Bear markets are nothing new.

Friend-of-the-blog Ben Carlson is having a field day in 2022 covering bear market history. Another f.o.t.b., Nick Maggiulli, wrote a great data-packed bear market article back in March. I wrote a quick “101” piece that picked up some traction.

Investing experts know a lot about bear markets. History is a great guide. We aren’t freaking out over the stock market being down 22% this year. It’s a known risk.

But 2022 is a little different. We’ve never seen a year—and a bear market—like this in both stocks and bonds. It’s a uniquely bad year.

Bonds are meant to be lower risk and lower reward compared to stocks. But most importantly, bonds are supposed to have little correlation to stocks. This is the mathematical underpinning to diversification and portfolio design. We don’t expect – and don’t want – stocks and bonds to behave in the same manner over the same time period.

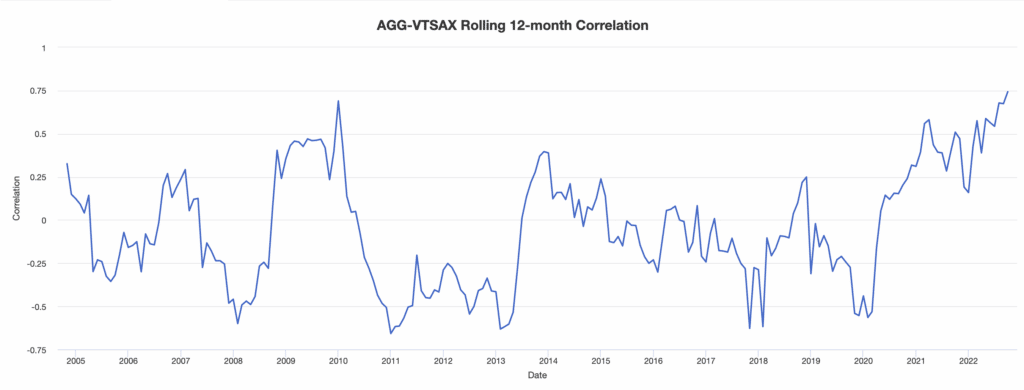

Above: the AGG represents a wide swath of the bond market. VTSAX represents a wide swath of the stock market. Normally, their correlation coefficient falls between -0.50 and +0.50. That’s a weak correlation at best. But we now see the rolling past 12 months’ correlation surpassing +0.75; generally considered strong to very strong correlation. This is not preferred for a diverse portfolio.

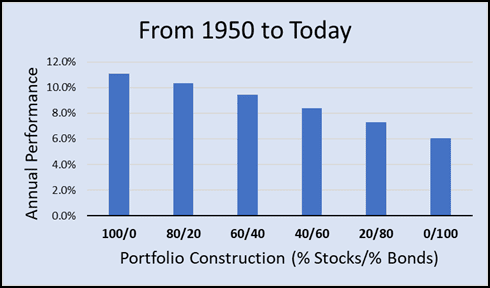

I went back and pulled stock and bond data from 1950. Let’s take a walk through history to see “normal” years, then compare against 2022.

But first: never forget that stocks are inherently riskier than bonds, and stock investors demand higher returns because of that. Simple risk and reward.

Stocks have returned 11% per year since 1950. Bonds only 6% per year.

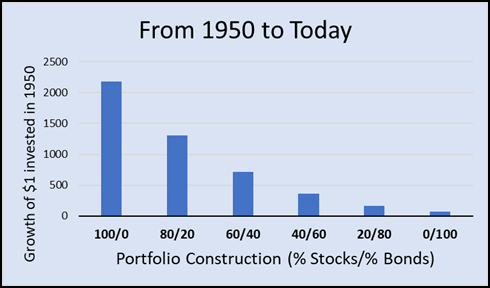

When we compound those returns over 72 years, though, we see an enormous difference. $1 in the S&P 500 in 1950 has grown over $2180 today. That same $1 in bonds has grown to $71.

Why, then, own any bonds?! Simple.

“We have to practice defensive investing, since many of the outcomes are likely to go against us. It’s more important to ensure survival under negative outcomes than it is to guarantee maximum returns under favorable ones.”

Howard Marks

We want to avoid fearful scenarios where we “sell to survive.” Stocks provide long-term returns. Bonds provide ballast. A balance of the two can provide you with enough returns to meet your long-term goals, and enough stability that you won’t puke along the way.

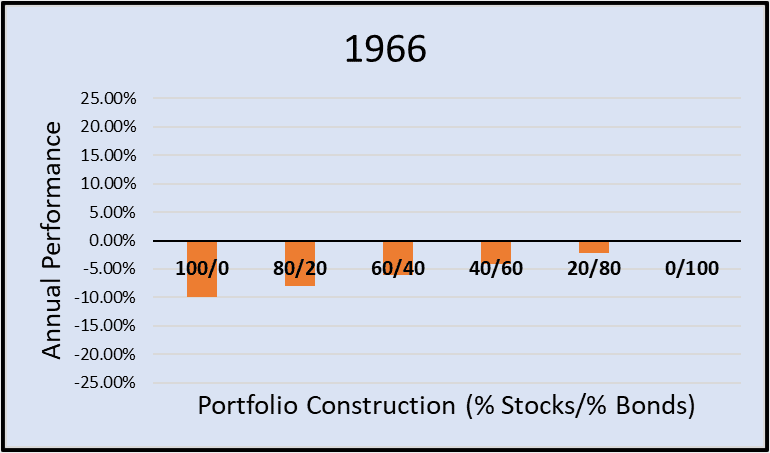

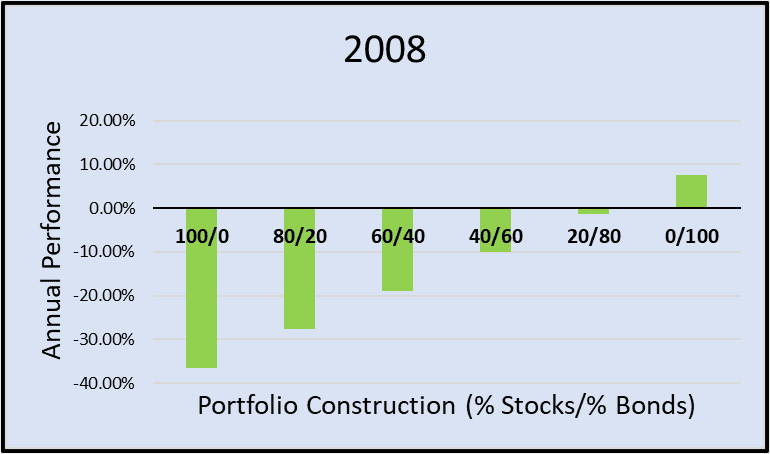

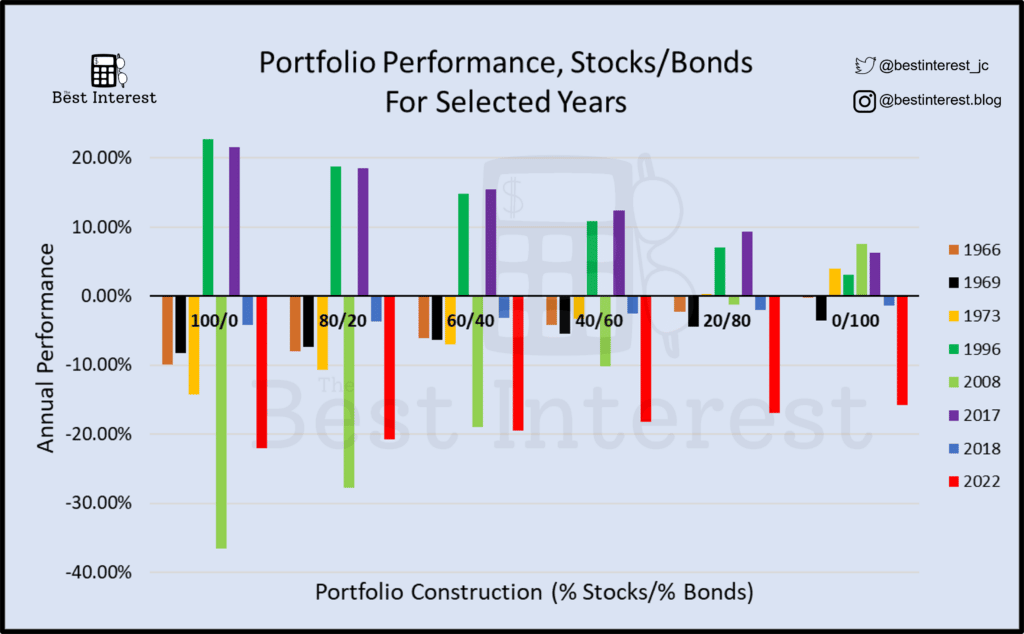

1966, for example, shows how a conservative portfolio (more bonds) prevents large drawdowns. This idea is even more pronounced in 2008 during the Great Financial Crisis.

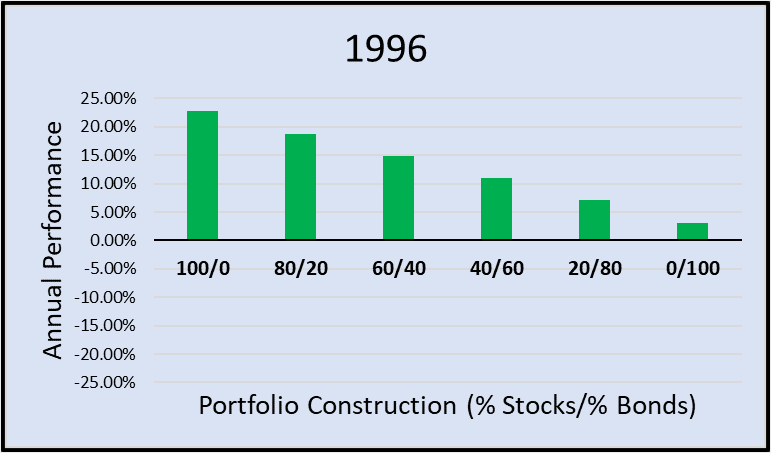

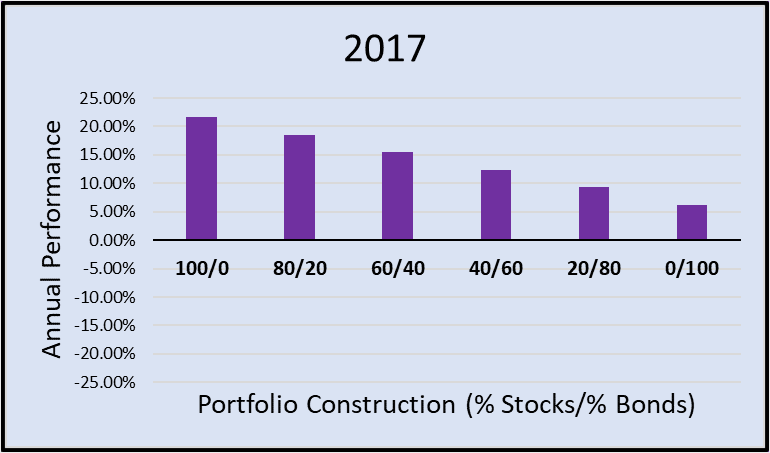

But most years, the stock market is up. Bonds tend to drag portfolio performance during those years.

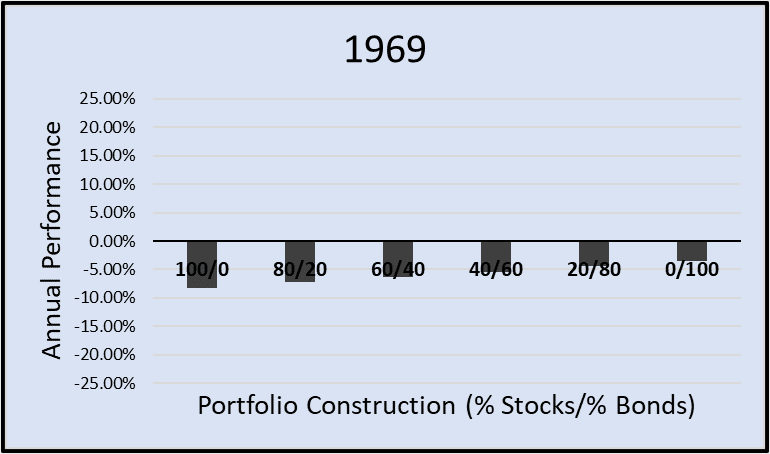

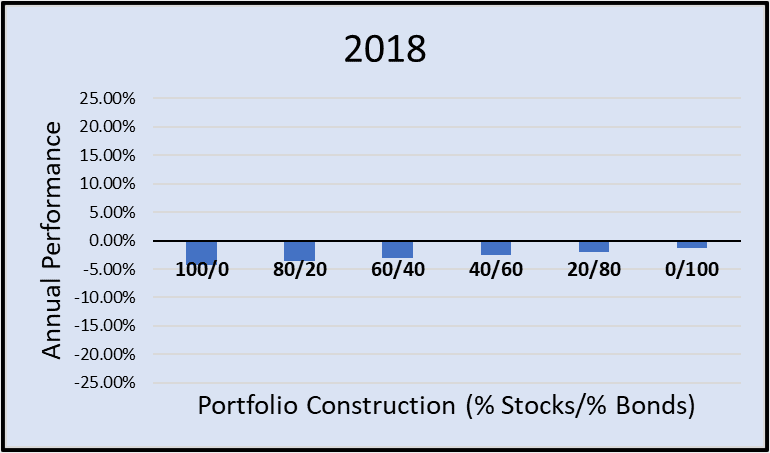

We have seen years with both stocks and bonds down, but it’s not too often, nor too severe. It happened in 1969 and 2018, but a balanced 60/40 portfolio was down ~5% in each of those years. It’s not that bad, like getting caught outside during a light rain.

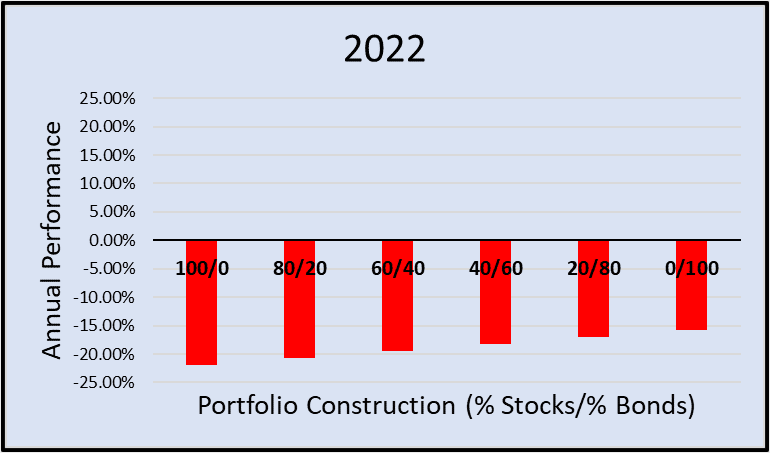

2022, however, is disturbingly different. Not only is there “no place to hide,” but it’s pouring rain. Even conservative investors are getting soaked. Across the risk spectrum, portfolios are down 15-25%. It’s unprecedented.

For reference and comparison, here are all of those years shown on one chart. Can you spot the outlier?!

2022 is, by far, the worst year for stock/bond portfolios since 1950. We know that stocks can, and will, drop 20%+ in a year. But the fact that bonds are also down 15%+…that’s different.

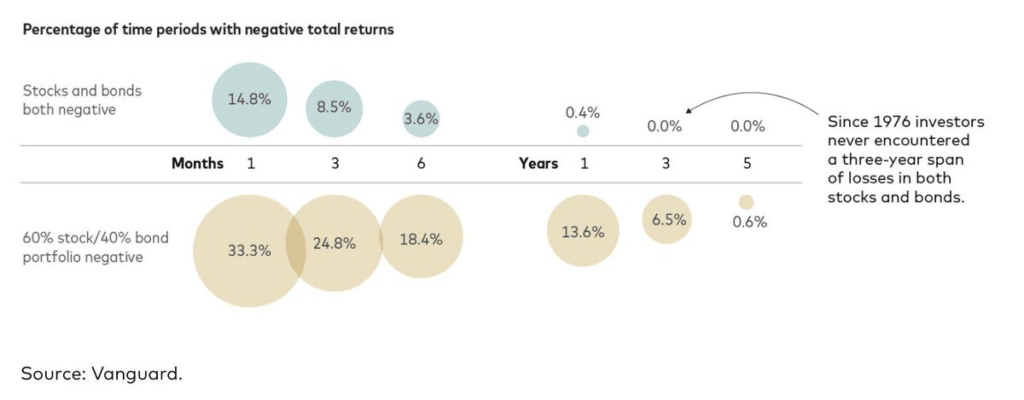

Friend-of-the-blog Sean sent me this great graphic from Vanguard:

In short, it shows:

- We’ve never seen a year like 2022

Now, the real question: what should you do about it?

Should you stop investing? Stocks and bonds are both down…so jump ship altogether?!

No. Definitely not. Remember, “the true cost of long-term investing is psychological.” It hurts to see your portfolio value drop. I know. But success comes from enduring that pain and, if you can, leaning into it. Keep investing.

Should you sell your bonds?

No. It’s too late for that anyway. The leading indicator for future bond returns is the current interest rate. Having bond rates at ~4% right now is a strong signal that you’ll achieve ~4% returns on near-future bonds.

So…should I just sit here and take it?! That’s not advice!

Remember what John Bogle famously said:

My rule — and it’s good only about 99% of the time, so I have to be careful here — when these crises come along, the best rule you can possible follow is not ‘Don’t stand there, do something,’ but ‘Don’t do something, stand there!’

John Bogle

Don’t do something? Stand there?!

It feels almost inhuman, right? We’re biologically wired for action. We want to do something!

You can consider something like tax-loss harvesting or rebalancing. But you should not consider abandoning your long-term investing plan.

That’s the difference between an emotional investor who reacts to their gut and a rational investor who follows logical rules. Your gut wants to end the pain…to do something. But logic suggests you do otherwise. Will you succumb to your gut? Or listen to the combined logic of many investors far wiser than me or you?

I’m listening to the wise guys.

2022 is a uniquely bad year. It’s understandable to feel glum about it. But you don’t need a uniquely special reaction. Stay the course. Just keep buying. Let the markets and your portfolio recover in the long run.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

Good article, wise advice. But you have to make sure the equities you hold are high quality. In USA, there were folks who held Enron, and in Canada, there were folks who held Nortel. Both looked like quality big companies & I knew folks whose brokers told them to average down, and buy more. Both companies went to zero, declared bankruptcy, and had management that were prosecuted for illegal actions. Once your losses reach a certain level, you need to act – retreat so your army of dollars can live to fight another day. I’ve seen too many “investments” get vapourized. Remain skeptical, take risks, but most of all, stay in the game.

Cheers Russel! You’re right. Those stories make me think of one word:

Diversification.

Great article! Thank you.

Joe Bob, thank you!

Thanks for the article and the data Jesse. The point I’d note is that if one took inflation into account 2022 would be a lot worse than it already looks, making it one of the worst calendar years on record. RK

Hi Ravi, thanks for the feedback. You’re right. I usually try to report investment data in real terms. But this article reports single years, I decided to report everything nominally. Not sure if that was right or wrong.

But your point stands. Thanks for reading and writing in!