One of the most common questions I receive from readers like you—especially since Grow (Acorns + CNBC) published my story last week—asks me how I invest.

All this theoretical investing information is fine, Jesse. But can you please just tell me what you do with your money.

That’s what I’ll do today. Here’s a complete breakdown of how I invest, how the numbers line up, and why I make the choices I make.

Disclaimer

Of course, please take my advice with a grain of salt. Why?

My strategy is based upon my financial situation. It is not intended to be prescriptive of your financial situation.

I’ve hesitated writing this before because it feels one step removed from “How I Vote” and “How I Pray.” It’s personal. I don’t want to lead you down a path that’s wrong for you. And I don’t want to “show off” my own choices.

All I can promise you today is transparency. I’ll be clear with you. I’ll answer any follow-up questions you have. And then you can decide for yourself what to do with that information.

Are we clear?

Let’s get to the good stuff.

How I Invest, and In What Accounts…?

In this section, I’ll detail how much I save for investing. Then the next two sections will describe why I use the investing accounts I use (e.g. 401(k), Roth IRA) and which investment choices I make (e.g. stocks, bonds).

How much I save, and in what accounts:

- 401(k)—The U.S. government has placed a limit of $22,500 on employee-deferred contributions in 2020 (for my age group). In past years, I’d aim for that full limit. Due to my recent housing purchase, I doubt I’ll hit it in 2023.

- 401(k) matching—My employer will match 100% of my 401(k) contributions until they’ve contributed 4% of my total salary.

- Roth IRA—The U.S. government has placed a limit of $6,500 on Roth IRA contributions (for my earnings range) in 2023. I am aiming to hit the full $6,500 limit.

- Health Savings Account—The U.S. government gives tremendous tax benefits for saving in Health Savings Accounts. And if you don’t use that money for medical reasons, you can use it like an investment account later in life. I aim to hit the full $3,500 limit in 2023.

- Taxable brokerage account—After I achieved my emergency fund goal (about 6 months’ of living expenses saved in a high-yield savings account), I started putting some extra money towards my taxable brokerage account.

In 2023, I’m aiming for $20,000 new investment dollars per year. But a lot of that money is actually “free.” I’ll explain that below.

Enjoying this article? Subscribe below to get new articles emailed straight to your inbox

Why Those Accounts?

The 401(k) Account

First, let’s talk about why and how I invest using a 401(k) account. There are three huge reasons.

First, I pay less tax—and so can you. Based on federal tax brackets and state tax brackets, my marginal tax rate is about 30%. For each additional dollar I earn, about 30 cents go directly to various government bodies. But by contributing to my 401(k), I get to save those dollars before taxes are removed. So I save about 30% off up to $22,500 = $6,750 off my tax bill.

Editor’s Note: The original version of this article incorrectly stated that 401(k) contributions are taken out prior to OASDI (a.k.a. social security) taxes. That claim was incorrect. 401(k) contributions occur only after OASDI taxes are assessed.

Many thanks to regular reader Nick for catching that error.

Second, the 401(k) contributions are removed before I ever see them. I’m never tempted to spend that money because I never see it in my bank account. This simple psychological trick makes saving easy to adhere to.

Third, I get 401(k) matching. This is free money from my employer. As I mentioned above, this equates to about $4,000 of free money for me.

Roth Individual Retirement Account (IRA)

Why do I also use a Roth IRA?

Unlike a 401(k), a Roth IRA is funded using post-tax dollars. I’ve already paid my 30% plus OASDI taxes, and then I put money into my Roth. But the Roth money grows tax-free.

Let’s fast-forward 30 years to when I want to access those Roth IRA savings and profits. I won’t pay any income tax (~30%) on any dividends. I won’t pay capital gains tax (~15%) if I sell the investments at a profit.

I’m hoping my 30-year investment might grow by 8x (that’s based on historical market returns). That would grow this year’s $6500 contribution up to $54000—or about $47500 in growth. And what’s ~15% of $47500? About $7,100 in future tax savings.

Health Savings Account (H.S.A.)

The H.S.A. account has tax-breaks on the front (36.7%, for me) and on the back (15%, for me). I’m netting about $1300 up-front via an H.S.A, and $4,200 in the future (similar logic to the Roth IRA).

Taxable Brokerage Account

And finally, there’s the brokerage account, or taxable account. This is a “normal” investing account (mine is with Fidelity). There are no tax incentives, no matching funds from my employer. I pay normal taxes up front, and I’ll pay taxes on all the profits way out in the future. But I’d rather have money grow and be taxed than not grow at all.

Money Invested = Money Saved

In summary, I use 401(k) plus employer matching, Roth IRA, and H.S.A. accounts to save:

- About $8,000 in tax dollars today

- About $4,000 of free money today

- And about $11,300 in future tax dollars, using reasonable investment growth assumptions

That’s just tax savings. Don’t forget, I still get to access the investing principal and whatever returns those investments produce.

I choose to invest a lot today because I know it saves me money both today and tomorrow. That’s a high-level thought-process behind how I invest.

How I Invest: Which Investment Choices Do I Make?

We’ve now discussed 401(k) accounts, Roth IRAs, H.S.A. accounts, and taxable brokerage accounts. These accounts differ in their tax rules and withdrawal rules.

But within any of these accounts, one usually has different choices of investment assets. Typical assets include:

- Stocks, like shares of Apple or General Electric.

- Bonds, which are where someone else borrows your money and you earn interest on their debt. Common bonds give you access to Federal debt, state or municipality debt, or corporate debt.

- Real estate, typically via real estate investment trusts (REITs)

- Commodities, like gold, beef, oil or orange juice

Here are the asset choices that I have access to in my various accounts:

- 401(k)—my employer works with Fidelity to provide me with about 20 different mutual funds and index funds to invest in.

- Roth IRA—this account is something that I set up. I can invest in just about anything I want to. Individual stocks, index funds, pork belly futures etc.

- H.S.A.—this is through my employer, too. As such, I have limited options. But thankfully I have low-cost index fund options.

- Taxable brokerage account—I set this account up. As such, I can invest in just about any asset I want to.

My Choice—Diversity2

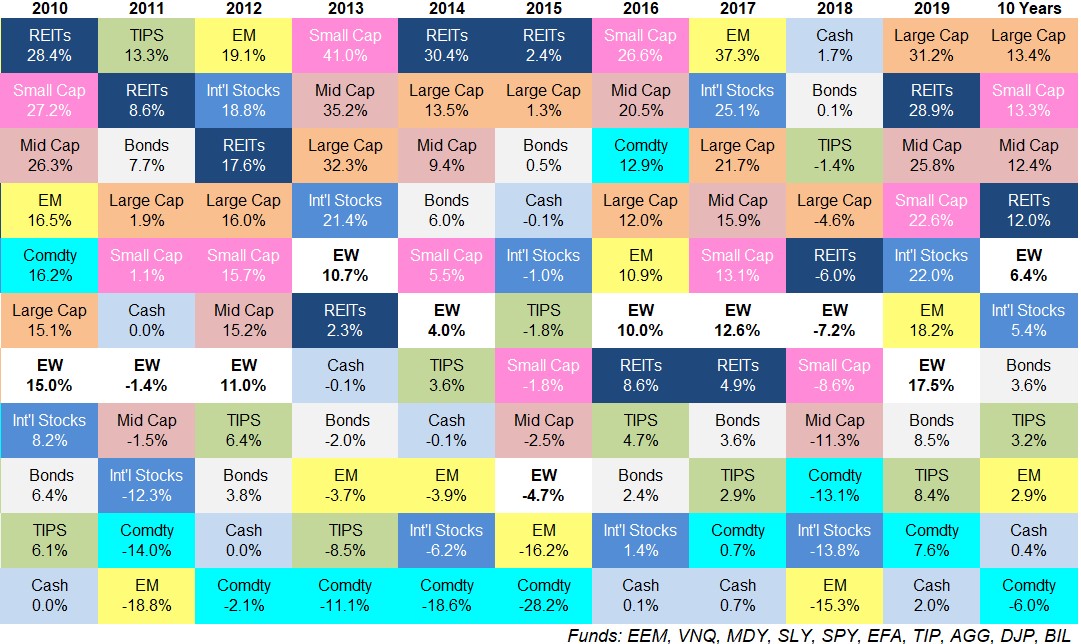

How I invest and my personal choices involve two layers of diversification. A diverse investing portfolio aims to decrease risk while maintaining long-term investing profits.

The first level of diversification is that I utilize index funds. Regular readers will be intimately familiar with my feelings for index funds (here 28 unique articles where I’ve mentioned them).

By nature, an index fund reduces the investor’s exposure to “too many eggs in one basket.” For example, my S&P 500 index fund invests in all S&P 500 companies, whether they have been performing well or not. One stellar or terrible company won’t have a drastic impact on my portfolio.

But, investing only in an S&P 500 index fund still carries risk. Namely, it’s the risk that the S&P 500 is full of “large” companies’ stocks—and history has proven that “large” companies tend to rise and fall together. They’re correlated to one another. That’s not diverse!

Lazy Portfolio

To battle this anti-diversity, how I invest is to choose a few different index funds. Specifically, my investments are split between:

- Large U.S. stock index fund—about 40% of my portfolio (example: FXAIX)

- Mid and small U.S. stock index fund—about 20% of my portfolio (ex: FSSNX, FSMDX)

- International stocks fund—about 20% (ex: FSPSX)

- Bond index fund—about 10% (ex: FTBFX)

- Various alternatives (about 10% of the portfolio), which provide true asset class diversification compared to the stocks and bonds above. These assets would be part of an “Investing 201” class. You can still accomplish a lot without them.

This is my “lazy portfolio.” I spread my money around five different asset classes and let the economy take care of the rest.

Each year will likely see some asset classes doing great. Others doing poorly. Overall, the goal is to create a steady net increase.

Twice a year, I “re-balance” my portfolio. I adjust my assets’ percentages back to 40/20/20/20. This negates the potential for one “egg” in my basket growing too large. Re-balancing also acts as a natural mechanism to “sell high” and “buy low,” since I sell some of my “hottest” asset classes in order to purchase some of the “coldest” asset classes.

Any Other Investments?

In June 2019, I wrote a quick piece with some thoughts on cryptocurrency. As I stated then, I hold about $1000 worth of cryptocurrency, as a holdover from some—ahem—experimentation in 2016. I don’t include this in my long-term investing plans.

I am paying off a mortgage on my house. But I don’t consider my house to be an investment. I didn’t buy it to make money and won’t sell it in order to retire.

On the side, I own about $2000 worth of collectible cards. I am not planning my retirement around this. I do not include it in my portfolio. In my opinion, it’s like owning a classic car, old coins, or stamps. It’s fun. I like it. And if I can sell them in the future for profit, that’s just gravy on top.

Summary of How I Invest

Let’s summarize some of the numbers from above.

Depending on the year and the other expenditures in my life, I aim to save and invest anywhere from $10,000 to $50,000 per year. Much if it is literally free (employer match), or provides immediate tax savings (401k), or provides long-term tax savings (Roth IRA).

I take that money and invest it across different asset classes, diversifying within those asset classes too, via the following allocations:

- 40% into a large-cap U.S. stock index fund

- 20% into a medium- and small-cap U.S. stock index fund

- 20% into an international stock index fund

- 10% into a bond index fund

- 10% into various alternative investments

The goal is to achieve long-term growth while spreading my eggs across a few different baskets.

And that’s it! That’s how I invest. If you have any questions, please leave a comment below or drop me an email.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

Interesting read! Do you apply the 40/20/20/20 ratios across each type of investment (ira/401/hsa/taxable)? I.e. each investment type consists of the 4 different types of index funds with the ratios above. Any reason you went with this approach vs. target date funds in everything and a robo-advisor like Betterment for the taxable account?

Hey Mike, great questions.

Do I apply 40/20/20/20 across each account?

No, I don’t. Not all of my accounts are flexible in terms of what investments they offer (I go over a few details in the article). Not each account has a bond fund or an international fund that I can choose. Instead, I look at all my accounts and re-balance them twice a year so that–in sum–I achieve the 40/20/20/20 ratio.

Why my approach and not a target data fund

At the end of the day, it’s mostly personal preference. There’s a small argument to be made that my manual Lazy Portfolio has lower fees than most target date funds and robo-advisor. But they’re just barely lower. Between reading The Boglehead’s Guide to Investing and A Random Walk Down Wall Street, I’ve convinced myself that I can manage my own fund choices. But if you’d rather invest in a target date or robo-advisor, I would 100% encourage that. The similarities are far more consequential than the differences.

Thanks for sharing some real world information, most articles only talk strategy. This is very helpful to those just starting out and those of us that have been moving towards retirement for a while now.

I appreciate you recognizing that your way is not the only but your still brave enough to share.

Rich! Thanks for the kind words. I appreciate you reading and taking the time to respond.

All the best,

Jesse

Hey Jesse – as always, great stuff.

Half as food for thought and half selfishly justifying the very noble profession of financial planning…

You probably already do this but have you considered aligning your assets held with the type of account you’re holding? For example, holding bonds in a taxable account is going to spin off interest at ordinary income rates to you versus a more growth oriented portfolio which won’t trigger tax until sold? Hold the most aggressive in your Roth as you get to keep all growth and your most conservative in the 401(k) which Uncle Sam is going to take a cut of things down the road.

Hey Craig – this is excellent feedback, and it’s not something I thought much about until the past couple years.

The short answer: yes, I have thought about that, and I think I’ve implemented it fairly well. Interested to hear your thoughts.

My HSA is small and 100% stocks. I don’t have many fund options anyway.

My taxable/brokerage account is also small has the 40/20/20/20 split (maybe this is dumb, though! e.g. Why have bonds here?)

My Roth IRA is about 10x in size compared to the HSA and taxable brokerage. It’s 100% stocks.

My traditional 401(k) is the largest account, and I use it flexibly to ensure that I’ve achieved an OVERALL split of 40/20/20/20. So it has a slightly higher bond percentage to make up for the fact that my Roth IRA has no bonds.

What do you think? Doesn’t have to be ‘professional’ advice 🙂

Another reader—Mike—asked a semi-related question here too.

Love it, thanks for sharing! It is so helpful for people to see real-world information about how people are investing. And, I appreciate how you are telling us what you do, but are open minded that other options have “consequential similarities” (love that, found it in your reply to a comment.

5-stars

I think people sometimes run the risk of overusing 401s and IRAs when they are young and have the ability to make large annual contributions. It depends how you envision your life evolving and whether you think you’ll work a salaried job until your IRA/401 becomes touchable – but what happens if you get rich before you’re 60? What happens if you have plenty of money to retire but all of it is trapped in an account that can’t be used until a specific date?

And this isn’t just empty rhetoric. Let’s say someone is 30 with $200,000 and they’re able to invest $41,000 annually like you. If they made 10% per year, they’d have $3.7 million by 50. What if they wanted to retire and couldn’t because it’s trapped inside an IRA? And they should be able to live on that – even finding 5% bonds would give them $185,000 of annual income.

Paradoxically IRAs don’t make as much sense for those that plan to max them out, as these are likely fairly engaged and motivated investors that have a far higher likelihood of achieving financial independence well before the arbitrary time period contained within an IRA.

Hi Cody – thanks for the thoughtful comment! You raise some excellent points that people should be considering, and I appreciate you bringing those to light for other readers.

First, I’d point you to what Craig Gingerich wrote below. He brings up the IRS allowance “Substantially Equal Periodic Payments” that might (or might not) change your view.

But there’s a second point here. The money isn’t “trapped” in an IRA. It simply subject to a penalty if you withdraw early.

So an important question is, “Is the early withdrawal penalty *worse* than paying taxes on a ‘normal’ taxable brokerage account?”

We aren’t the first to have asked this question.

The answer is: typically, the tax-advantaged accounts perform better EVEN IF you end up paying early withdrawal penalties. Utilizing Roth conversions and/or SEPP 72(t) distributions play a big role in making this true.

In other words: for most people, there’s no excuse not to max out your tax-advantaged accounts.

Hey Cody – I think your concern is definitely real, but in your specific example the IRS allows “Substantially Equal Periodic Payments” for those individuals who are in a position to retire before the traditional 59 1/2 age. Doesn’t change the general concern of if you don’t have a stereotypical retirement in mind that 401k’s and IRA can make it tricky. I picture something like wanting to start a business or more sporadic time off, a year to travel Europe, then back to work, 6 months in Costa Rica, then return to the workforce. Qualified accounts are terrible for that.

Another great article with lots of good info here!

Thanks Div Power! I appreciate your returning readership 🙂

Ayyy, MTG investing…like it! I used to play regularly but don’t have anything that valuable over maybe $40. I liked collecting the Swords (Feast and Famine, Ice and Fire etc.).

I have quite a few fun vintage Stat Wars and old niche video game pieces which are worth a fair bit, but like you said they’re more fun than an actual investment.

Ohh cool! Yeah, there’s a lot of money in old collectibles. About ~10 years ago I bought some MTG commons from Alpha and Beta. They’ve increased 20x to 50x since then. It’s crazy.

Great article! Good information with explainations laid out in a logical way with visuals spread throughout. Also pointing out MtG as a fun hobby first and possible investment last is great advice. I believe too many people justify overspending on hobbies as an “investment” without thinking or tracking it.

I’m assuming you use a traditional 401k but do use a RIRA because your workplace doesn’t offer R401k?

Hey TH! Thanks for reading, thanks for the kind words, and thanks for the thoughtful question! That’s many thanks haha

Agreed on the MtG stuff. Those cards could disappear tomorrow, and I’d be ok with it. It’s a weird market anyway…their value is completely dependent on how many people out there are playing, who want the cards. So if the publishing company–WOTC–starts making the game un-fun and players start leaving, then my ‘investment’ would be affected. That’s why it’s not worth taking it seriously as an ‘investment,’ IMO

As for your 401k question, exactly.

Employer offers a traditonal 401k, but no Roth 401k.

I use a Roth IRA to try to balance the post-tax/pre-tax allocations in my portfolio.

Thanks Jesse, reading you from El Salvador.

Great article, very helpful real investing information you shared. It is really appreciated.

Thanks Felipe! Glad it helped you, and hope to hear from you again.

-Jesse

Second blog post I’m reading since finding your site, I hope the last for today (hard to stop with such good ideas and writing style)

It’s 00:30 where I’m reading from and also where I’m reading from there is no 401k or other fancy way of saving money, and very few vanguard or great brookers available.

I have to invest in foreign currency and take that risk on too.

I’m 2 years starting with something that should be a couch potato pasive portfolio of stock & bonds.

I have an allocation idea but really like the one you presented

I’m doing 20/80 stocks&bonds , EUR & USD and under that 1/N across for the stocks part 1/N for the bonds pârț, mostly because I don’t have logic to determine diferent and because I read it in a book about risk and shortcut to handeling it.

N =nr of different stock ETFs & nr of different bonds ETFs.

2 years is still the start and I Find it harder & harder to not try smth differrent like the one you have.

Any words of wisdom for my overthinking investing brain?

Razvan! Good to hear from you, my friend.

First, thanks so much for reading! I’m very glad you find my writing entertaining and educational 🙂

Second – I am not an expert on investing in Romania, you’ll have to forgive me!

But I’ll help how I can!

How old are you?

And what are your investing goals?

I basically try to invest with XTB & eTorro, we just can’t buy Vanguard and some other US ETFs (just the CFD version for them). So I’m not really investing in Romania (just investing from Romania in US & European market)

I’m planing to invest in the RO stock market (just got elevated to emerging market, 2 companies got into FTSE 100 index, just 10% flat tax on profit and very good track record, but just a hand full of very big companies that are very very sensitive to politics and law changes), but for now I don’t consider I have the time to learn and to invest directly in stocks (there are no ETFs for the RO (BVB) market.

I’m 33 soon. My initial plan was to double my money in 10 years and buy a flat to rent, but the more I read to more I’m discouraged about that since it’s not really passive and there’s a whole lot of headache and work to make that work and then there’s the compound interest that just gets better and better after 10 years.

So now I’m switching focus (hence thoughts about allocation strategy and reading a lot, looking for some answers) and looking to a bigger horizon (30 years) – basically retirement and if things go well maybe early retirement if I can cover more than 60% of my living expense from investments.

I like the idea of finding a strategy and letting it work for you, I’m 90% convinced that the more I thinker with things the more I’m exposing myself to mistakes and the more I’ll “buy what I don’t understand”, so I’m currently buy&hold and just looking out for the next covid size drop to take advantage maybe with selling bonds and buying stocks with DCA.

But for now I wanted your thoughts on the 1/N idea of allocation because it’s very simple (I like to keep things simple) and from reading a few things it’s not a bad one (just that it’s stating to do 1/N across different types of investments – not doing that right now)

The thing is that it doesn’t seem to be very popular, every portfolio I found always has different allocations for different markets / types of stock etc. (from the big well know portfolios to bloggers like yourself and others)

I’ve been thinking about it but I couldn’t find a rationale to help me decide X % in US stock , Y% in this and to keep that for the long run. I mean how can I decide to put more in US market for the next 20 years VS another one ? I seems just like a gamble I can’t find “solid” arguments to say that this is a “winning” bet VS another.

Hope that’s enough info to give you a better picture of where I’m at.

Salut (cheers)!

Hi Jesse,

It’s good to re-read things, it helps as a reminder to not tinker and complicate things, to keep me on track and only deviate with very strong reasons.

I was just born in the wrong place for investing (ish).

I’m not investing in Romania, I’m just investing from Romania.

I’m investing with eTorro & XTB on US / Euro markets, broad market ETFs (basically trying to capture market returns).

Also the BVB (RO stock market) is getting attractive: 5% flat tax on dividends, 10% flat tax on profit, large companies with great dividend yields but, infrastructure companies that are very very sensitive to whatever the politicians are saying / doing.

I’m not yet ready to invest in individual stocks.

I’m 33 and I don’t have a very specific goal (you could say retirement) .

I aim to beat inflation at least and grow enough so my investments can sustain the largest part of my expenses (>60%).

My set growth / year right now is 8%

I was attracted to FIRE early on but, then I realized I like the work I do and being employed for now and I don’t want and can’t really save that aggressively (I have a family and I want to enjoy life also now 🙂 ).

Goal: build a nest egg big enough so I can cover most of my expense around retirement (when I’m 50-60 years old). I do realized that if some life event comes along that requires money the egg is going to get slightly cracked.

Long story short, I keep seeing portfolios with X% in S&P then Y% in this , Z% in that.

My only allocation strategy is 20% bonds / 80% stocks which will drift towards bonds the closer I get to 60 years.

But from there I can’t find a rationale to tell me that it’s better to put more money in X than Y especially since I’m looking to come to a fix number or ETFs and just increase positions over time.

How can I come to a rationale that tells me it’s better to make a bigger bet on lets say STOXX 600 vs S&P500 for the next 20 years ?

Hence my 1/N allocation, I now 1/N is for splitting across different (unrelated) investment types, but basically I’m using it because I’m saying “I can’t decide otherwise”

Just wanted your thoughts on this (1/N splitting), if you have “material” on this you recommend please share, criticism is highly welcomed as well.

P.S. The 1/N is not from an investment/money book it’s from “Risk savvy”

( https://www.goodreads.com/book/show/18114056-risk-savvy )

Hey Razvan – so, “How can I come to a rationale that tells me it’s better to make a bigger bet on lets say STOXX 600 vs S&P500 for the next 20 years ?”

My two cents:

I have neither the time nor the expertise to predict the next 20 years’ performance of U.S. large cap (S&P) vs. Euro large cap (Stoxx).

I’m sure there are some folks out there who *do* predict those performances. Read what they have to say, and see if it makes sense to you.

If you’re still unsure what to do, it’s hard to go *too* far wrong using a diversified approach, e.g. a Lazy Portfolio.

And what does that sound like? A bit like yoIur 1/N approach.

I’d recommend “A Random Walk Down Wall Street” and “Bogleheads Guide to Investing” – two phenomenal books.

-Jesse