Don’t miss an episode of our podcast, Personal Finance for Long-Term Investors. Available on all podcast players.

Here’s the latest episode:

Today’s article addresses a fantastic retirement question. Reader-of-the-blog Maykel asked me:

So I often hear people say if you follow the 4% rule you’ll “never run out of money.” But I thought it was just a high probability of not running out of money for maybe 25-35 years? Can you really never run out of money with the 4% rule?

Maykel’s question is so good because the 4% rule is the most frequently misunderstood retirement topic I see in personal finance forums and social media.

So let’s break it down and explain the 4% rule in simple terms.

PS: Here’s a straightforward financial independence and 4% rule calculator where you can input your own data.

Why the 4% Rule Was Created

Retirees have always faced a scary question: how much money can I withdraw from my portfolio without ever running out?!

This amount of money is called a safe withdrawal rate (SWR).

Without a known SWR, how can someone determine how much money they need in retirement? How can a person feel comfortable that they won’t run out of money? It’s a stressful question.

The Basics of the Rule

The “4% rule” suggests that retirees can withdraw 4% of their retirement nest egg every year in retirement and never run out of money. **With some important caveats! We’ll discuss them.

Let’s say I’m planning my retirement. After calculating my Social Security benefits, my small pension, and the thousands (of pennies) generated by The Best Interest, I realize that I need an additional $2500 per month to cover my cost of living.

That $2500 per month—or $30000 per year—will come from my retirement savings. But how big does my portfolio need to be to fund $30K per year? Let’s use the 4% rule!

I should save 25x (100% divided by 4%) my $30000 need by saving $750,000. That way, I can withdraw 4% of $750,000—which is $30,000—to help fund my first year of retirement.

That’s the 4% rule. But let’s discuss some of its vital caveats.

The 4% Rule Assumes a 30-Year Retirement

The 4% rule has been “backtested” many times. It was proven to work over a wide range of historical financial scenarios, using real historical stock and bond data.

The 4% rule had a 100% success rate for 30-year retirements, a 91% success rate for 35-year retirements, and an 89% rate for 40-year retirements. Withdrawing 4% for 30 years is safe.

**Note: I’m using Wade Pfau’s 2018 update to the Trinity Study

“But Jesse, 4% times 30 years is 120%! How can I withdraw more than 100% of my portfolio?!”

Great question. It’s because your portfolio is invested. You own stock and bonds, and they’re growing, like a tree. You’ll prune away branches (spend your money), but new shoots will replace them (investment growth).

30 years is safe. But 35 or 40 years are less safe. The new growth doesn’t always keep up with the pruning.

If you’re using the 4% rule to plan your 50-year “FIRE” retirement, you’re using the 4% rule wrong. You’d need to use results from a 50-year backtest (e.g. a “3% Rule”).

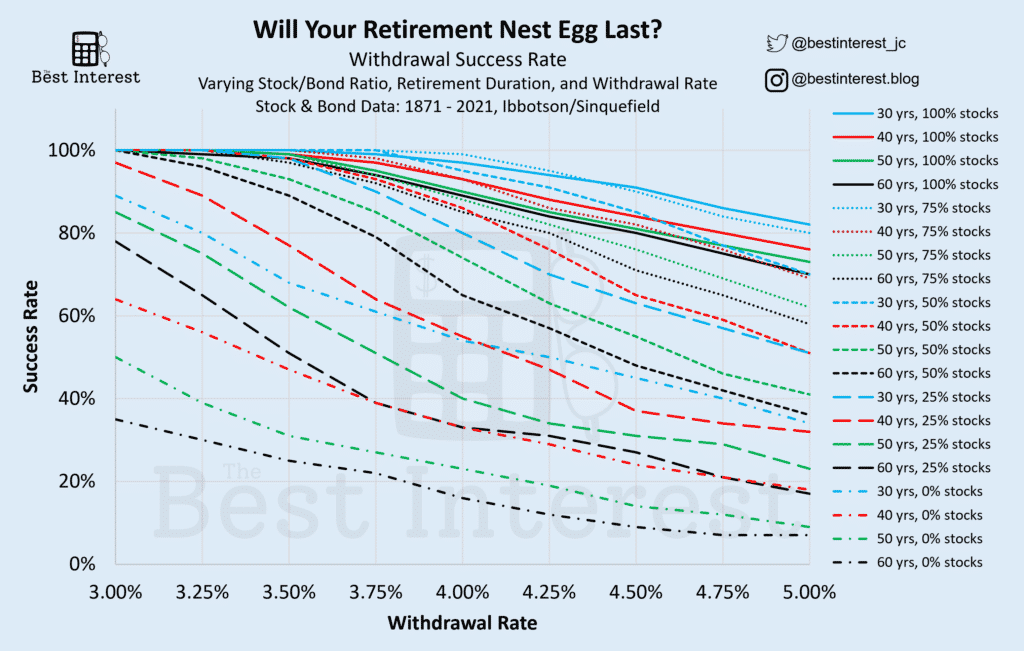

The 4% Rule Assumes a “50/50” Portfolio

The 4% rule was based on the assumption that a retiree has a balanced portfolio of stock and bonds. Wade Pfau’s most recent “backtest” utilized the S&P 500 for stocks and intermediate-term Treasury notes for bonds.

If you’re using the 4% rule on a 100% stock portfolio or 100% bond portfolio, you’re using it wrong.

Each portfolio (all stocks? all bonds? mix?) and each duration (30 years? 20 years? 40 years?) has a safe withdrawal rate that you can use as a benchmark. But it might not be 4%!

Here’s a useful graph that shows other portfolios’ long-term success rates.

The 4% Rule Is Inflation Adjusted

The 4% rule’s creators were smart, and they included inflation into their “backtest.” Let’s revisit my example above, where I’d save $750K to withdraw $30K in Year 1 of retirement.

Due to inflation, I might need $31000 in Year 2. And then $32000 in Year 3. Etc. The creators of the 4% rule accounted for this slow creep upwards. It’s already built-in.

The 4% calculation (and the “25x Rule” I used above) is based on your Year 1 spending in retirement, and accounts for inflationary cost of living increases.

What the 4% Rule Is Not.

Let’s now focus on what the 4% rule is not.

By understanding these common 4% rule mistakes, you can arm yourself against poor retirement planning choices.

The 4% Rule Is Not a Guarantee

The 4% rule isn’t guaranteed to work for you.

It worked in the past. It worked based on 20th-century economic conditions. Will the next 100 years mirror the previous 100 years? I don’t know. Maybe we’ll have a utopia. Or maybe the climate crisis (or aliens, or a meteor, or…) will destroy us.

That’s the hard part about being human. We too easily fool ourselves into exuberant optimism or forlorn depression.

If we Cathie Wood ourselves into 20% annual returns for the next 50 years, we should adopt a 10% Rule and retire tomorrow.

If we Jeremy Grantham ourselves into believing the Greater Depression starts tomorrow, even a 1% Rule will fail. The economic cataclysm will turn Hometown USA into Mad Max.

I try to stay between those extremes. That’s why I use the 4% rule as a starting point. It’s a guidepost. It’s as good an answer as we have. But it’s not a guarantee.

But get this: the OG of the 4% rule, Bill Bengen, recently told the Wall Street Journal he mainly holds cash—not stocks or bonds!—due to his anxiety over current high market valuations. Looking at the market right now, maybe he was onto something…

In late 2021, Morningstar issued a report suggesting that a more conservative 3.3% to 3.5% Rule was the intelligent choice moving forward. That means retirees would need to save more.

But then financial planning all-star Michael Kitces published a response to Morningstar explaining why the 4% rule is still valid.

Why am I telling you about Bengen, Morningstar, and Kitces? Because even the best experts in the world can’t agree on the 4% rule’s utility!

It’s a guidepost. Not a guarantee.

The 4% Rule Isn’t Aggressive or Conservative

“You probably shouldn’t eat too much candy.” Is that an aggressive admonishment? Or a conservative suggestion?

If you’re a 9-year-old on Halloween, it’s aggressive. Don’t limit me! I want to eat all the candy!

But if you’re a paranoid dentist, it’s conservative. Why leave the door open to any candy consumption? Don’t you realize one mini Snickers can cause a cavity?!

The 4% rule is the same.

If you run out of money in retirement, you’d accuse the 4% rule of being irresponsibly aggressive. But remember: the 4% rule was created to eliminate failure. Therefore, it can be very conservative for many retirees. Here’s a crazy example of that conservatism:

The aforementioned Michael Kitces did a backtest of the 4% rule on a 60% stock, 40% bond portfolio. Kitces found that retirees using the 4% rule here were more likely to 4x their money than they were to decrease their portfolio by a single cent!

Why? Because an investment portfolio often compounds well beyond 4% per year. The 4% rule survives the worst markets and thrives in average ones.

The 4% Rule Doesn’t Absolve You of Taxes

You need to consider your own tax situation when applying the 4% rule to your life. Far too many people misapply the 4% rule by not considering their taxes. For example:

“Rent, groceries, gas, etc….I spend $4000 per month, or $48,000 per year. If I multiply by 25…that’s $1.2M. Therefore, I need $1.2M in my 401(k) to safely utilize the 4% rule!”

The problem, of course, is how that $1.2M could be taxed. Dollars invested in “traditional” retirement accounts will face a future income tax. Dollars invested in a taxable brokerage might face future capital gains tax.

The $1.2M nest egg could easily be $1.0M after tax. And now you’re withdrawing 4.8%, not 4%. That’s not ideal.

You need to account for your taxes such that your total annual withdrawal (including the tax bill) is 4% of your Year 1 nest egg. Easier said than done. A spreadsheet or financial planner is your friend, here.

PS: Dave Ramsey Can Be Very Wrong

One final note today. Dave Ramsey is great at getting people from negative net worth (i.e. in debt) to zero. But he’s demonstrably bad at getting people from zero net worth to retirement.

Case in point: Dave recommends people use an 8% withdrawal rate (“the 8% Rule”) on a 100% stock portfolio. Let’s test that out! We have Wade Pfau’s recent Trinity Study to show us:

- For a 20-year retirement, Dave’s plan fails in 38% of backtests.

- For 25-year retirements, 46% failure.

- 30 years, 57% failure

- 35 years, 64% failure.

Dave’s plan fails a lot. While 100% stocks can work for long periods of wealth accumulation, it’s far too aggressive for long periods of withdrawals.

Time to Retire…

Big thanks to Maykel, whose great question prompted today’s article.

The 4% rule is not a guarantee. And it has important caveats that are too often overlooked. But it remains a data-backed guidepost to help retirees find comfort in their long-term financial planning.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

Does it matter if you pull out in lump sum yearly amounts or divide that into 12 monthly withdrawals?

Hey Sara! Technically speaking, you’re more likely to succeed with more “time in the market.”

That is, pulling 1 year of money out on January 1st is worse than withdrawing money 1 month at a time.

The Trinity Study assumed 1 withdrawal per year.

I like how you explain the 4% rule as a guide post. In my opinion the 4% rule is conservative the risk of failure is very low. As you pointed out normally the majority will end up in having much more money than when they started by a large margin. The only time one would call the 4% rule aggressive is if one starts retirement off with a bad sequence of returns drawing down their capital early on in retirement. However, If one is flexible and adaptable they could make changes (go back to work/cut expenses) to deal with this risk.

Thanks Tech!

It definitely skews conservative. 100% agree. The problem tho, is that upon failure, it becomes the most AGGRESSIVE withdrawal plan in the world! 🙂

And as you said; flexibility fixes this problem.

Thanks for this write-up Jesse, very helpful. I’m curious: Is there any combination of ETFs that one could buy in the 50/50 distribution to match exactly the backtested portfolio? I guess for the stock portion it would be something like $VOO…?

Thank you 🙂

And don’t worry, I won’t buy exactly that. But it will be helpful as a start. Especially on bonds, I’m pretty clueless…

Hey LadyFire!

Yeah, I think so.

VOO would replicate the stock portion.

And if you want to stick with Vanguard, VGIT would be the best proxy for the bond portion.

Hope that helps!

Great article! I for one am using the 3.25% rule, but since my retirement was haphazard, I also bought a website to help cover my butt a bit and bring in some cash flow in the event of a prolonged bear market. 3.25% still feels risky to me, because there is so much more risk given current market conditions (see inflation). Alas, only time will tell!

Thanks a bunch, AR!

I was thinking on the drive in this morning…the “number” is important. But I believe the willingness to be flexible is infinitely more important.

3%, 4%, 5%…whatever. Are you willing to tone it down during bear markets to avoid the sequence of returns risk? I think THAT is the most important part of SWR retirement planning.

Need re-balance portfolio every year?

Depends on the person. The most common frequencies I’ve seen and used are twice per year or once per year.