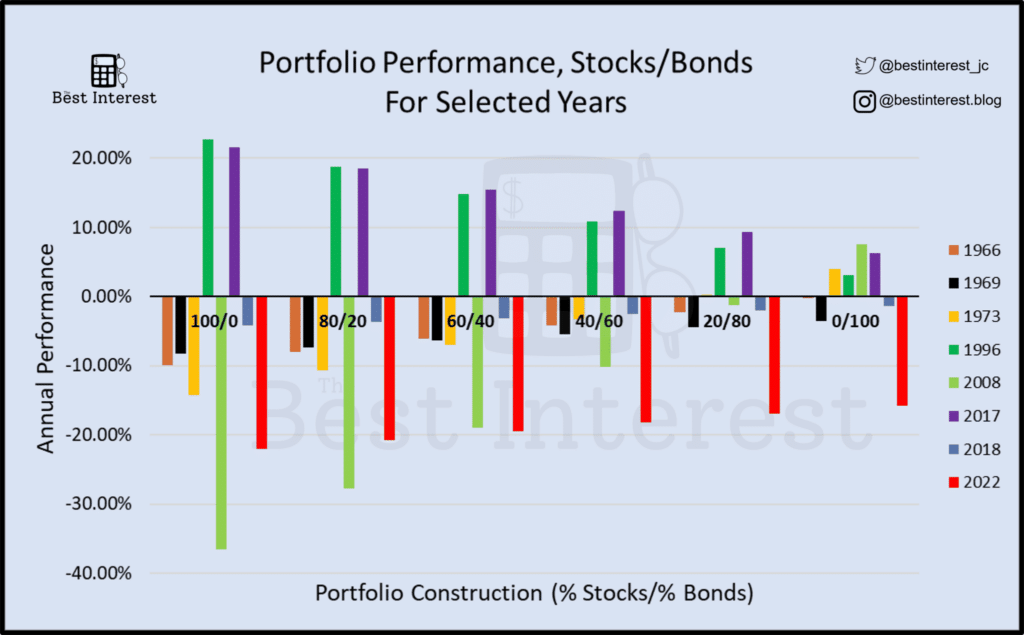

2022 was a bad year for investors. See the red lines in the graph below? …that’s 2022!

Back in October (around what turned out to be the bottom of the market) I wrote:

2022 is, by far, the worst year for stock/bond portfolios since 1950. We know that stocks can, and will, drop 20%+ in a year. But the fact that bonds are also down 15%+…that’s different.

Now, the real question: what should you do about it?

Should you stop investing? Stocks and bonds are both down…so jump ship altogether?!

No. Definitely not. Remember, “the true cost of long-term investing is psychological.” It hurts to see your portfolio value drop. I know. But success comes from enduring that pain and, if you can, leaning into it. Keep investing.

Should you sell your bonds?

No. It’s too late for that anyway. The leading indicator for future bond returns is the current interest rate. Having bond rates at ~4% right now is a strong signal that you’ll achieve ~4% returns on near-future bonds.

So…should I just sit here and take it?! That’s not advice!

Remember what John Bogle famously said:

My rule — and it’s good only about 99% of the time, so I have to be careful here — when these crises come along, the best rule you can possible follow is not ‘Don’t stand there, do something,’ but ‘Don’t do something, stand there!’John Bogle

Don’t do something? Stand there?!

It feels almost inhuman, right? We’re biologically wired for action. We want to do something!

You can consider something like tax-loss harvesting or rebalancing. But you should not consider abandoning your long-term investing plan.

That’s the difference between an emotional investor who reacts to their gut and a rational investor who follows logical rules. Your gut wants to end the pain…to do something. But logic suggests you do otherwise. Will you succumb to your gut? Or listen to the combined logic of many investors far wiser than me or you?

I’m listening to the wise guys.

2022 is a uniquely bad year. It’s understandable to feel glum about it. But you don’t need a uniquely special reaction. Stay the course. Just keep buying. Let the markets and your portfolio recover in the long run.

Just kidding! The truth is it’s a little too early to say I told you so. One bad year of investment performance (2022) shouldn’t ruin our moods, and a half year of great performance (2023) shouldn’t make us over-exuberant. We might not be out of the woods completely. I just don’t know. And neither does anyone else.

But if you allowed 2022 to sour your puss and you chose to abandon your investment plan…yikes! Your results aren’t looking too good.

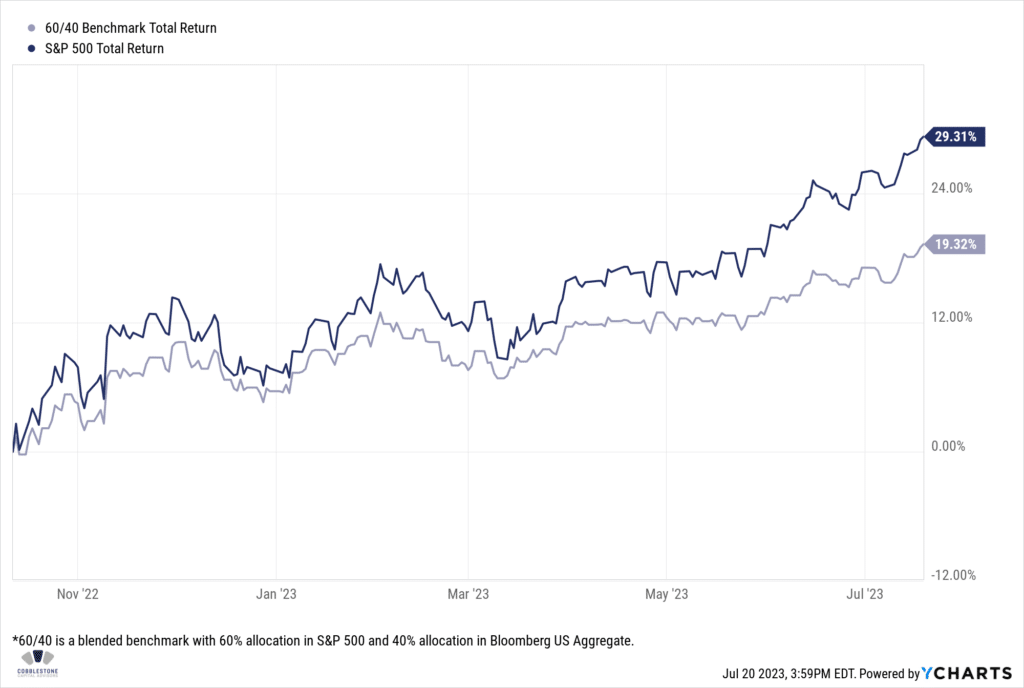

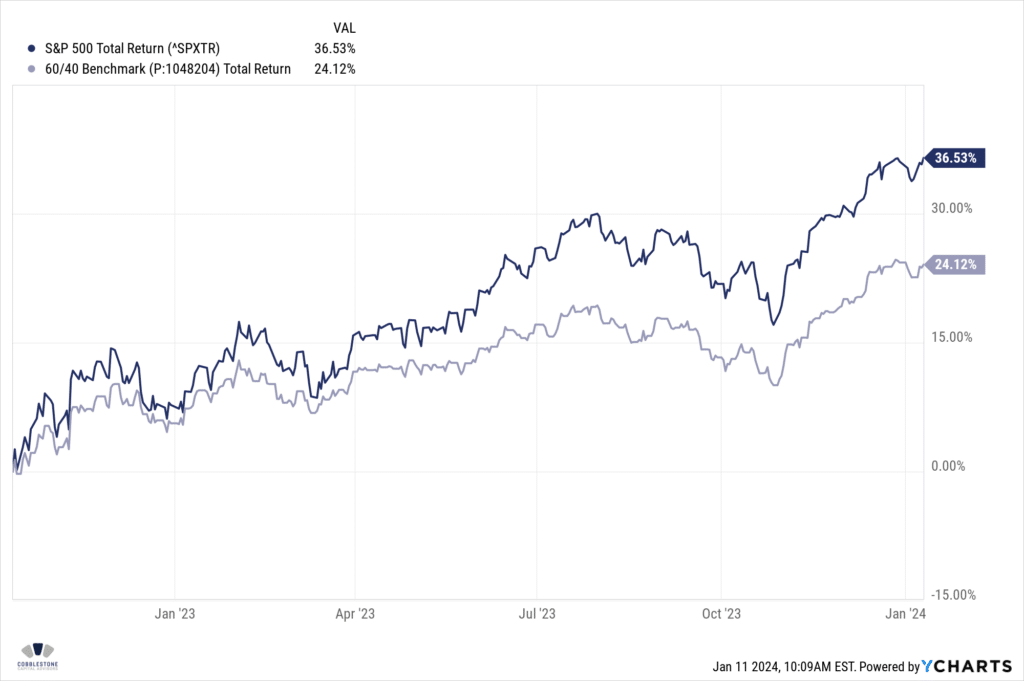

The chart below shows the S&P 500 (dark) and a 60/40 portfolio (light) from October 12, 2022 (the market bottom) to today (7/20/23).

The S&P is up 29% in 9 months. The conservatively diversified 60/40 is up 19% in that period. If you abandoned your portfolio at the end of 2022 and missed those gains…again, I say yikes.

Editor’s note: I’m back, writing this particular sentence on January 11, 2024. ~6 months after initially publishing this post, and ~15 months from the market bottom. Here’s an update of that chart as of today…

-Jesse

This is Example 1A of why you should stay the course. The headlines at the end of ’22 and the beginning of ’23 were awful. The stock market was taking a dump, the economy was surely headed for recession, and Barbara Walters died.

July 2022, Bloomberg: “Wall Street Says a Recession is Coming. Consumers Say It’s Already Here.”

September 2022, The World Bank: “Risk of Global Recession in 2023 Rises Amid Simultaneous Rate Hikes”

November 2022, CNBC: “Bezos urges consumers and business owners to reduce risk in the face of a likely recession.”

December 2022, NPR: “Barbara Walters, trailblazing journalist, has died at age 93.”

January 2023, Wall Street Journal: “Big Banks Prepare for a Recession”

Who would voluntarily invest in those headwinds?

I know who! Someone who understood market history, had a long-term mindset, and detached emotion from their financial decisions. Not easy, but very possible.

A bunch of The Best Interest readers did phenomenally well these past 9 months. Not because they’re stock-picking wizards, but instead because they buy a diversified set of income-producing assets month after month, then hold those assets for the long term.

Investing won’t always feel good. But the times that feel bad are often the best, most important times to stay the course. We’ll never know in the moment, and won’t find out until sufficient time passes. But with the benefit of hindsight, we usually realize, “How about that! The time that felt terrible was the market bottom, and we’ve only gone up from there.”

That’s the lesson so far in 2023.

That lesson might pivot tomorrow. I just don’t know.

But that’s the point. The exact point. I just don’t know. Neither do you, nor the experts writing the headlines.

And that’s why I’ll continue to stay the course.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.