After I wrote a simple primer on Roth conversions a couple weeks ago, several readers reached out asking for more details. A few specific snippets of those questions include:

I see many articles like this about lowering your tax bracket when doing Roth conversions. But, what about the amount of money that can be made by not doing Roth conversions and letting the taxable [sic: qualified, or not taxable] money grow in an account like an IRA or 401K? Is that math too hard to explain?

Sure your RMDs will be higher and you will be taxed more, but how much more money will you make by letting that tax deferred money grow? You could assume a rate of return at 6% for the illustration.

Kelly M., Question 1

A wise man once said “never pay a tax before you have to.”

Bob, Question 2

Back around 2015 I had the owner of an income tax service try to convince me to convert all my traditional IRA money to Roth. He said tax rates were going to go up and he was converting all of his own personal traditional IRAs. Fast forward to 2017 and Congress actually ended up lowering tax rates. I wonder what he thought about his conversions after that.

Even with my spouse still working, I don’t think we’ll hit the IRMAA limits while I do Roth conversions before I take Medicare. But, could Roth conversions now help me avoid the IRMAA thresholds when I’m taking RMDs in the future? Or, is it worth doing Roth conversions to avoid the IRMAA thresholds? I’d be interested in an article like that.

Anonymous, Question 3

To summarize those three questions:

- Does the math of Roth conversions really work?

- But since we don’t know future tax rates, how can we confidently convert assets today?

- What about IRMAA (the income-related monthly adjustment amount), which is an additional Medicare surcharge on high-earners?

Let’s address these questions one at a time.

Does the Math of Roth Conversions Really Work?

Roth conversions involve many moving pieces, as you’ll see in this simple Roth conversion spreadsheet.

Reminder: you can make a copy of the spreadsheet via File >> Make a Copy

There are terrific financial planning software packages that take care of this math. I wanted to present 95% of the good stuff in a free format that you all can look at. Hence, Google Sheets.

Nuanced Tax Interactions

Especially important is the interaction between normal income (via Traditional account withdrawals), capital gains, and Social Security. These taxes interplay in nuanced ways. A simple example:

Let’s say a Single retiree’s annual income is:

- $5000 in interest income

- $5000 in long-term capital gains

- $30,000 in Social Security benefits.

If you plug that into a 1040 tax return, you’ll find that:

- None of that Social Security income is taxable.

- All of the interest and capital gains are enveloped by the Standard deduction

- Resulting in zero taxable income and a $0.00 Federal tax bill.

But if we copied Scenario A and added in $30,000 in Traditional IRA distributions, what happens? I think we all expect that the $30,000 distribution itself must have a taxable component, but you might not know that:

- The IRA distribution affects Social Security taxability. Now, $22,350 of the Social Security income becomes taxable. That’s right. Simply by distributing IRA assets, you’ve now increased how much Social Security you pay taxes on.

- The Standard deduction still helps, but there’s now a remainder of $48,500 in Federal taxable income.

- Resulting in a $5584 Federal tax bill.

It’s not the end of the world. Taxes happen. They pay for our public shared interests.

But part of tax planning is understanding ahead of time what your future tax bills will look like. It’s important to understand how taxes interact. And this is just a simple example!

Measuring Roth Conversion Benefits

Going back to this spreadsheet, you’ll three tabs full of retirement withdrawal math. The Assumptions tab contains important information on our hypothetical retiree’s starting point (e.g. $2.9M in investable assets), their annual spending ($100K), their future assumed growth (5% per year, after adjusting for inflation), and other important numbers.

Note – this math takes place in “the convenient world” where inflation is removed from the math.

Then three tabs are presented with different Roth conversion scenarios, described below:

“Baseline Calculations“

This tab shows a retiree not focused on any conversions

They want to leave to their children both Roth assets (if possible) and taxable assets (on a stepped-up cost basis).

Therefore, they attempt to fund as much of their retirement using Traditional assets as possible

“No Trad Withdrawals”

This tab shows a “worst case” scenario, to help bookend the analysis. This retiree is not pulling any funds from their Traditional accounts (unless necessary). Thus, we’d expect them to have large RMDs and large RMD-related tax bills.

“Reasonable Conversions”

This tab shows a “reasonable” Roth conversion timeline, electing to convert $1.7 million throughout their retirement, while funding their lifestyle using a mix of Traditional, Roth, and taxable assets along the way.

By no means is this “optimized.” But it’s reasonable, and better than the first two scenarios, as we’ll see below.

Pros, Cons, and Results

The three scenarios end up similar in multiple ways.

- Our retiree never has an issue funding their annual lifestyle. This is of utmost importance.

- Our retiree reaches age 90 (“death”) with roughly $5M in each scenario.

But there are important differences (as we’d suspect).

- The Baseline scenario ends with $5.00M. Of that, 27% is Traditional, 35% is Roth, and 34% is Taxable. They’ve paid an effective Federal tax rate of 20.7% throughout retirement.

- The No Traditional Withdrawal scenario ends with $5.20M. Of that, 63% is Tradtional, 0% is Roth, 37% is Taxable. They’ve paid an effective Federal tax rate of 18.8% throughout retirement.

- The Reasonable Conversions scenario ends with $5.17M. 18% is Traditional, 68% is Roth, and 14% is Taxable. They’ve paid an effective Federal tax rate of 13.9% throughout retirement.

The Same, But Different

These three scenarios share many similarities. All three result in successful retirements. But there are important differences.

Our Roth converter paid far fewer taxes and, ultimately, left a majority of their tax dollars to their heirs via Roth vehicles, and thus tax-free.

The No Trad Withdrawal retiree paid 28% effective tax rates in their final years (only going further up in the future) and left 63% of their assets in Traditional accounts with a large asterisk on them.***

***TAXES DUE IN THE FUTURE*** …unless you’re leaving the Traditional IRA assets to, for example, a non-profit charity. But if you’re leaving the Traditional IRA to your kids, they’ll owe taxes when they withdraw the funds.

Long story short: Roth conversions work to your benefit when executed intelligently.

Should You Worry About Leaving Behind Traditional Assets?!

I don’t want to freak you out. Your heirs will appreciate you leaving behind a 401(k) or Traditional IRA for them.

But it’s worth understanding that they’ll owe taxes on that money (usually). Let’s dive into an example with simple math: a $1 million Traditional IRA left to one person (e.g. your child).

That person will most likely set up an Inherited Traditional IRA and (via new-ish rules in the SECURE Act) will have to empty that account by the end of the 10th year after your death. The withdrawals can be raised and lowered during those 10 years. Much like with Roth conversions, it makes sense to take larger withdrawals during otherwise low-income years and vice versa.

But if the beneficiary is in the middle of their career, a series of 10 equal withdrawals makes sense. Some rough math suggests ~$135,000 per year is a reasonable withdrawal amount (based on account growth over the 10 years).

That withdrawal is taxed as income for the beneficiary. If they already earn $100,000 per year of normal income, then taxes will consume ~$41,000 of their annual $135,000 withdrawal. State taxes might take another bite.

Again – I don’t want anyone to cry over the prospect of inheriting $94,000 annually for 10 years. Where can I sign up?! But it’s also worth understanding that 30% of this inheritance goes to Federal taxes.

“Never Pay a Tax Before You Have To”

What about Question #2 from the beginning of the article? Bob wrote in and suggested one should “never pay a tax before you have to.”

While pithy, it’s false.

If you can reasonably front-load low tax rates to prevent later high tax rates, the math supports you. What we’ve covered so far today is clear evidence of that.

Now, in the reader’s defense: I’d rather delay taxes if the dollar amounts are exactly the same. That’s one argument behind the tax-loss harvesting craze: I’d rather pay $100 in taxes in the future than $100 in taxes today.

But Roth conversions work differently. Done well, Roth conversions allow you to pay a 22% tax on $50,000 today to prevent a 37% tax on $100,000 in the future. It’s apples-and-oranges compared to the tax-loss example.

And perhaps the bigger lesson: there are few universal rules in personal finance. The pithy rule that works in one scenario (“never pay a tax before you have to”) might fail miserably in another scenario. Let the math guide you.

But We Don’t Know Future Tax Rates!

That’s right, we don’t.

We don’t know if rates will go up (even more fuel for Roth conversions) or down (acting as headwinds against Roth conversions).

For that reason, the best logic I’ve heard is: act on what you know.

We know the current rates. We’ve been signaled how rates will change at the end of 2025. That’s it.

We do have a historical context, but who knows if that context will be important to our tax future? We know, historically, different Federal administrations have changed rates. And we know, historically, current rates on on the low end of the spectrum.

The entire exercise of financial planning and investing is an admission that we don’t know the future but we’d like to plan for the possible scenarios. Roth conversions are no different.

We don’t know what future tax rates will be. But when I combine our current tax knowledge with the spectrum of possible scenarios, I can see plenty of reasons to execute Roth conversions today.

What About IRMAA?

Irma used to only be a name you’d give to the great-grandmother character in your 11th-grade B-minus fiction story.

No longer! Today, IRMAA has been given new life (which, I bet, was covered by Medicare!)

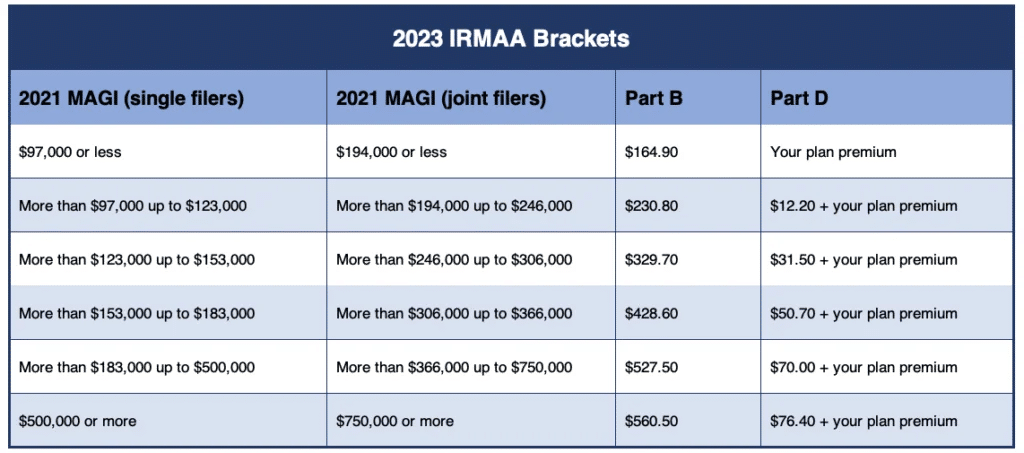

IRMAA (Income-Related Monthly Adjustment Amount) is a Medicare premium surcharge imposed on higher-income beneficiaries in addition to their standard Medicare Part B and Part D premiums. The amount of IRMAA is determined based on an individual’s modified adjusted gross income (MAGI) and can result in higher healthcare costs for those with higher incomes.

In plain English: high-earners pay more for Medicare.

Question #3 today asked if Roth conversions can be used to avoid IRMAA premiums. The answer is: yes.

But first, how painful are these IRMAA surcharges in the first place?!

Important note: you’ll see below that the 2023 IRMAA brackets are based on 2021 modified adjusted gross income (MAGI). That same 2-year delay holds for future years. Your 2024 Roth conversions (or lack thereof) will be important in determining IRMAA in 2026

If a married couple’s MAGI in 2021 was $225,000, they’d end up paying $231 per month (or, more accurately, $462 per month for the couple) as opposed to $330 for the couple if they earned less than $194,000. That’s a difference of $132 per month or $1584 for the year.

I’m of two minds here. Because:

- Yes, I believe in frugality. A penny saved is a penny earned. Why pay $1584 extra if you don’t have to?

- But if you’re earning $200,000 in retirement, do you also need to stress over a $1500 annual line item?

Personally, I’ll be stoked if my retirement MAGI is $200,000. It’ll be a sign that my financial life turned out unbelievably well. I won’t mind the IRMAA.

The people most likely to suffer IRMAA are also best positioned to deal with it.

Will IRMAA Get You?

The 2-year delay in IRMAA math means you might get IRMAA’d early on in retirement.

Imagine retiring at the end of 2023. The peak of your career! You and your spouse earned a combined $300,000 and now you’re settling down to mind your knitting. Like all U.S. citizens, you sign up for Medicare just before you turn 65.

Come 2025, Uncle Sam and Aunt IRMAA are going to look back at your 2023 income and surcharge you.

But the good news, most likely, is that your 2024 income is quite low in comparison and IRMAA will drop off in 2026.

Can Roth Conversions Help?

Remember: RMDs are forced and count as income, and that has the potential of “forcing” IRMAA on retirees as they age.

So to answer our terrific reader question: yes, Roth conversions can help here. You can use Roth conversions to shift the realization of income from high years to low years, preventing or mitigating IRMAA in the process.

But once more, make sure the juice is worth the squeeze.

If a 75-year-old has a $200,000 RMD that kills them on IRMAA, ask yourself: where does a $200,000 RMD come from? Answer: it’s coming from an IRA of over $5 million. Should someone with $5 million be losing sleep over IRMAA? I don’t think so.

That’s A Lot of Numbers…

A long and math-heavy article. I hope this helped you out! We covered:

- Roth conversions can be objectively helpful, decreasing taxes in retirement and shifting large portions of portfolios from Traditional accounts (with potential taxes for heirs) into Roth accounts (no taxes for heirs)

- Taxes in retirement are nuanced and interconnected. In today’s example, realizing extra income (via IRA distributions) also triggered extra Social Security taxes.

- It’s not bad to leave behind Traditional assets to heirs. They’re getting a wonderful gift from you. But there will be taxes, which should be planned for.

- There are many scenarios where it makes sense to pay taxes before you “have” to.

- IRMAA is a negative reality for many retirees, but the people most likely to suffer IRMAA are also best positioned to deal with it.

- Roth conversions can be used to mitigate IRMAA over the long run.

As always, thanks for reading!

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

I’m the author of anonymous #2. I just discovered you recently from Humble Dollar. We chatted a little bit after I signed up for your blog. I’m Bob Wright, I asked if you were a CFP. The wise man I quoted was Bob Brinker, he’s a market timer and had a radio show for decades and still publishes a subscription newsletter. There was a time when I followed him and fortunately for me he got me out of the stock market at almost exactly the high of the market in 2000 and then got me back in about 2 years later at exactly the low point. I don’t know for sure but I suspect that move alone, with compounding, made me 500,000 to a million dollars.

I love your blog. You seem like a very sharp individual. I’ll have to reconsider doing Roth conversions and just ignore IRMAA. I’ll probably leave some of my traditional IRA to my special needs grandson who I believe will be able to take withdrawals over his life expectancy, not subject to the 10-year rule.

Hey Bob! Thanks a bunch for writing. I don’t know Bob Brinker…but maybe I’ll look him up. And very interesting about that great timing and results.

I appreciate the kind words. And yes – there are many special needs situations where normal IRA rules go out the window.

Love your articles.

With regards to “will Irma get you”. If you’ve just retired, and the 2-year look-back is going to have your salary income cause Irma payments. One could file social security form SS-45 to potentially have the Irma payments waived.

Thanks Wayne! Good to know. I’ll check out that SS form.

Best,

JEsse