build a 60/40 portfolio for their retirement. On the other hand, the couple who neglect Social Security income would end up building a 40/60 portfolio. That’s a big difference!

Again, Social Security for a newly retired couple can be considered a $700K—$800K allocation to fixed income. When you include that into the 60/40 portfolio described above, it looks similar to a 40/60 allocation.

Granted, we need to remember a couple important caveats:

- While considering Social Security as a lump sum is helpful from a portfolio construction standpoint, we still cannot withdraw Social Security as a true lump sum (like we could an IRA or taxable account).

- The “value” of Social Security steadily decreases with age as our expected remaining lifespan decreases.

Conclusion

Going back to those opening statements:

- “We don’t want to assume Social Security will be there for us. Let’s just focus on the assets in our control.”

- “I know Social Security is there, but it’s so small. Let’s play it safe and ignore it for now.”

- “Social Security is only $2000 monthly, whereas my IRA has $900K. Social Security is a drop in the bucket.”

For the average new retiree, this is a $350K—$400K oversight per person, and twice that for a couple.

These aren’t drops in the bucket.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

This is fantastic information! Thank you for explaining it in a way that is digestible and not anxiety inducing.

Thank you! I’m glad you found it helpful.

Jesse

Generally a good article. But I take exception to two points:

1) “Does Delaying Matter? […]

In short, there’s no effect.”

This is incorrect. In fact, it is actuarily beneficial to delay SS to 70. Reason being that the SS early and delayed retirement credit percentage adjustments haven’t been updated since 1983, but life expectancies have increased considerably since then. So, they currently favor delaying.

2) Basing SS lump sum equivalent only on life expectancy is a mistake for a few reasons, not the least of which is that odds are 50% you’ll outlive your life expectancy, and even more likely that at least one person in a couple will. If you don’t feel safe using a 6% withdrawal rate on your own nest egg, you shouldn’t use 6% to convert SS monthly payments to a lump sum equivalent. Same with using a 20 year bond rate. The closer equivalent financial instrument to compare against would be purchasing a 100% joint and survivor annuity (at least for the higher earner in a couple) with a 2%-3% annual COLA (SS is better since it is CPI adjusted, but you can’t buy a CPI adjusted annuity), and seeing how much you would have to spend on that. SS is a bit better than the annuity because there are no sales commissions, but in terms of risk, this is much closer to equivalence than a bond that would drop to $0 after 20 years.

Hi John, thanks much for the feedback.

On your Point #1 – amazing! Thanks for pointing that out. I went off and did a few hours of reading and, yessir, I agree with you. I’ve edited the article to reflect that.

On your Point #2, I mostly disagree. I’m intentionally painting a picture for the *average* scenario. For example, we both know that $1900 per month is the *average* SS income, but that very few retirees *actually* received $1900 per month on the nose. That fact, however, doesn’t mean that using $1900 per month is the wrong thing to do here.

Now, using US Treasury bonds *while including your own adjustments for inflation in the initial sum* feels like a smarter choice, in my opinion, than buying a high-fee annuity. Maybe that’s just a disagreement on the details. If you’d like to run the math of the correct way to value the correct sized annuity to “replace” a couple’s social security cashflow, I’d be interested to see what you come up with.

Either way, good food for thought and thx for the feedback.

Thanks for updating the article on point 1. And I agree the effect is not huge, but the benefit for the high earner in a couple (or a single individual) to delay is longevity insurance (reduces the risk of running out of money before running out of life) since no one knows how long they’ll live, most people underestimate their life expectancy (especially for a couple), and with a 50% chance of outliving life expectancy, I think it is quite dangerous to plan only up to life expectancy.

On point 2, I agree that individualized inflation estimate is appropriate if you have it, but 2%-3% is a pretty good placeholder, as 2% is the Fed target inflation rate, both the 20 and 30 year average inflation rates are under 2.5%, and 3% leaves some margin in case inflation is high early in retirement (sequence of inflation risk). High cost annuities should be avoided, but commission-free SPIAs exist which should be reasonably priced if riders aren’t added. But my main point that lifetime annuities are more comparable than fixed term bonds for comparison to Social Security is that bonds do not provide longevity insurance, whereas Social Security does, so they are not a fair comparison. If given the opportunity to replace my Social Security with 20 or even 30 year bonds, there is no way I would do that, because of the risk of running out of income late in life.

I don’t know how to mathematically calculate annuity premium costs. They fluctuate and that has to be looked up on an annuity cost comparison websites.

FYI, I previously tried to comment on my own comment and kept getting nonce errors, failing to post. Probably a WordPress thing…

Great article, thanks for a “different” way to look at SS!

You’re welcome! I’ll glad it resonated with you.

_Jesse

One of the other benefits of social security – is it does a reasonable job of keeping pace with inflation. Our brains have a hard time imagining the impact of inflation in 25 years….love that you modelled that on your spreadsheet.

Thanks for the feedback and thanks for reading!

I was watching a program on financial tips and on there he said that you have to pay taxes on social security now. Is this true?

Hello – the short answer is, “It depends on your overall income.”

The longer answer is:

Yes, for some people, up to 85% of their Social Security income is taxable based on the Federal income tax brackets. Be careful, though. “85% taxable” is much different than “taxed at an 85% rate.” Instead, it means that 15% of SS income is tax-free, while the other 85% gets taxed at one of the Federal income tax levels (10%, 12%, 22%, etc).

If your overall retirement income is high, you’ll likely be paying taxes on 85% of your SS.

If your overall retirement income is low, you might pay taxes on ZERO of your SS income.

This is where smart retirement planning and tax planning comes into play.

Best,

Jesse

Wow, that 85% taxable thing totally threw me for a loop when reading irs documents. Thanks for explaining this in a way that I actually understand.

No problem, David!

Thank you for sharing. This has been on my mind for some time and sheds the light I needed. Does this logic hold true for other income streams, such a pension?

Hi George – yes, this logic holds true for other income streams.

You’ll want to ask yourself questions like,

“How guaranteed is my other income stream?”

“Is it adjusted for inflation?”

“How well-funded is the pension fund?”

“What’s the pension fund invested in?”

etc. etc.

Good luck!

Jesse

Such a motivating article! It always perplexes me why people discount having social security in their retirement projections, especially because for the vast majority of people, they will have to rely on it for most of their living expenses. Suddenly having an “extra” $350k-$450k for retirement is a game changer.

Thanks for this article. I am public school educator in CA. I don’t pay into social security given teacher pension rules here. But I have 20 credits from previous employment. Should I find a way to get all 40 credits to get social security at some point—even though there will be also be the government offset penalty and windfall elimination penalty? Is it still worth it?

As of now, I’ve just overlooked social security but your article here is making me re-think it. However, the added obstacles of the GPO and WEP penalties stops me in my tracks again.

Thanks for any and all insights about this matter.

Hello there. I’m not familiar with all of the in’s and out’s of the California system.

As for your SS question, are you essentially asking, “Should I work 5 additional years while paying into SS, obtaining 4 credits per year?”

To answer that, I’d start with, “Well…we need to understand the entirety of your retirement puzzle in order to provide a proper answer. ALL the puzzle pieces are important.”

So for that reason, I’d recommend you reach out to a Certified Financial Planning professional who specializes in that kind of retirement analysis.

Feel free to send me an email [email protected] to continue the conversation.

jesse

Thank you for explaining a mystery for me. My wife and I have found that social security income is sufficient for 90% of our living expenses. Why then use a conservative formula like 60/40 (stocks/bonds) for our retirement portfolio? Even a 20% to 30% loss or more in our stock portfolio would have little effect on our daily lives, neither now nor in years to come. So we’ve increased our stock holdings to 80/20 currently, and plan to keep the stock portion somewhere between 60 and 80 going forward.

I suppose we might plan more conservatively considering increasing future health care needs, but those costs seem designed to consume any fortune, no matter the size!

Risk on!

You’re welcome, Gerry. Glad you found it helpful!

Hi Jesse, great article and very helpful.

One major thing I noted in the spreadsheet and the chart you’ve included – it seems you forgot to multiply the monthly SS payments with 12 for annual calculations?? The numbers will shake out much higher for lifetime SS income. Unless you did actually mean for everything to be an annualized income estimate in today’s dollars?

Thanks and keep up the good work!