I didn’t know how to pronounce Les Miserables until 2017. Now I know all the songs. My wife bought us tickets to the show for my birthday this year. What a triumphant masterpiece! 99% of children dislike art museums, musicals, and reading the news. But many adults find beauty or intrigue in those same ideas.

A similar “boring-to-not-boring” transition happens in personal finance. The problem is that the fun doesn’t last. We had fun getting our personal finances under control. We got hooked on that fun. It lasted for months or even a few years. Money went from a scary unknown to an exciting area of optimization.

But then we got it all figured out and…well, the thrill is gone as B.B. King sang. And thus you find yourself here, on a .blog domain. Who uses .blog?!

Don’t despair. The lack of financial fun is a good thing. It’s a sign that your finances are in a great place.

But I still find fun financial things to think about and learn. There are a few traditionally “boring” topics that I find exciting. I’ll share them below, and maybe you’ll be intrigued too.

Get to Know Your Taxes

Can it get more boring than taxes?!

Actually, I like taxes. Over the past two years, I’ve realized that the tax code is half puzzle and half game, and I love puzzles and games.

The rules are well-defined (but there are a lot of them). I certainly do not know all the rules, but the more rules I learn, the better my “strategies” become.

The “pieces” interact in different (and sometimes surprising) ways. There are always multiple ways to “solve” a tax problem. Some solutions decrease this year’s taxes, and others decrease future taxes. Sometimes, we trade off lots of effort and paperwork to save a few bucks; is that a worthwhile trade?

If you’re a young W2 worker (like me), there’s not too much to know. Our tax scenario is fairly simple.

But if you’re a retiree earning Social Security income, making IRA withdrawals, realizing short and long-term capital gains, earning interest, dividends, and more, you’ve got an interesting puzzle before you! The interactions on a simple 1040 Federal Tax return can be quite complex and involve thousands of tax dollars per year.

If you’re a business owner or a real estate investor, the “puzzle” intensifies! This is why a good CPA accountant is worth their weight in gold.

To be clear, tax planning is not about cheating the tax system. When accountants tell me they’re “aggressive,” I take it as a euphemism for “I bend the tax code until it breaks.” That’s bad—and usually illegal. Avoid that. If you’re an honest accountant, please find a different word than “aggressive.”

But working with a tax professional who 1) knows the “rules” of the tax code and 2) enjoys optimally “solving the puzzle” you bring to them…well, odds are they can solve your puzzle much better than you can alone.

Pro tip: starting this year, review your 1040 Federal Tax Return (or your country’s equivalent)…try to go line-by-line, and if you don’t understand what a particular line item means, look it up.

Wait. For A Decade or Two.

The Best Interest is a big proponent of long-term investing, which, as you might have noticed, includes the verbiage “long-term.”

We’re not talking weeks or months. We measure in decades. We beat a slow-tempo’d drum of basic tenets, like “buy and hold” and “diversify” and “don’t look for needles, buy the whole haystack.“

BORING!

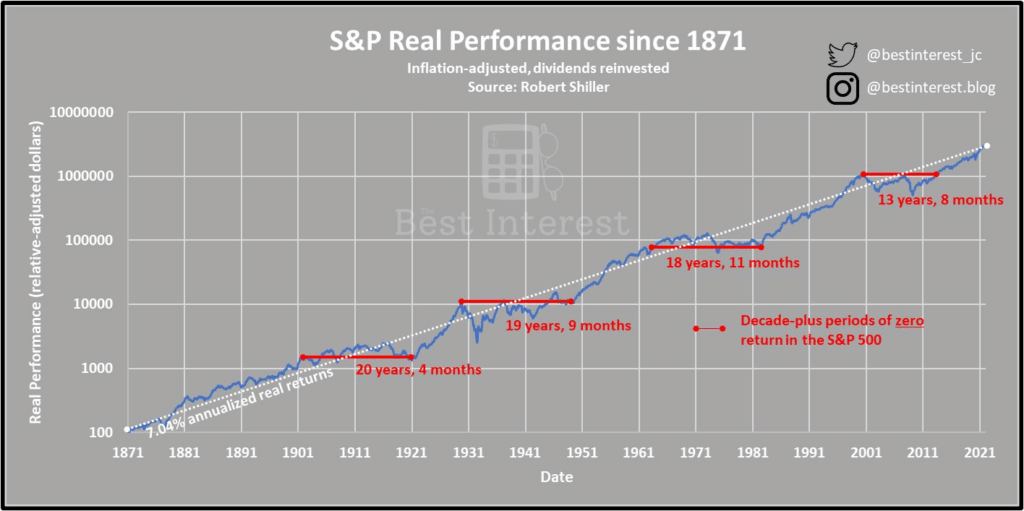

To spice things up, I like to remind myself (and you) of market history. One of my favorite cautionary tales is that returns are never promised, and we’ve suffered decades of zero returns.

In that article linked directly above, I put together this chart:

WOW! Multiple ~20 year periods of zero return?!

As I’ve realized in hindsight, there’s a problem with that chart. Everything is factually correct, but the chart presents data differently than most people think. I inflation-adjusted the data. In other words, the chart does not measure dollars and cents. It measures purchasing power.

There have been multi-decade periods when investors’ purchasing power was stagnant. Their accounts increased in value, but inflation ate the entirety of those gains.

Most of us, though, measure our accounts in dollars and cents. We understand the reality of inflation, constantly knawing at our purchasing power. But we don’t inflation-adjust our conception of the world. If $1.00 grows to $2.00, we see exactly that. We don’t say, “…but inflation was 14%, so really it’s like I only have $1.86.”

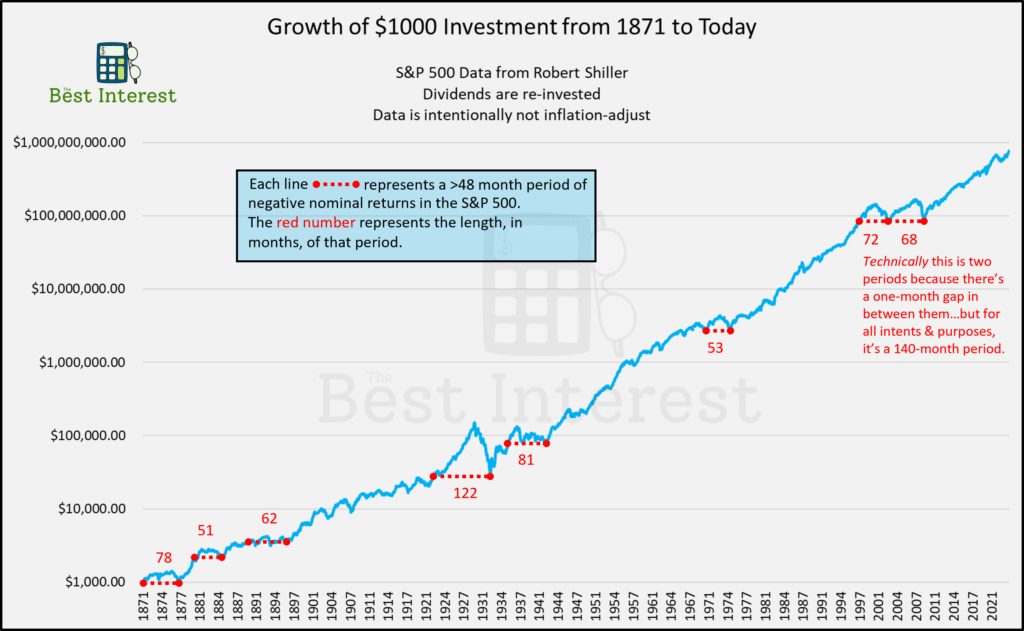

To fix this problem, I reconstructed the plot to show nominal dollars.

If you read my primer on accounting for inflation in retirement, the chart above lives in “the convenient world” while the chart below lives in “the true world.”

The lesson: it’s realistic for your diversified stock portfolio to go through a ~5+ year period of negative nominal returns. If you’re unlucky, it might stretch out to 10+ years!

Now that’s exciting (in the same way BASE jumping is exciting).

It’s a far stretch from the lazy shorthand of “the S&P returns 10% year!” that too many FinFluencers use. I’ve been guilty of that shorthand, and I understand its usage when calculating 30-year compound math.

I despise that shorthand, though, when I hear it used to explain expected stock market returns to a new investor. New investors need to know that stock investing is not a smooth ride. It’s not always up and to the right. It involves years – if not decades – of what feels like wasted time.

5 years is a long time. 10 years, per math, is longer. Are you excited to stay the course that long through thick and thin?

Important note: this analysis looked at a lump sum investment. Dollar-cost averaging, though, smooths this ride out immensely! In fact, DCA actually takes advantage of bad times and volatility. I’m a huge fan of DCA’d monthly contributions through thick and thin.

Know Your Flow

Cashflow is the cinder block of personal finance.

It’s boring and basic and plain and every other synonym thereof.

But it’s also foundational.

You cannot build strong personal finances without healthy cash flow, and you won’t know if you have healthy cash flow unless you measure it.

Buy Protection

Speaking of BASE jumping…

The exciting part of extreme sports is “the jump” itself. But it’s someone’s job to consider the “boring” questions like,

- “Is that parachute packed correctly?”

- “Can that bungee cable support a 300-pound man?”

- “If he doesn’t make it and lands in the pit of burning tires, what’s the rescue plan?”

Ok. That’s kind of funny. But on a more serious note, about the modern miracles of CPR and AED?

Christian Eriksen is a Danish soccer player, currently on the roster for Manchester United. On June 12, 2021, Eriksen had a cardiac arrest during a national team game against Finland. 50 years ago, he would be dead. But because the training staff is both CPR-trained and well-equipped with a automated external defibrillator (AED), Eriksen’s heart was shocked (one shock!) back to life. He’s still plays today.

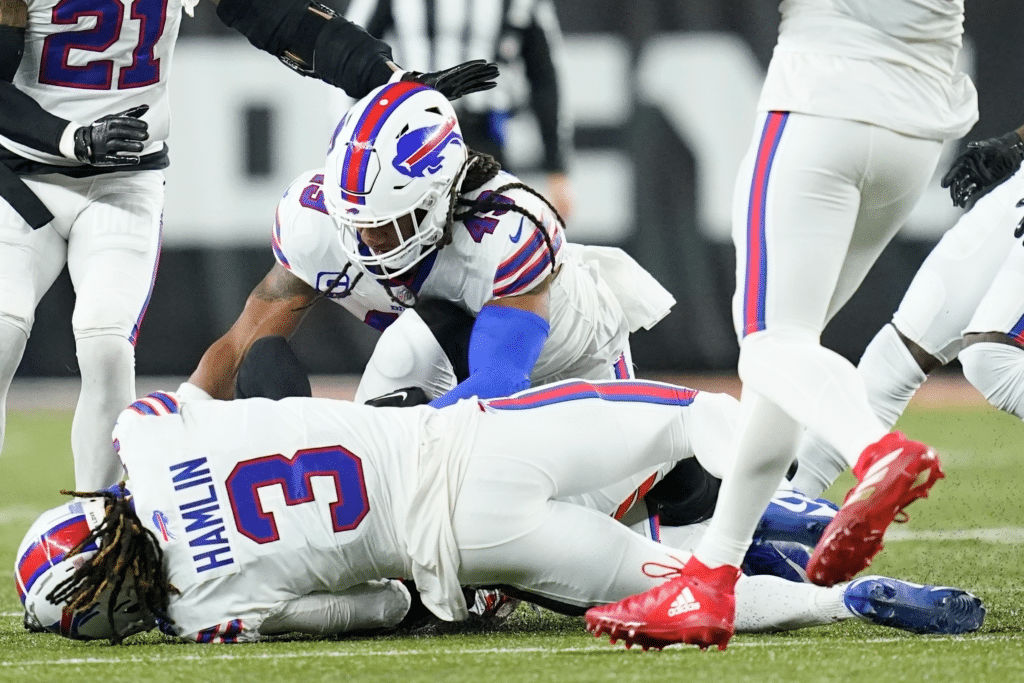

A similar cardiac arrest happened to Damar Hamlin in a Buffalo Bills football game in January 2023. Again, an AED shocked his heart back to life. He’s alive and well and still playing football.

These might be 1-in-10000 events. Easy odds to ignore, right? But asking, “What happens if…” can lead you to some life-saving answers. A little preparation goes a long way.

The personal finance world skews less life-and-death than cardiac arrest, but some of the financial “Q&A” will point you toward:

- A well-funded emergency fund.

- Life insurance (term only!)

- Home and auto insurance

- Disability insurance

- An umbrella insurance policy

If you’re unsure what kind of insurance you do (or don’t) need, ask yourself:

If something bad happened on [this axis], do I have the assets needed to pay for it?

- If I died, would my family have the assets and cash flow to continue our desired lifestyle? If not, you need life insurance.

- If I got disabled and couldn’t work…

- If my house burned to the ground or got swept away in a hurricane…

- If I got sued when the mailman trips on my sidewalk…

- Etc. etc.

If you don’t have the assets to cover your liability, you need insurance.

You Made It. Go Live Life!

If everything in your finances feels boring, that’s a good thing. You’ve reached the top.

There are plenty of nuanced topics to nosedive into.

Or, you can just go live your life. Go check out a musical or a museum. Another story must begin!

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!