Smart investors know to rebalance their portfolios. Let’s talk about why it’s so important and how you can do it yourself.

What is Rebalancing?

When you begin investing, you should have an asset allocation in mind. What’s an asset allocation? It’s the ratio that splits your money between the various asset classes and investments that you own.

For example, in How I Invest, I explained how my target asset allocation is:

- Large U.S. stock index fund—about 40% of my portfolio

- Mid and small U.S. stock index fund—about 20% of my portfolio

- Bond index fund—about 20%

- International stocks fund—about 20%

It’s a 40/20/20/20 asset allocation.

Over time, the markets will ebb and flow. Stocks might do better than bonds. Large companies might lag behind small companies. Etc, etc. You get the point.

One result of natural market movements is that my real-life portfolio asset allocation will wander from my target 40/20/20/20 ratio. For example: if U.S. stocks do well, my actual asset ratio might become 50/30/10/10.

I didn’t make any changes to what I own. But the market changed the value of my portfolio for me. And thus I’m faced with a question: should I adjust my portfolio back to the ‘target’ ratio?

This ‘adjustment’ is rebalancing. It’s bringing your actual asset ratios back in line with your target asset ratios.

Why is Rebalancing Good?

At first blush, rebalancing might seem bad. After all, let’s think about how a portfolio falls out of sync with your target ratio? It’s because some assets do great while others do poorly.

And what does rebalancing ask of you? It requires you to sell your best-performing assets to buy more of your under-performing assets. Why would anyone sell something good to buy something bad?

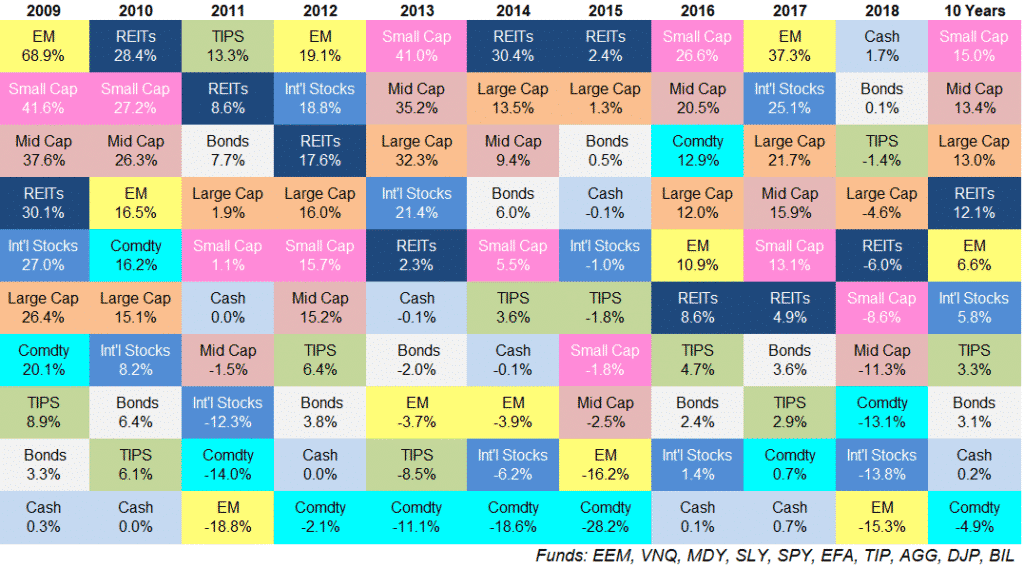

The answer is that “good” and “bad” are ever-changing in public markets. Take a look at the “quilt chart” below. It shows how various asset classes performed from 2009 to 2018. Time flows left to right, and each color represents a specific asset (e.g., pink = small-cap stocks, yellow = emerging markets)

One year’s winner can be next year’s loser. “Good” and “bad” are rarely stable over the long run. Asset performance is never guaranteed, and past outcomes do not equal future returns.

Rebalancing, therefore, isn’t about selling “good” to buy “bad.” It’s about selling “high” to buy “low.” And that—sell high, buy low—is one of the foundations of good investing.

But don’t worry. We’ll answer the question, “Does rebalancing actually improve portfolio performance?” later in the article.

How to Rebalance Your Portfolio?

From a logistics standpoint, rebalancing our portfolio is simple. Most brokerages offer automatic rebalancing, or you can choose to rebalance manually.

Some people rebalance based on how “out of balance” their portfolio is. For example, a rebalancing rule might read, “If any of my actual asset allocations are more than 5% different than my target allocations, then rebalance my portfolio.”

Others choose to rebalance at a specific frequency, e.g., once a quarter or yearly.

Note: This is what I do. I rebalance once every 6 months.

You’ll notice that both these rules utilize cold logic. The first is based purely on the numbers in your portfolio. The second is based on time. Neither is based on how you feel in the moment. That’s important. Like all good investing plans, the fewer emotions involved, the better.

But Is the Math Complex?

Any brokerage worth its salt will make the math of rebalancing incredibly easy.

You won’t have to calculate how much of this to sell or that to buy. Imagine trying to manually rebalance 10+ different assets! There’s a lot of math involved.

Instead of you doing that math, most brokerages will simply ask you: What target asset allocation do you want? Then, they take care of all the math, buying, and selling on your behalf.

If my target allocation is 40/20/20/20, but my actual allocation is 47/21/17/15, all I must do is ask my brokerage, “Please get me back to 40/20/20/20.” And they take care of the rest.

Enjoying this article? Subscribe below to get new articles emailed straight to your inbox

Does Rebalancing Earn Me More Money?

Here’s the money question! Does rebalancing improve your portfolio’s returns? Maybe.

The real point of rebalancing is to reduce your risk. It’s not about making more money, but rather about losing less money (in the case of a market crash, for example).

Nevertheless, we all want to know how rebalancing will affect the bottom line.

Financial advising guru Michael Kitces wrote an excellent article that divides rebalancing into two categories.

- Rebalancing between asset classes with similar returns (e.g., large-cap stocks and small-cap stocks, both around 10% per year)

- Rebalancing between asset classes with different returns (e.g., stocks and bonds, at 10% per year and 5% per year, respectively)

When the asset classes have similar returns, rebalancing can improve your returns while simultaneously decreasing your risk exposure. That’s a win-win! And investing expert William Bernstein agrees with Kitces in this article on his Efficient Frontier blog.

But when the asset classes have different returns, then rebalancing will always tamp down long-term returns. Let’s look at stocks and bonds as an example.

Over the long run, the law of averages says that your stocks will do better than your bonds. So, how will your asset allocation change as time goes on? It’s simple logic: your portfolio will skew towards stocks more than bonds. Therefore when you rebalance, you’ll sell stocks to buy bonds. And then? Then you have fewer stocks, a.k.a fewer of your best-performing assets.

So it’s true. Rebalancing between asset classes with different expected returns will likely hurt your long-term profits.

But the point of rebalancing isn’t profit-seeking. It’s risk-reducing.

What Happens if You Don’t Rebalance?

Forgetting to rebalance isn’t the end of the world. You could make much bigger mistakes—like neglecting to invest in the first place.

Rebalancing is a solid second-order behavior. As long as you’re investing your money and diversifying your initial investments (both first-order behaviors), you’re getting most of the way to success. Actions like rebalancing will take you from most of the way to all of the way.

In concrete terms, the risk of not rebalancing is that your portfolio could “un-diversify” itself, thus exposing you to a market crash.

Simple Rebalancing Example

For example, look at a simple 60/40 portfolio—60% stocks, 40% bonds. To simplfy the math, let’s say we own $60 worth of stocks and $40 worth of bonds.

Next, let’s say that stocks increase by 100% over 5 years (compounding at 14.8% per year for 5 years) while bonds stay stable over those 5 years—0% returns. We now have $120 of stocks and $40 of bonds.

Some quick math tells us that the asset ratio is now 75% stocks and 25% bonds. That’s significantly different than where we started. Thus, we are more exposed to stock risk and larger losses in a potential stock market crash.

What happens if stocks now crash by 40%?

Our $120 in stocks would become $72. We’d have $112 overall. Sure, that’s up 12% from where we started. But it’s down 30% from our high-water mark.

What If We Had Been Rebalancing?

Let’s play the same scenario again, except when we rebalance at the end of each year.

In Year 1, our stock portfolio grows from $60 to $68.92, and our bonds stay stable at $40. But now, we rebalance to achieve a 60/40 ratio. We sell some stocks to buy some bonds. Our new values are $65.35 in stocks and $43.57 in bonds.

The same pattern continues for the remainder of the five-year period. Stocks go up, bonds stay flat, then we sell a few stocks to buy bonds to rebalance our portfolio.

After five years, we have $91.99 in stocks and $61.32 in bonds, for a total of $153.31 total. Recall in the previous scenario, we had $120 in stocks and $40 in bonds for $160 total. We covered this: rebalancing can hurt you because you’re selling your “winners” to buy your “losers.”

But remember! What did we learn from the quilt chart above? Winners don’t stay winners forever! So let’s see what happens when the market crashes on our rebalanced portfolio.

We lose 40% of our stock value, and our $91.99 in stocks becomes $55.19. Overall, our portfolio drops from $153.31 to $116.52.

Ah ha! $116.52 is more than the other portfolio has ($112).

Rebalancing helped in this cherry-picked case. But it isn’t the end of the world if you forget. The rebalanced portfolio performed slightly better than the unbalanced portfolio.

But the important point is that the rebalanced portfolio remained diversified throughout this hypothetical.

Rebalancing Prior to Retirement

As you age and approach retirement, you should naturally rebalance your portfolio towards a less risky asset allocation. Traditionally, this means selling stocks and high-yield bonds in favor of lower-yield, stable bonds.

Financial advisors and experts frequently call this a glide path. Much like a plane gliding in for a smooth landing, aging workers should smoothly rebalance their portfolios as they retire.

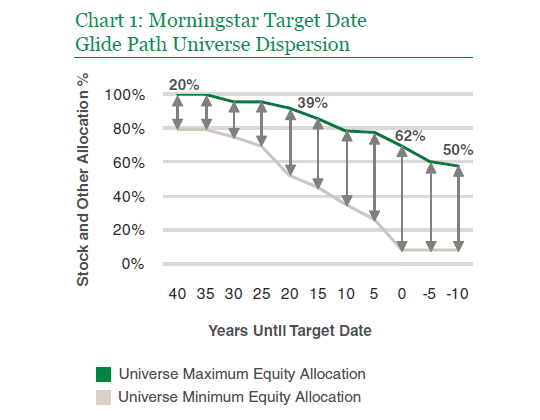

For example, here’s a suggested glide path allocation from Morningstar.

When someone is 30+ years away from retirement, Morningstar suggests holding 80%-100% of their money in stocks. Why? Because stocks tend to have higher returns over long periods of time.

But stocks are also risky. That’s why Morningstar smoothly decreases their suggested stock allocation as one approaches retirement. Someone 15 years away from retiring should have ~50%-80% of their money in stocks. And at 5 years from retirement, between 20%-70% in stocks.

Once in retirement, Morningstar suggests no more than a 60% allocation in stocks. It’s too risky to lose a huge portion of your nest egg in a nasty stock market crash.

Each step down the glide path requires rebalancing. In this case, it means selling high-risk assets in favor of safer, low-risk assets.

Gliding in for Landing

Rebalancing your portfolio might cost you some profit percentage points. Or it might not. That’s not the point.

Because it will also reduce your risk and ensure your portfolio is properly allocated at all times. It’s a smart thing to do, especially as you glide toward retirement.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

“And at 5 years from retirement, between 20%-70% in stocks.” – That seems like a quite an expansive range. Who might be best suited to the 70% besides just , “I am willing to accept more risk” type folks? – Or is it more function of bear vs. bull market? Thanks for the post!

Hi Big Woods Soap! It really is a matter of risk tolerance. It has litte to do with the current state of the market (e.g. bull or bear).

The difference between Morningstar’s ‘aggressive’ glide path and their ‘conservative’ glide path is about 40%-50%.

More stocks = more risk. If you can stomach that 70% of your portfolio might drop by 50% in the next stock market crash…then maybe the agressive path is for you. It’s that kinda thing…

Here’s a great resource from the Boglehead’s: https://www.bogleheads.org/wiki/Glide_paths

Good summary, Jesse.

I also have a guide about this – in the end it will increase risk adjusted returns, but definitely worth having some kind of discipline around it be it time rebalancing or threshold based

Cheers,

Raph