Let’s discuss the proper way to account for inflation in retirement and FIRE planning.

I lurk in some online personal finance forums, and what I see scares me. I see “the blind leading the blind” discussing how to account for inflation as part of your retirement or financial independence plan.

These mistakes can be gut-wrenching. If you double-count inflation, you’ll assume a worse-than-real future and mistakenly believe retirement is impossible. But if you improperly discount inflation, you’ll assume a better-than-real future and torpedo your retirement with false hopes.

We’re going to fix that today.

What’s the Problem in the First Place?

The problem is that it’s challenging to understand if/when/how to apply inflation. It’s entirely understandable. Inflation is a weird phenomenon and the math isn’t intuitive.

Should you inflate your current salary into the future? What about your current spending? What about investment returns? You’ve probably heard of the 4% Rule; but how does inflation affect its usage?

All great questions. We’ll answer them all today.

The True World vs. The Convenient World

I’ve heard intelligent people tackle this concept before. It’s tough. Lots of numbers are involved. There are mysterious rules about when to apply those numbers and when not to. My friends Cody Garrett and Brad Barrett expertly tackled this topic on a recent episode of ChooseFI. :

As I listened to Cody and Brad, I thought: a few visual aids and analogies might help here.

My preferred analogy is what I call “The True World” vs. “The Convenient World.”

“The True World” involves numbers as they actually exist in our society and economy.

“The Convenient World” involves shortcuts that financial experts frequently use.

I’ll explain both worlds below.

Good news: you can do math in either world and get correct answers for your life. Hooray! This is wonderful. It shows the power of smart mathematics.

Bad news: you cannot flip-flop between worlds. You must do all your math in “The True World” or do all your math in “The Convenient World.”

The problems I see every week arise when DIYers flip-flop between worlds. So I say again: you cannot flip-flop between worlds!

Let’s describe these worlds.

The True World

Let’s talk about The True World a.k.a. our actual society and economy.

- Inflation: inflation exists in the True World, typically varying between 2% and 4% per year. We don’t know what future inflation will look like. But it’s reasonable to use a benchmark like 3% per year.

- Stock returns: stock returns vary in the True World and can do so by significant amounts. Still, a pattern emerges when we zoom out to large time scales (20+ years). On average, a diversified stock portfolio has returned ~10% per year over long periods. It’s reasonable to use that 10% benchmark for the future. $100 this year turns into $110 next year.

- Important side note: in my financial heart of hearts, you need to understand the data presented in this article to truly realize the volatility of long-term stock investing. It’s more nuanced than my simple “zoom out to 20 years, assume 10% per year” statement.

- In fact (!!) – I am convinced that using a lower number, like 8% nominal returns, is more useful and will be more accurate on a go-forward basis. But I understand why that’s controversial.

- Bond returns: bond returns also vary in the True World, though typically by smaller amounts than stocks. Over the past 100 years, intermediate-term, high-grade bonds have returned ~5% per year. It’s reasonable to use that 5% benchmark for the future. $100 this year turns into $105 next year.

In the three bullets above, I made an interesting assumption: that the future will closely resemble the past. You’re allowed to disagree with me and say, for example, that you want to assume inflation will be 4% ongoing and stock returns will be 8% ongoing. That’s fine.

The critical point is that all your numbers occur here in the True World. Inflation is above zero. Stocks and bond returns are measured using the actual amount of dollars. When we combine these factors, we conclude:

- Your future income will be higher than your current one, increasing with inflation.

- Your future raises will be greater than current, increasing with inflation

- Your future spending will be higher than current, increasing with inflation.

- Your future annual savings will be higher than current, increasing with inflation.

- Your future nest egg will grow by some mix of true-world return percentages (assuming you build a diversified portfolio).

Remember those four components: income, raises, savings & spending, and investment growth.

If you do all of your future planning using “True World” numbers, your analysis results will show reality as it is. That’s the goal.

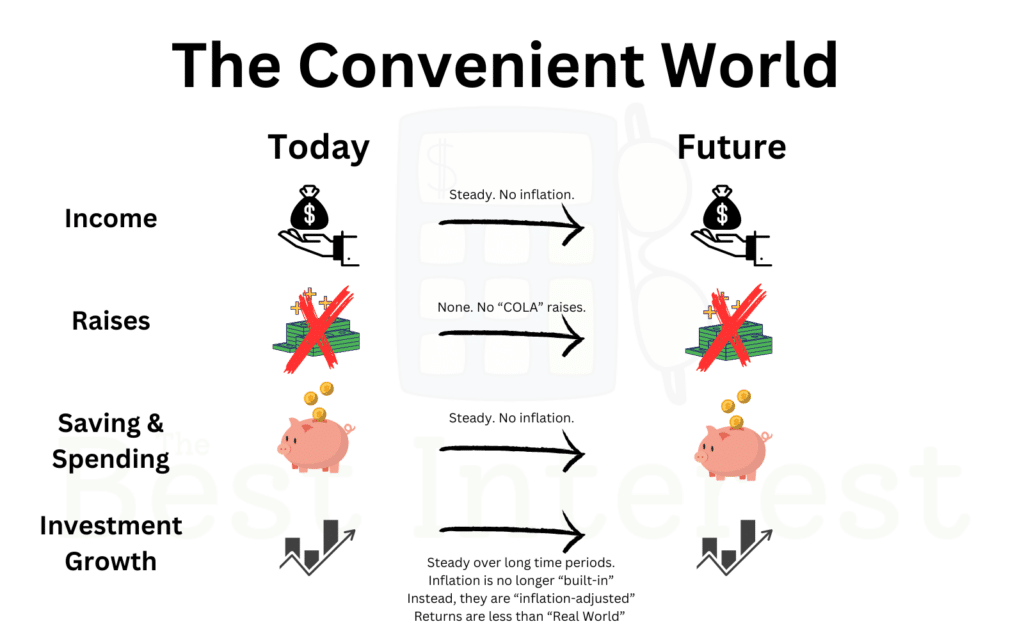

The Convenient World

In the True World, as we’ve seen, everything seems to be adjusted by inflation.

Income increases with inflation.

Raises too.

And saving. And spending.

We are accounting for inflation every step of the way.

This is lame and tedious! Can’t we just do a mathematical trick to remove inflation from the equation entirely?

Yes. That’s exactly right. Some intelligent people wanted to make The True World more convenient for us. We’re here today (discussing a confusing financial planning topic) because of that desire for convenience.

…which, in my opinion, is a great idea! Unfortunately, those good intentions paved the road to our present confusing situation. Those intelligent people said,

“Three of our four main components (income, raises, spending & saving) are adjusted by annual inflation. To make the math easier, let’s remove inflation. No more adjustments! But to even out all facets of the equation, we must also decrease the investment growth by the inflation rate.”

The Convenient World contains no inflation! Here in the Convenient World, our same four components are:

- Your future income will equal your current income (assuming no merit-based raises).

- There are no raises (at least, no “cost of living” or “COLA” raises)

- Your future annual spending & saving will equal your current amounts.

- Your investments will grow by the “true-world returns” minus the annual inflation rate.

There’s no inflation in any of the four factors. While we’ve decreased our future spending needs, we also decrease the amount we save in the future and the rate at which our investments grow. Everything is a bit muted in The Convenient World.

But because we’ve discounted inflation in both positive ways (less future spending) and negative ways (less investment growth), you can do future planning using these “Convenient World” numbers, and your results will show reality as it is.

The math works.

Don’t Believe Me?

“But Jesse! How can the math work if we remove inflation in retirement and FIRE planning?! We’re ignoring a very real phenomenon!”

Trust me. Trust the math. Take a look at this simple spreadsheet.

The True World tab uses true world data. The Convenient World tab removes inflation entirely as I’ve described above.

Both tabs yield the same exact retirement savings results (Column I). The math works.

What About “The 4% Rule?”

The famous 4% rule throws an essential question at us.

As my 4% rule explainer article describes, the 4% rule builds inflation into its math. The creators of the 4% rule told us, “Hey future retiree – don’t you worry about inflation in retirement, we’ve already built it into our mathematical construct. All you need to worry about is hitting your 4% or 25x nest egg goal at your retirement date.”

What’s that sound like? What world washes inflation away? The Convenient World!

Now, the 4% Rule applies starting Day 1 of Retirement and extends until the day you meet Charlie Munger (RIP). That period is covered by the 4% rule (or whatever retirement rule/simulation you choose to utilize).

How should you cover that first period of time, from today to Day 1 of Retirement? I recommend continuing to do all of your math in The Convenient World. Remove inflation from your numbers altogether.

Can you mix and match? While dangerous, the answer is technically “yes…“

To get from Today to Your Retirement Date, you can either:

- Do all your math in The Convenient World, where both your future annual spending AND your future nest egg need will be muted values, but the ratio of those two will be 4% or 25x.

- Do all your math in The True World, where both your future annual spending AND your future nest egg will reflect reality, and the ratio of those two will be 4% or 25x.

You can use True World math to get from Today to Your Retirement Date, and then let the 4% Rule (which is Convenient World math) take over from there.

But you CANNOT mix-and-match True World and Convenient World math when determining how to get from Today to Your Retirement Date. You cannot, for example, increase your future spending by the inflation rate (True World), then also reduce your investment growth by inflation (Convenient World). Don’t do it, I say!

In this example, both True and Convenient math get us to a place where we can start using the 4% Rule.

But – Those Future Nest Egg Amounts Are Different?!

We’re sitting here in 2024. In the example graphic above, The True World tells us we’ll need $3.75M to retire in 2040. The Convenient World tells us we’ll need $1.875M. Those two numbers are vastly different…so which one is right?

The way to think about that is:

- We’ll need $1.875M to retire as measured in 2024 dollars

- We’ll need $3.75M to retire as measured in 2040 dollars

Either way, the most important takeaway from these planning analyses is to understand what we need to do in 2024 to hit these future goals. Then we can revisit in 2025, 2026, etc.

Thankfully, both True and Convenient math will inform us precisely what we need to do in 2024. For example, both methods would tell us, “You need to save $30,000 in 2024 to stay on track for your retirement goal.”

What About “Real” vs. “Nominal” Returns

You might have heard of “real returns” and “nominal returns” before. I use those terms regularly here on The Best Interest, but I’ve intentionally excluded them so far in our discussion of inflation in retirement and FIRE planning.

The reason is that “real returns” confuses my analogy of “The True World.” Ugh.

Investment professionals use the term “nominal returns” to describe the actual dollar amounts that investments are increasing/decreasing by. If $100 turns into $110, the nominal return is 10%. In other words, nominal returns exist in The True World.

Investment pros use “real returns” to describe whether investments increase your purchasing power. In other words, have the investments outperformed inflation? If $100 turns into $110, but there is also 4% inflation, the real return is ~5.77%. “Real returns” exist in The Convenient World.

Yes, it’s confusing. You’ve been warned. Good luck.

Lessons and Takeaways

What have we learned?

- Inflation in retirement and FIRE planning is a touchy topic. It’s not intuitive or easy. In fact, it requires great attention to detail.

- You can use True World numbers and get all the answers you need.

- You can use Convenient World math that excludes inflation and get the answers you need.

- I recommend against mixing and matching. That said, if you’re very comfortable with the math, you can mix-and-match and end up fine.

- You don’t want to mess this up. Misapplying inflation (a ~3% annual mistake) compounded over decades will lead you to a dark place.

Talk to an expert if you need to. CFP financial planners know how to handle this. Modern financial planning software takes care of the math for you.

Go get ’em!

PS: Here’s a straightforward financial independence and 4% rule calculator where you can input your own data.

PPS – you’ll notice my calculator does all its math in The Convenient World!

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

Where is your current debt section on your worksheet? Such as consumer, educational or real estate? Seems odd not to ask for that data.

You should include your monthly debt payments right now as part of Row 11. That takes care of any current debt you have.

If you plan on paying off your debt before FIREing, then you should *not* include debt payments as part of Row 13.

Isn’t there a risk here in not using the true world numbers. For example in your infographic it shows that in the convenient world, I hold everything constant and need 1.875 million, which is fine for setting up the plan, but the money in your accounts grows nominally and when checking to see if you can pull the trigger on retirement, you need to have 3.5 million to meet the 4% rule. Am I missing something?

Hi Matt, great question. I had that same thought. If you revisit the article, look for the section titled But – Those Future Nest Egg Amounts Are Different?!

It contains precisely the answer you’re looking for.

The biggest misunderstanding I’ve seen on this topic is “locking in” on a FIRE number. It’s fine to use “convenient world” analysis and project 25x your current expenses to ask the question, “do I have enough to retire TODAY?” It’s also good to use this as a rough directional guideline for how much longer it might take to get into the retirement zone.

However, if one takes their 25x value from today’s expenses, multiplies by 25 and “locks in” that target such that as soon as their retirement funds reach this specific target value (potentially decades later), then they can retire — well, now real vs convenient worlds have been mixed inappropriately. One’s true retirement threshold (FI number) needs to be recalculated using up-to-date real-world numbers as time goes on.

Absolutely correct. I agree. At one point in the article, I discuss this idea and write:

Thanks so much for your spreadsheet and the work involved in creating it. I have a question about SSI. If I know I will get some SSI as well as my husband, our needs in later years will be lower as we will have some income covered with SSI. Can the spreadsheet account for future SSI? Alternatively, should I upwardly adjust my withdrawal rate to account for the reality that I can take more early as later I can take less to account for SSI? what do you suggest?

Great question.

The short answer: my spreadsheet tool isn’t complicated enough to handle the variable retirement income brought about by SSI.

If I were you, play around with cell B13 “Annual Withdrawal when FIREd”

Adjust that between the two extremes: no SSI ever, and full SSI your whole retirement. That, at least, provides you with a spectrum of results. The “real” result lies somewhere in the middle of that spectrum.

I do think there are more detailed FIRE calculators on the Internet, much for advanced than mine, which can properly account for your question.

Best,

Jesse