I grew up east of Rochester, in Upstate New York’s apple country. New York produces ~30 million bushels of apples per year, second among the 50 states (behind Washington).

But apples start to rot 5-7 days after they’re picked. So how does New York harvest 30 million bushels of apples in September and October without eating 30 million bushels over the following week?

The answer is cold storage.

Apples can be stored near 35°F for 6-12 months without decay. We gain an entire year of “freshness!” But first, we must put forth an effort of time, resources, and money to build that cold storage infrastructure.

Today’s effort allows us to keep more of our harvest in the long run. We get to choose our consumption schedule, not Mother Nature.

Roth Conversions

It might seem like an odd transition, but the same concept applies to Roth conversions. Today’s planning can allow us to keep more of our “harvest” in the long run. We gain control over our tax schedule rather than leaving it entirely up to the IRS.

Roth conversions are among many tools in a good “tax planning toolbelt.” Done correctly, Roth conversions allow an investor to turn high tax rates in the future into lower tax rates today. This article was inspired by Catherine (a listener of our podcast, Personal Finance for Long-Term Investors), who wrote me the following email:

Can you please explain the connection between RMDs and Roth conversions? Is this something I should look into? I’m 57, single, and have ~$2.3M in my 401k right now.

We tackled Roth conversions in both Episode 81 and Episode 99; find both below!

An Example: Required Minimum Distributions

Most retirees have heard of required minimum distributions, or RMDs, which are mandatory withdrawals that individuals with tax-deferred retirement accounts, like Traditional IRAs and 401(k)s, must make once they reach a specific age.

RMDs are forced. You must withdraw money from your 401k. Thus, the income tax associated with RMDs is forced. That’s not ideal.

Let’s use Catherine as an example. She’ll start taking RMDs at age 73 (although Congress might change that minimum age, as they’ve done before). That’s 16 years from her current age 57.

We don’t know the rest of Catherine’s scenario. Her Roth assets, taxable assets, Social Security, etc. are a mystery to us. So is her monthly spending need. All that info is essential to proper planning!

But I want to be extreme, so we’ll say Catherine’s lifestyle is wholly supported by her Social Security, taxable assets, and Roth assets. She doesn’t withdraw a single dollar from her 401k. Thus, it will grow from $2.3M today to $6M by the time she’s 73 (the assumption: 16 years at 6% per year).

Now in 2040, it’s time for her first RMD.

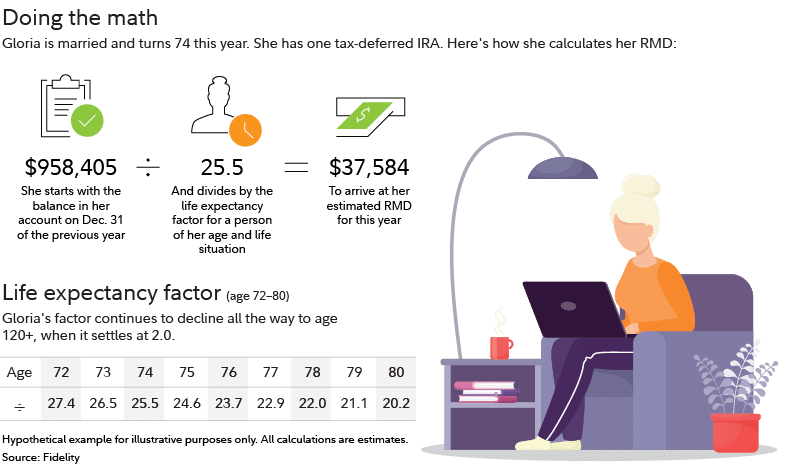

To calculate that RMD, we’ll look at Catherine’s year-end account value from the prior year ($6.0M) and divide it by her age-based Life Expectancy Factor. For age 73, that factor is presently 26.5. Here’s the full table of Life Expectancy Factors.

Catherine’s RMD is $6M / 26.5 = $226,415

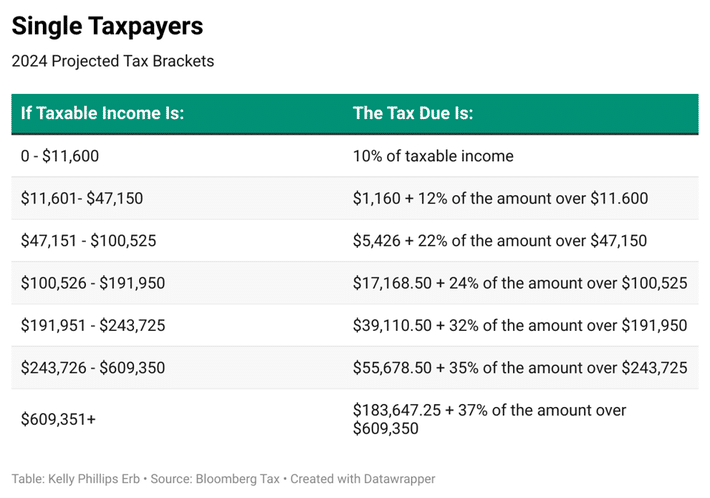

That entire RMD is taxable as income, so her marginal Federal tax bracket is 32% based on the current tax code.

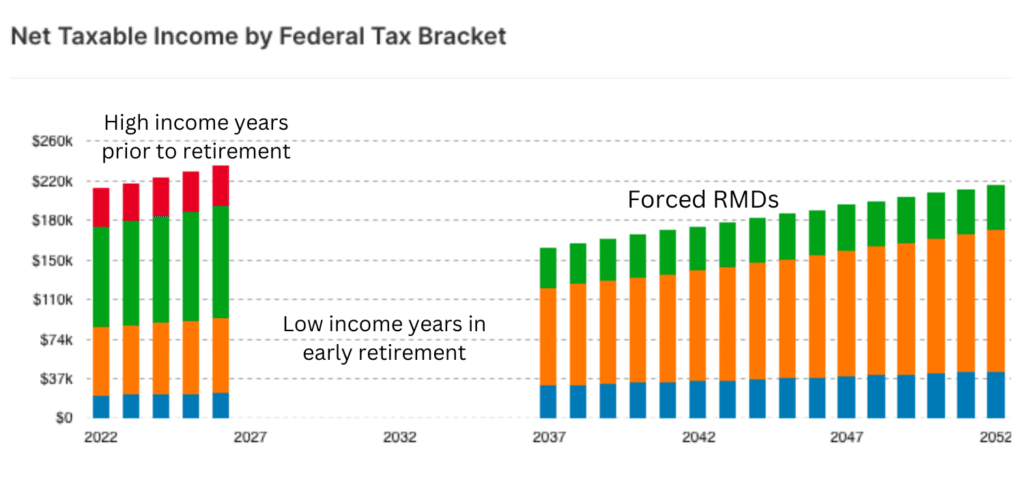

I’d bet Catherine’s account continues to grow past 2040, despite the RMD withdrawals. Her first 10 RMDs are all in the 4-5% range, and we’d expect her investment growth to outpace that. Her RMDs will grow in size. And that means she’ll be paying higher and higher marginal taxes in the 32% bracket, the 35% bracket, and potentially even the 37% bracket.

How Can Roth Conversions Help?

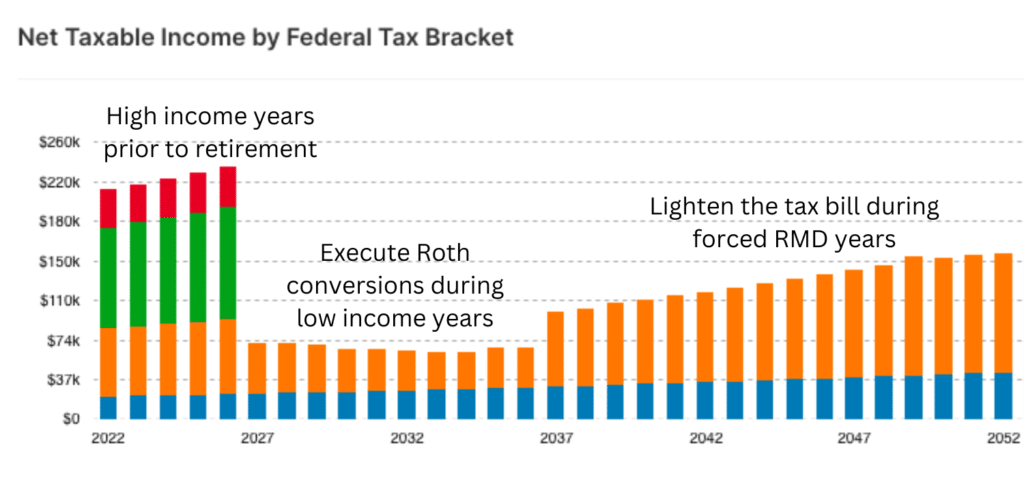

Paying high tax rates on RMDs is like letting your apples rot during the glut of harvest season. We need a “cold storage” to gain control over our tax rates and spread those taxes over time.

So let’s return to 2024, while Catherine is still 57 and her 401(k) is still at $2.3M. How do Roth conversions work?

First, we need to ensure Catherine’s 401(k) – which is still active – allows “in-service Roth conversions.” If it doesn’t, Catherine will have to wait until she retires and rolls over the 401(k) into an IRA.

Some simple paperwork with Catherine’s custodian will allow her to convert a number (of her choosing) of Traditional dollars into Roth dollars. Since the Traditional dollars have never been taxed, this conversion is taxable, triggering income tax.

Those converted Roth dollars will never be taxed again! That’s fantastic. But did Catherine save money? Was this a smart move?

We’d want to know all of Catherine’s personal financial details to run an accurate analysis, but we certainly need to understand what Catherine’s tax rate is today.

Her 2024 regular taxable income is $100,000, so she’s paying Federal taxes in the marginal 24% bracket. And she has another $90,000 available in that 24% bracket this year.

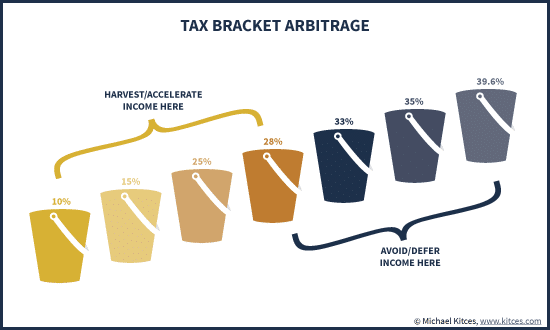

We can fill that ~$90,000 space in her 24% bracket with Roth conversions. Catherine would pay 24% Federal tax on those dollars today to prevent 32% (or higher) marginal tax rates once her RMDs hit. That’s the essence of Roth conversions.

Not Too Much Roth Conversion

Catherine needs to be careful not to overdo it. And so should you.

If you’re in your high-earning years and paying high marginal taxes, the odds are Roth conversions don’t make sense for you right now. There’s no reason to move extra income into your current high tax years.

But! You might have a few low-income years as soon as you retire. Your W2 income will disappear. Your financial plan might dictate you delay Social Security for a while.

Your only income might be dividends and income from your Taxable accounts and small withdrawals from your Traditional accounts. If so, fill up those low tax brackets with Roth conversions! This is a very common strategy for new retirees.

What If…?

But even as I write this article, “What if…” questions are bombarding my head.

Retirement planning withdrawal strategies are far from one-dimensional, and what I’m describing today is a one-dimensional view. I’m only focusing on a few details to provide an example of Roth conversions. Other nuanced planning questions include:

- When should I start taking Social Security?

- Should I be worried about Social Security funds decreasing in time?

- How will I pay for Medical expenses in retirement?

- How do I account for inflation in retirement?

- How should my investments be allocated?

- How does a pension fit into retirement?

- Do I need insurance? What types and how much?

- How should I approach estate planning?

Roth conversions and (more generally) tax planning are essential aspects of retirement planning. But just two of many aspects.

A cold-stored apple a day keeps the IRS away.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

I see many articles like this about lowering your tax bracket when doing Roth conversions. But, what about the amount of money that can be made by not doing Roth conversions and letting the taxable money grow in an account like an IRA or 401K? Is that math too hard to explain?

Sure your RMDs will be higher and you will be taxed more, but how much more money will you make by letting that tax deferred money grow? You could assume a rate of return at 6% for the illustration.

Hey Kelly – great question. I might even write an entire article to answer. But imagine these two scenarios…

You have $100.

It grows at 6% per year.

After 20 years, you owe 20% tax on it.

How much do you have?

Scenario 2:

You pay the 20% tax up front and only have $80.

It grows at 6% per year.

After 20 years, you own it all tax free.

How much do you have?

The answer is: you’d have the same exact amount.

And that’s why Roth conversions (paying 12% now instead of 30% later), make sense.

A wise man once said ” never pay a tax before you have to”.

Back around 2015 I had the owner of an income tax service try to convince me to convert all my traditional IRA money to Roth. He said tax rates were going to go up and he was converting all of his own personal traditional IRAs. Fast forward to 2017 and Congress actually ended up lowering tax rates. I wonder what he thought about his conversions after that.

Hey there. Thanks for writing in! Well…

I’m not in the business of predicting tax rate changes, and thus making advice based on that. I disagree with that tax service.

But I am in the business of looking at today’s tax rates and saying,

“If you change nothing, you’ll pay 32% marginal taxes in 10 years…

But if you do this Roth conversion today, you’ll only pay 12% marginal taxes.

And 12% is less than 32%.”

To me, that’s an easy win and terrific advice. But to each their own.

Great article Jesse. I hope you do write an article based off the first question. If my wife and I are retired at 58 with 4.5 million and have no income until I’m 59.5 other than 20k from dividends in my brokerage account and we’re using 120k from a money market until I’m 59.5 for the rest of our yearly expenses of 140k, I’ll be in a low tax bracket. Roth conversions probably make sense, as I’ll be paying the conversion taxes from that same money market and possibly selling some equities (long term holdings) to rebalance and pay some of those taxes too. I figure we’ll be in about the 22% tax bracket even with the conversions. That’s likely lower than if we let the money grow tax free, but I’m not sure. It’s hard to take that conversion money out and watch my balance drop, but probably better in the long run.

Jesse,

I just recently found your site and podcasts and I am very impressed! I have very much enjoyed you content.

I’m 61, retired and have found two things have finally sold me on doing Roth conversions this year:

* Your blog here with the good charts: https://bestinterest.blog/roth-is-better-than-traditional/

* And the Schwab Roth IRA Conversion Calculator: https://www.schwab.com/ira/ira-calculators/roth-ira-conversion

Even with my spouse still working, I don’t think we’ll hit the IRMAA limits while I do Roth conversions before I take Medicare. But, could Roth conversions now help me avoid the IRMAA thresholds when I’m taking RMDs in the future? Or, is it worth doing Roth conversions to avoid the IRMAA thresholds? I’d be interested in an article like that.

Thank you for all of the good content!

Kelly

Hi Kelly, thanks for those kind words.

Short answer:

– yes, Roth conversions can help you avoid IRMAA later by moving future tax dollars into current tax years.

– but be careful. Overdoing Roth conversions now can actually trigger IRMAA now (again, because you’re moving taxable income into current years)

– and remember: IRMAA math has a two year delay. 2024 IRMAA premiums are based on 2023 modified adjusted gross income (MAGI). What you do this year (2024) will matter for 2026 IRMAA premiums.

for more specifics, you should consult with a CFP professional.

I’ll add your idea to my article content list!

best,

Jesse

Enjoy your site and blog posts. My wife and I (filing jointly) are in the 24% marginal tax bracket. I’ve not yet converted any of our traditional 401-k/IRA to Roth. As we are likely in our highest earning years I just can’t make the math work overwhelmingly to cause me to want to convert a significant sum. Am I missing something?

Hi there. Thanks for writing in.

If you’re in your highest earning years, then your thinking is right on. You shouldn’t do Roth conversions when you’re already at your highest tax brackets.

Best,

Jesse