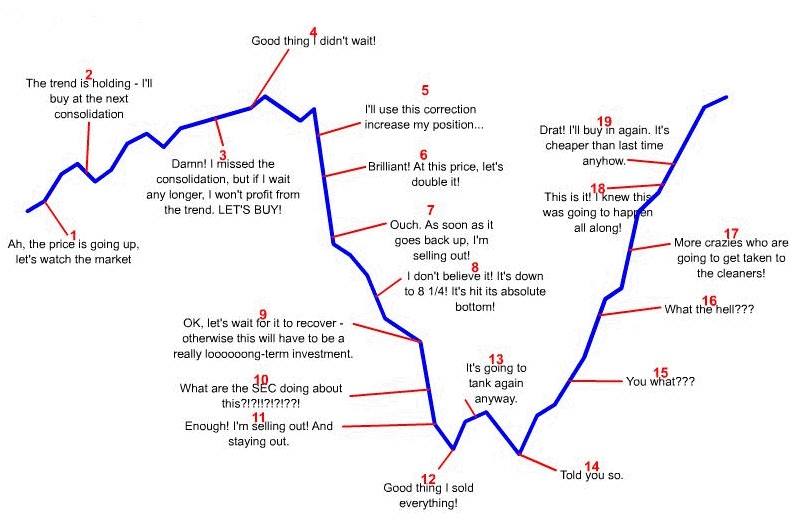

Like birds chirping at the rising sun, investors tweet “buy the dip!” at the first hint of the stock market dropping. Yes, “buy the dip!” makes sense at first blush. It suggests that we should buy assets at the lowest possible prices.

But “buying the dip” is a suboptimal investing strategy.

Let’s discuss why.

The Basic “Buy The Dip” Argument

Buying stocks is a risk. The stocks’ prices might go down after you buy them.

But holding onto cash is a risk, too. That cash could be invested—and grow with the rising market! This is the opportunity cost of not investing.

Either choice—to invest or not—has a risk and a reward. The risk is that the market moves in the wrong direction. The reward is that the market moves in your favor.

So how do we answer whether ‘buying the dip’—i.e. waiting for the market to drop in price before we buy—works?

We can’t predict what the market will do in the future. But we can look at previous market data to “backtest” a buying-the-dip strategy. This is what professionals typically do. And we’ll do that today.

Two Kinds of “Buy The Dip”

Before I insult too many people, let’s baseline ourselves. There are two common definitions of ‘buy the dip.’ As my good friend Andy wrote:

Scenario 1: You’re holding lots of cash for many years, waiting for a big crash. And then you buy after that crash. This is certainly a form of “timing the market.” But is it the same as “buying the dip?”

Scenario 2: You’re holding a small amount of cash, expecting to deploy it in the market in the next few weeks. You wait for a single “red day” of stock market decreases before buying. Even if the market only drops ~1%, you “buy that dip.” Rinse and repeat on a weekly or monthly basis.

I consider both these scenarios to be a form of bad market timing. I say both are “buying the dip.”

But Andy and many others disagree. One argument they make is this: since they are dollar-cost averaging (DCA) anyway, why not wait for a red day to execute their purchase? Buy low, they say. It makes sense.

And in Andy’s defense, I do see a significant difference between the two scenarios. And it’s not just my opinion. The difference between the two scenarios is backed up by convincing analytical data.

Holding onto cash for years is a huge losing scenario. It could cost you millions of dollars (seriously) over the course of a 30-year investing timeline. It underperforms basic dollar-cost averaging by as much as 800% in historical backtests.

Holding onto cash for a few weeks is a slightly losing scenario. Over most historical 30-year investing periods, attempting to buy every dip would drag your overall portfolio down by 0.5% – 1.0%. For someone retiring with $1 million, holding onto cash to ‘buy the dip’ would have cost them ~$10,000 over 30 years. It’s not terrible. But it’s certainly not good!

Note: your emergency fund should still be in a cash bank account. Today’s article is specifically talking about money that you plan on investing. And in my opinion, your emergency fund should not be something you invest.

Waiting for 2% dips drags down historical portfolios by 1-2% over 30 years. Waiting for 5% dips drags historical portfolios by 2-10% over 30 years. No matter how much of a dip you wait for, it’ll impact your portfolio negatively over the long run.

The bigger a dip you’re waiting for, the more it costs you. The best thing to do is not buy the dip at all.

Here’s the full data set and analysis method for all the summaries above.

Enjoying this article? Subscribe below to get new articles emailed straight to your inbox

But Why? Buying the Dip Makes Sense…Right?!

Most people equate buy the dip to buy at a low price. And as we all know, it makes sense to buy assets at low prices. So why doesn’t “buying the dip” work in practice?

The best way to explain it is with a simple example.

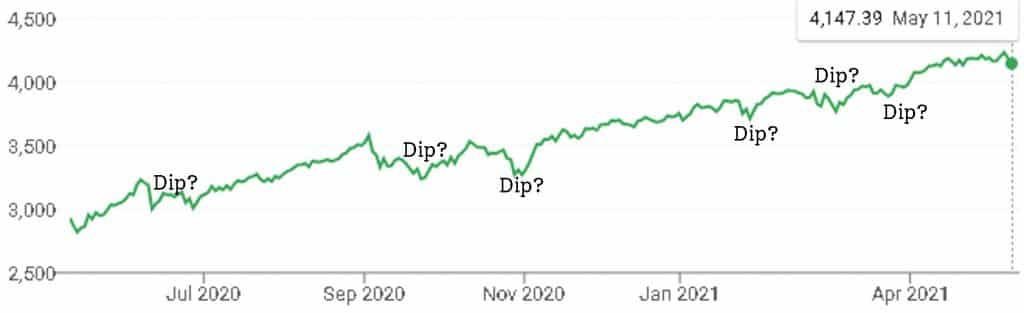

Let’s say Adam had money to invest in April 2021. On April 1st, the S&P 500 was valued at $4020. Adam decided to wait before buying—he wanted the market to drop so he could buy the dip.

Unfortunately for Adam, the S&P increased by 4.1% in the first two weeks of April, from $4020 to $4185. Only then did the S&P dip—by about 1.2%, down to $4135.

Should Adam have bought that dip at $4135, even though $4135 was higher than where he was previously sitting ($4020) at the beginning of April?

Should he have held out for an even bigger dip? What if that even bigger dip never comes? The market is unpredictable. I bet Adam felt conflicted, possibly full of regret.

I specifically cherry-picked April 2021 because:

- It was a recent month.

- It was a typical month. We’ve seen similar months throughout stock market history. It’s a perfect example.

For most months, the best day to buy is the 1st of the month. For most years, the best day to buy is January 1st. Early is better most of the time. On average, waiting for a dip is a losing proposition.

A future dip might come. But it usually gets swamped out by larger gains in the meantime.

“Wait for lower prices” makes logical sense. But ask yourself—what if “lower” never comes? The problem isn’t buying the dip. It’s waiting for the dip.

What About Advanced ‘Buy The Dip’ Strategies?

I’m looking at one metric today: price. If you’re making investment decisions based solely on price, then “buying the dip” is a losing strategy.

But I’m sure there are ‘buy the dip’ strategies that utilize other metrics that might work. For example, imagine a strategy tied to the P/E or CAPE ratios.

Note: P/E stands for price-to-earnings ratios. When P/E high, it’s because stocks’ prices are high relative to those stocks’ underlying companies’ earnings. The ratio is generally used to determine whether the stock market is under-priced or over-priced.

If the market’s P/E ratio is too high, perhaps you’d be wise to hold off on investing until it dips by a certain amount. I could see that working. Or you could choose to invest based on Federal interest rates. Or you could use social sentiment metrics—what are people saying about given companies, or about the market in general?

My point is this: there probably are ‘buy the dip’ strategies out there that could work, even those that have worked in previous markets. There are millions of potential if/then correlations, and some of them will lead to investment returns that beat the market average.

But for 99% of the people reading this post—and certainly, the person writing it—we have neither the skill, the time, nor the moxie to make one of these strategies work.

If you’re asking me, don’t buy the dip. History frowns on you. Time in the market beats timing the market.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

Good reminder. The best advice is to setup investing automatically. Of course that is easier said than done. I have to manually move money from my saving account and I end up falling into the “market timing/buying the dip” trap. If markets are high let it sit in cash in my emergency fund, if there is a dip take the time and effort to move it over and invest it. Above you point out the fact that in the long run this “timing” also most always turns gives lower returns. Best to do it regularly and if it’s automatic even better.

opps a bad last sentence there. Should have read almost always gives you a lower return. * It could just be me but the comment line where you enter these comments is just showing one line at a time and seems to cut off the bottom letters making editing comments a challenge.

Hi Jesse, thanks for the article!

I came across this today because of the “dip” in crypto prices (which motivated me to finally buy a very small amount).

I understand your reasoning, and for the stock market, this seems to make rational sense. I’m curious: Do you think it also applies to something like crypto? With such volatility demonstrated multiple times by now, I have to say I certainly wasn’t comfortable buying at a peak.

Of course, no one knows the future, but I’m just curious about your thoughts.

Hey LadyFIRE.

Great question. Short answer, I can’t be 100% sure (though the pricing data is out there to crunch some numbers on)

But if we zoom out a bit…let’s assume we have an asset that will ALWAYS increase over time.

If you had to, would you prefer to invest in that asset SOONER or LATER? The answer should be obvious. It’s *sooner*

Of course, things get much more complicated when we consider things like supply and demand, investor sentiment, etc. But in short, we want to invest in profitable assets sooner rather than later.

Hope that helps!

-Jesse

Thanks Jesse! This article still makes me think…

I think what you say is generally true if certain conditions are met. One would be, as you mentioned, that it’s an asset that generally appreciates over time. I think another one might be that it is an “interest paying” asset. Because if stocks didn’t pay dividends, it could actually be (more) worth it to wait for a (serious) dip. I understand that if an asset first grows 50% and then falls 30%, you would still have been (slightly) better off buying earlier. So maybe there need to be some more rules around it.

If I had invested in bitcoin 10 years ago, would I be better off than having bought today? Sure. But if I had invested in bitcoin 1 month ago, would I be better off than having bought today? Nope. But if I had bought one month ago, woudl I in 10 years be better off compared to not having bought at all? Only time will tell. If it turns out that bitcoin is a continually appreciating asset, probably. But who knows for sure?

Maybe a mixed strategy could work… Say, if I was able to invest 1000 EUR a month, I could invest 900 and hold back 100 “waiting for the dip”. By dip I mean a significant dip, maybe 20+%? That way, when a serious correction happens, I would have some extra capital to take advantage, and “most” but perhaps not all of that capital would still benefit from buying lower than it otherwise would have. And yet, on the 90% of my investment, I’m still making sure I buy in early. I wonder if such a strategy would come closer to outperforming… Maybe I’ll run the math at some point 🙂 What source do you use for pricing data?

Either way, thanks for the thought-provoking article.

Hey again! Yes, you’re completely correct that intrinsically valuable assets–like stocks–make “buy the dip” less appealing. The asset is growing in-and-of-itself. It makes sense to get in as early as possible.

It probably be straightforward for me to write a “How Has ‘Buy the Dip’ Worked For Bitcoin’s 10 Year History?”

That’d be a cool article!

I’d certainly like to read such an article 🙂

It’s on its way 😉

I’ve also done my backtests to face buy and hold by setting aside a monthly amount for future dips (large and small). Always with funds that are statistically expected to grow over the long term.

And I quickly came to the conclusion: the strategy of buying the dip, with the SP500, works better than “buy and hold,” only if you know where the bottom of the decline is. Any other approach works worse than buy and hold. And that’s the difficulty.

Now, I have another approach. Bogle portfolios typically have a percentage of fixed income (with very few, even negative, returns over the last four years). If that money is invested as the dip occurs, the following occurs:

1) You don’t lose your risk profile, because the deeper the drop, the more you can rebalance and invest more in equities, while the fixed income in the portfolio maintains the same weight.

2) Knowing that the further the SP500 falls, the greater the probability of hitting the bottom, allows you to avoid taking excessive risks by buying more equities with fixed income. Of course, you can then reverse the dip when we recover.

3) By using the fixed income in the portfolio, you are not incurring any opportunity cost losses.