You might have heard Danny Kahneman died on March 27, at age 90. Today, we’ll discuss his best idea and why it’s so important to long-term investors.

Kahneman (and his late research partner Amos Tversky) revolutionized the understanding of human decision-making with groundbreaking work on cognitive biases and heuristics. Their research, particularly in prospect theory, has profoundly influenced fields ranging from economics to public policy. They won a Nobel Prize for their work.

What’s Prospect Theory?

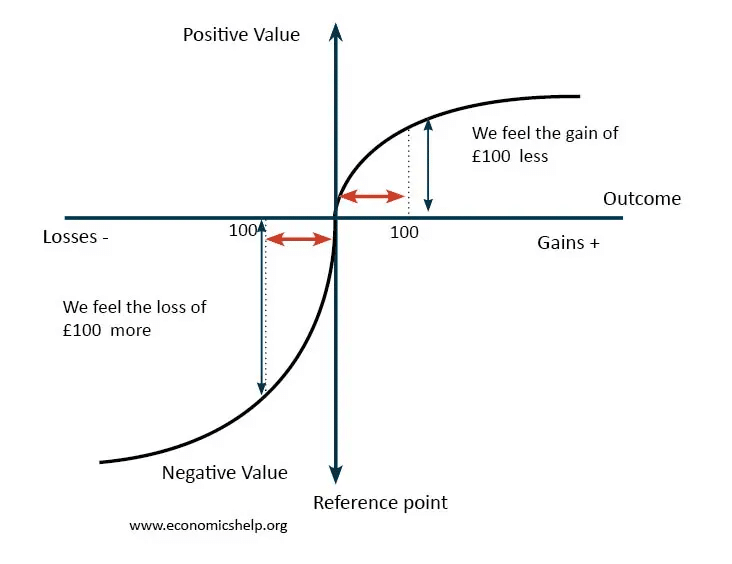

Prospect theory, often called “loss aversion,” turned the world on its head.

Before prospect theory, most economists stuck to “rational choice theory,” which posited that people consistently make decisions that maximize their utility based on rational calculations. They assumed people have stable preferences, perfect information, and make decisions consistently and logically. Individuals were considered rational actors who always made choices that would lead to their greatest overall satisfaction or utility.

But humans aren’t robots. We’re flawed and monkey-brained. We know we shouldn’t eat the cinnamon bun, but we do it anyway. Kahneman (and Tversky) realized this and developed prospect theory.

They suggested that people assess potential gains and losses relative to a reference point, and they tend to weigh losses more heavily than equivalent gains (a.k.a. “loss aversion”). Prospect theory also introduced the concept of “diminishing sensitivity,” where the perceived value of gains and losses decreases as their magnitude increases (example: winning $1000 does not feel 10x as good as winning $100, even though it rationally should).

Prospect theory is a fundamental truth of the human condition. But why should the long-term investor care?

Prospect Theory and The Long-Term Investor

If you’re a long-term investor, you need to understand prospect theory.

It’s a flaw, you see? We care about losing more than we ought to. It’s an irrational bug that you, I, and every other person possess. That bug will weevil its way into our heads and whisper:

- “Your portfolio is down. Time to second guess yourself.“

- “Your portfolio is down. Time to panic.”

- “…run away and then never subject yourself to this again.”

- “…do something (even though it’s suboptimal), and do it now!“

When Emmanuel Kant and Socrates and the Oracle at Delphi all separately said, “Know thyself,” I don’t think they had the stock market in mind. But they were talking about human flaws. To know your flaws is the first step to overcoming them.

Loss aversion is a critical flaw that investors need to be aware of and, if possible, preemptively mitigate.

How to Fight Against Loss Aversion!

The ability to deal with losses is what separates successful investors from unsuccessful investors. You’re in trouble if losses cause you to overreact or make big mistakes at the worst possible moments.

Ben Carlson

I call this “selling to survive.” It’s not a good thing. But how do we preemptively fight against loss aversion? How do we take our irrationality into account before it does us in? We make intelligent allocation decisions.

For starters, Kahneman and Tversky found that the pain of loss was often twice as acute as the joy of winning.

In simple portfolio terms, we should view a 5% loss and a 10% gain as opposite sides of the same coin. Our rational brains might realize the loss is (likely) temporary, but the acute “2x” pain of that loss is quite real. Similarly, the pain of touching a stove doesn’t last forever. We’d still prefer to avoid touching stoves and we’d prefer to avoid acute portfolio pain.

So…annuities?

I don’t think so. Although annuities promise “no losses—ever,” they also strangle long-term gains. We need long-term gains, but we need to balance those gains against the potential pain of loss.

Enter diversification. Diversification’s fundamental benefit is reducing portfolio risk (pain) while maintaining portfolio reward. Simple stock/bond diversification is a beautiful example. (I won’t rehash that entire article here, but I recommend you read it.)

In that article, I share data from the S&P 500, the Bloomberg Aggregate Bond index, and a 60% S&P, 40% bond portfolio.

Since 1980, the 100% stock portfolio returned 11.0% per year with an average intra-year drawdown of -14.3%. What would Danny Kahneman say about comparing a $11,000 gain against a $14,300 loss?

The 60/40 portfolio returned 9.9% per year with an average intra-year drawdown of -7.7%. Again, let’s compare a $9900 gain against a $7700 loss.

The perfectly rational investor knows the losses are temporary and would stomach the larger loss from 100% stocks to achieve larger gains. But we’re flawed and monkey-brained. We care too much about losses. For many investors, the 60/40 portfolio is easier to stomach and stick with. While irrational, that’s reality; that’s the world we live in. That’s why Kahneman and Tversky’s work is impactful.

The Stove Can’t Be Untouched

Another behavioral tic resulting from loss aversion is the proverbial “scar tissue” or the perhaps-not-proverbial “PTSD” that can occur after a harrowing investing event.

Take, for example, the GameStop or Enron investors who lost vast sums of their net worth and reacted, “Stocks are a scam. I’m never investing again.” There are more tame examples, too. Someone owning a diversified basket of U.S. stocks would have lost 49% during the Dot Com bubble bursting and 57% during the Great Financial Crisis.

Some investors get burned in one terrible event and then, proverbially, never step foot near a stove or a fire again. They stay out of the market, leaving their dollars on the sidelines. That is not an ideal outcome.

I’d rather see an investor in a boring, tame 40/60 portfolio for their entire investing career than have them start at 100/0, get terribly burned, and then bail to cash for the rest of their lives. While 40/60 is far too conservative for me (and maybe for you), we live in a world where loss aversion is a reality.

RIP Danny

Kahneman and Tversky fundamentally changed psychology, economics, and (specifically for us) how we think about long-term investing. The Best Interest owes them a debt of gratitude!

As you forge on in your personal investing journey, your future losses will sting more than you might think, so you must allocate your dollars accordingly today.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

Excellent review of Kahneman’s work and a very insightful recap of that work that is a valuable read for investors.

Cheers! Thanks for reading.