Readers had some awesome questions after my recent post about after-tax returns.

The summary of the article is that for long-term, diversified stock investing, I use the following after-tax, real return estimates:

- In Roth (“tax-free”) accounts, 6% per year.

- In Traditional (“tax-deferred”) accounts, 5% per year.

- In taxable accounts, 3% per year.

Again, these are post-tax and real (accounting for inflation) returns.

Reader Joaquin wrote in and asked:

With regards to a recent blog post you did, I’m confused on why I always hear about Traditonal 401k accounts instead of Roth. It appears to me that, if you’re investing for the long term, that Roth accounts will give you better returns (i.e. I will be able to take out more cash from a Roth account upon retiring versus a Traditional 401k account (assuming same amount of money invested monthly)). If this is correct, shouldn’t I invest all my money into a Roth account instead of a Traditional 401k?

Joaquin

Amazing question! After all, I wrote that Roth accounts have a higher real return that Traditional accounts. Right? We have to be nuanced here. I’m going to explain two quick scenarios to illustrate a subtle, but important, point.

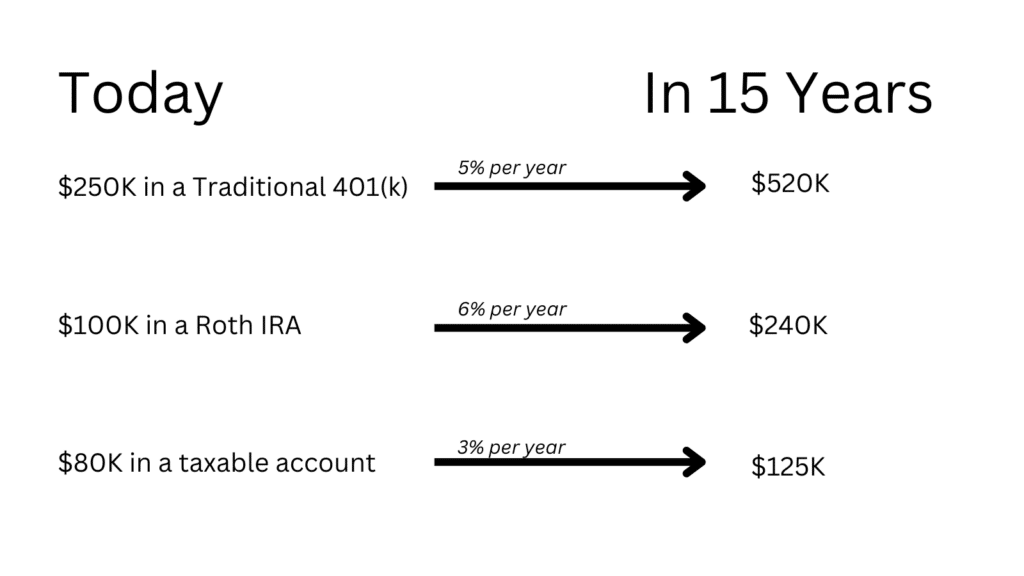

Scenario 1: Dorothy is a 45-year-old woman with the following assets.

- $250K in a Traditional 401(k)

- $100K in a Roth IRA

- $80K in a taxable account

…and all of these dollars are invested in a diversified stock portfolio. She wants to project how these assets might grow by the time she’s 60, assuming she doesn’t add another dime.

Since Dorothy’s money is already placed into specific accounts**, I would use the estimated returns I wrote about last week. Her long-term, after-tax, real portfolio value could be estimated as:

- $250K * 15 years @ 5% per year = $520K

- $100K * 15 years @ 6% per year = $240K

- $80K * 15 years @ 3% per year = $125K

**This is the important caveat.

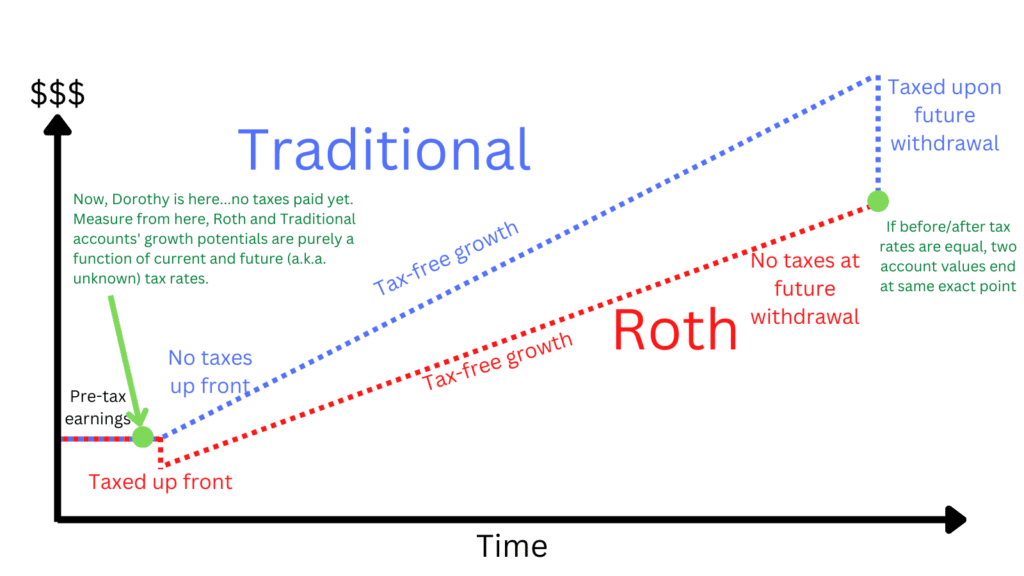

Now let’s look at Scenario 2: Dorothy has $20,000 budgeted for 2023 investment savings. Which accounts should her dollars go into? It’s time for nuance!

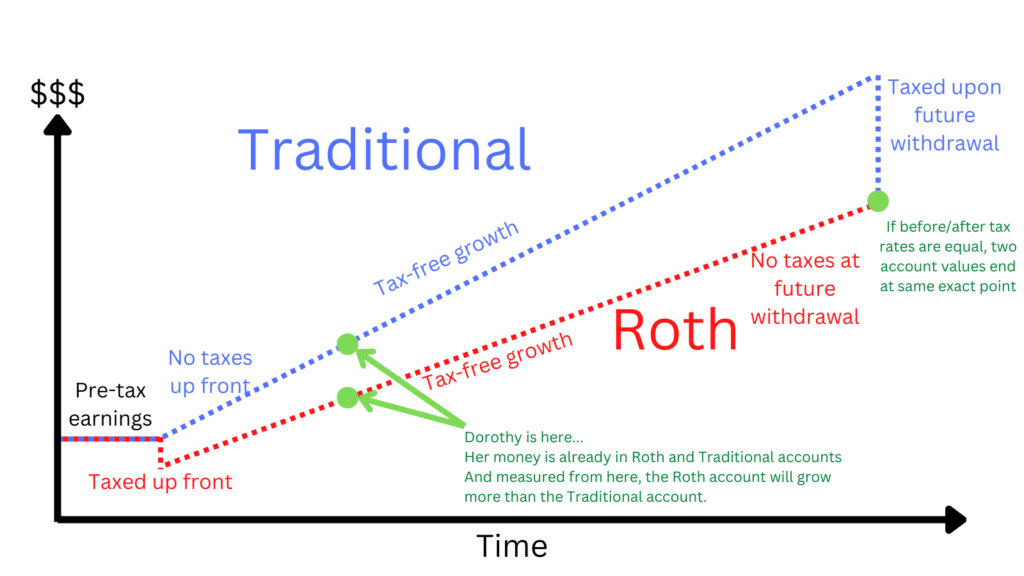

This money has not been placed in any specific accounts yet. She hasn’t earned the money. As of now, it’s all pre-tax dollars. This is different than Scenario 1. So we need to do some tax analysis. Roth accounts and Traditional accounts are “equal, but opposite” in terms of their tax treatment.

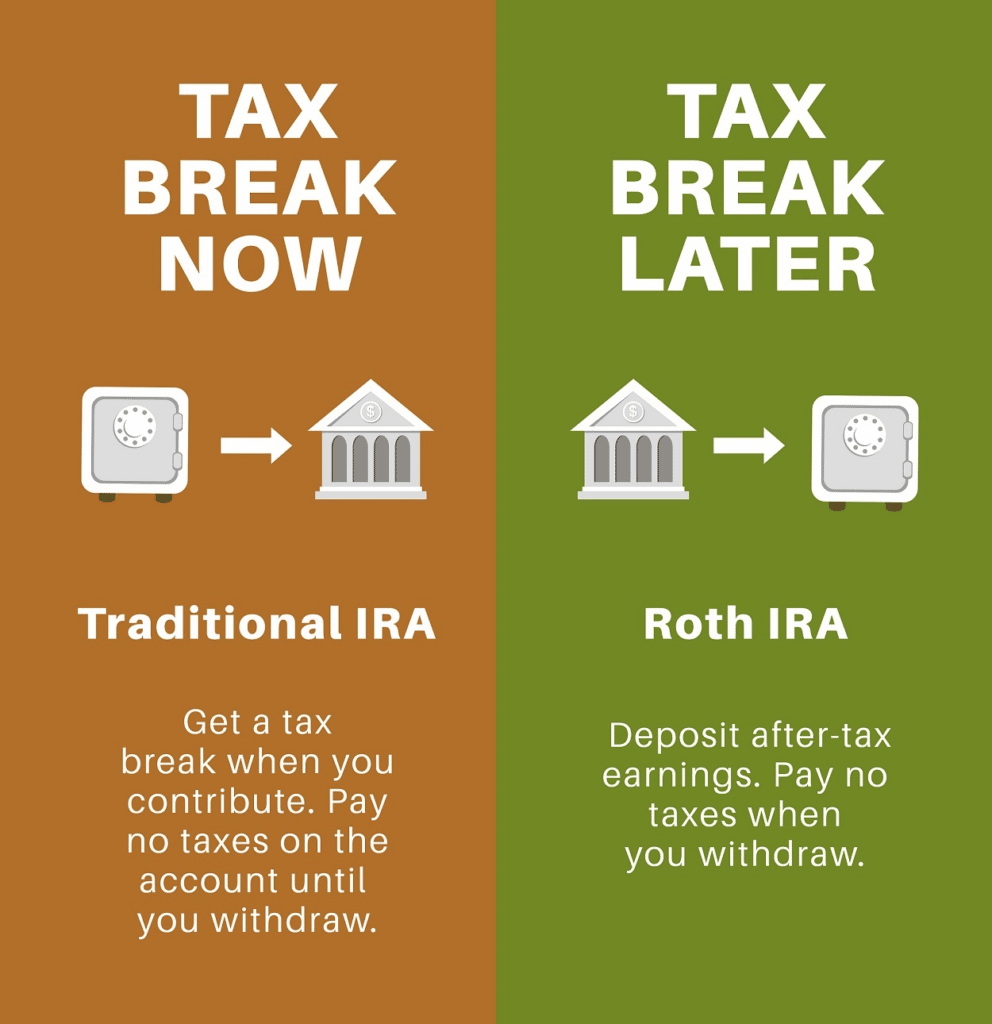

Roth dollars pay taxes today. Traditional dollars do not. That’s good for Traditional dollars.

But Roth dollars have no future taxes. Traditional dollars do. That’s good for Roth dollars. And this is why, once money is already placed inside these two accounts, Roth accounts have better long-term returns than Traditional accounts. Traditional dollars pay future taxes, hurting their long-term returns.

But if our “starting line” is drawn before money is placed into the accounts, then Roth and Traditional accounts are “equal.” The debate between the two becomes completely about tax rates. Here’s an example:

- Imagine a world where taxes are always 25%.

- Dorothy earns $200 and splits it between Roth and Traditional, $100 and $100.

- The Roth dollars are taxed today down to $75, but the Traditional dollars are tax-deferred and stay at $100.

- All the dollars are invested in stocks and grow at a nominal 10% per year.

- After 20 years, the Roth account is worth $505 and the Traditional is worth $673.

- Dorothy withdraws the money. The Roth account is tax-free and Dorothy receives the full $505. The Traditional account is taxed at 25% and Dorothy only receives…$505. The two accounts are exactly the same!

What if taxes aren’t always 25%? Current taxes are considered low by historical standards, so let’s assume taxes go up in the future.

- Imagine a world where taxes are 20% today and 30% in the future.

- Dorothy earns $200 and splits it between Roth and Traditional.

- The Roth dollars are taxed today down to $80, but the Traditional dollars are tax-deferred and stay at $100.

- All the dollars are invested in stocks and grow at a nominal 10% per year.

- After 20 years, the Roth account is worth $538 and the Traditional is worth $673.

- She withdraws the money. The Roth account is tax-free and Dorothy gets the full $538. The Traditional account is taxed at 30% and Dorothy only receives…$471. Roth > Traditional.

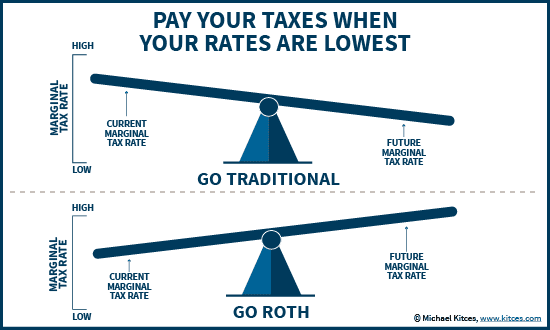

Lesson: if future tax rates are higher than current tax rates, then funding Roth accounts make more sense than Traditional accounts.

The opposite is true too. If future tax rates are lower than current tax rates, then funding Traditional accounts make more sense than Roth accounts.

This allows you to “pay your taxes when your rates are lowest.”

My crystal ball is murky though. I’m not sure how Federal tax rates will change in the future.

However, it’s reasonable to think that most of us will increase our earnings as we grow older, pushing us into higher tax brackets. In other words, our future taxes will be higher than our current taxes. That’s a pro-Roth fact.

So, as reader Joaquin asked, should we fund our Roth accounts before Traditional?

One more important point! We need to talk about 401(k) matching. 98% of 401(k) accounts having matching – this is free money. And it’s (almost) always worth maximizing your free money.

The ideas in today’s article have guided me to how I invest my dollars:

- First, I invest in my Traditional 401(k) to get the full match. Get that free money.

- Then I max my Roth IRA to the annual limit.

- Then I continue investing in my Traditional 401(k) until the annual limit.

- Then I invest in my taxable account.

Roth accounts aren’t inherently better than Traditional accounts. It’s all a matter of taxes. Thanks for the great question, Joaquin!

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!