There’s a famous parable out of Philadelphia about a “financial advisor” named Phil Cannella.

Cannella loved to sell annuities. You’ll know why by the end of this blog post.

Cannella loved annuities so much, he ran sales infomercials on the radio every weekend.

He loved annuities so much he believed they made him a target for assassination. Why? For shining a light on the “atrocities on Wall Street.” He believed (genuinely? insincerely?) that annuities were superior to stocks, bonds, mutual funds, and the like.

Cannella said, “If I get picked off for doing something great nationally, I’m ok with that. Isn’t that how Martin Luther King died? They all died for a cause, and the cause still survives. So I’m not afraid to die.”

- Martin Luther King, Jr.

- Abraham Lincoln.

- And Phil from Philly, who sold too many annuities.

What a peculiar sales tactic. Martyrdom. Perhaps Phil ought to buy some life insurance? I bet he knows a guy…

Rather than decipher Phil’s sales tactics, let’s answer another confusing question. What the heck are annuities?

That’s what we’ll focus on today. We’ll explain annuities in simple terms.

So put on your flak jacket and get ready to cover the basics of annuities.

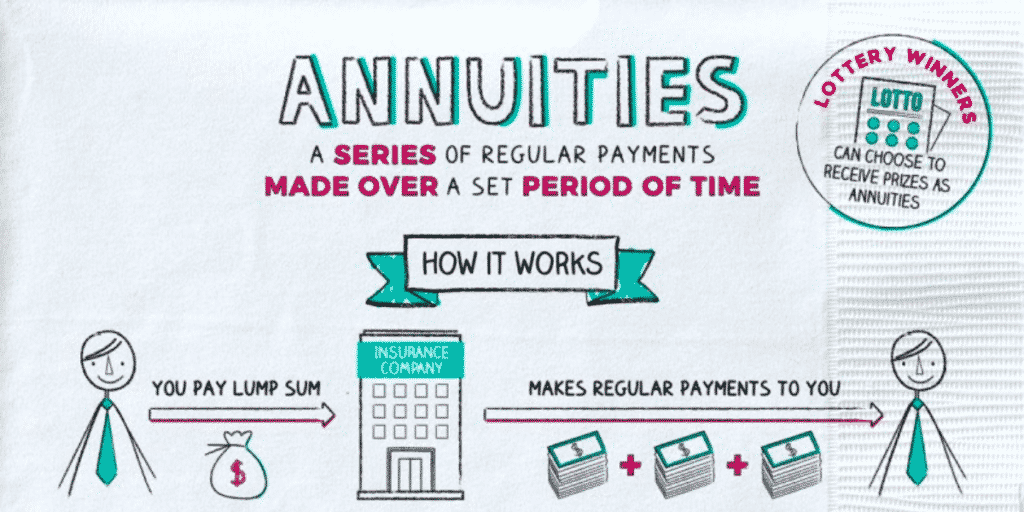

What Are The Basics of An Annuity?

Annuities are contracts between you and an insurance company.

You provide a large sum of money today. The insurance company then promises to make a fixed stream of income payments to you in the future.

The future is unknown. It’s risky. By purchasing an annuity, you’re buying a more certain future.

But at what cost? We’ll cover that later.

How Does An Annuity Work?

Annuities exist on a timeline, and they should be explained through that lens.

At beginning of an annuity, the purchaser (or the “annuitant”) forks over a large amount of cash. Sometimes this occurs through a single lump sum. Other times, through a series of payments. The insurance company might invest this money on your behalf to (hopefully) grow it. The growth is tax-deferred. The period of initial funding and growth is called the “accumulation phase.”

Notably, annuity salespeople and insurance companies collect their commissions and payments upfront. That’s the nice thing (for them) about collecting a lump sum of your money. They immediately receive their reward.

Could this incentive lead to annuities being oversold? Ask Phil “Martin Luther King Jr.” Cannella. Better yet, ask Charlie Munger:

“Show me the incentive and I will show you the outcome.”

Charlie Munger

After the accumulation phase, the payments begin. This is called “annuitization,” or the “annuitization phase.”

Some annuities are immediate, with no significant accumulation phase. They go straight from lump sum into annuitized payments. Other annuities are deferred, with a time period between initial accumulation and later annuitization.

Annuities are frequently associated with “infinite payments.” In other words, they provide the annuitant with fixed income for the rest of their lives. But annuities can be structured with limited annuitization periods, including periods that continue paying out after the annuitant’s death. Annuity contracts can also be written to continue paying “survivorship benefits” to a spouse or beneficiary after the annuitant’s death.

How Are Annuities Taxed?

Annuity taxation is famously complex. There is no one-size-fits-all answer.

The best way to answer annuity taxation questions? Consult a financial and/or taxation professional, and preferably not the one who sold you the annuity. Remember: the annuity salesperson’s incentives exist at the time of sale of the annuity, not during the annuitization phase. And the taxes are all paid during annuitization.

Here are some simple bullet points on annuity taxation. But be careful, because most of the simple rules have “gotchas” and exceptions:

- Growth during the accumulation phase is tax-free until distributed (e.g. tax-deferred)

- Distributions are taxed as income, not capital gains (even if the growth came from assets that normally fall under capital gains tax e.g. stocks).

- Taxation is dependent on where/how the annuity is held. e.g. annuities in a Traditional IRA or 403(b) can be funded with pre-tax dollars.

- Annuitization distribution taxes are prorated. If a $100,000 annuity grows to $200,000, then half is principal and half is growth. Thus, 50% of the annuity payout will be subject to income tax.

- Withdrawal distribution taxes are subject to last in, first out (LIFO) rules. If a $100,000 annuity grows to $200,000, then the first $100,000 of withdrawals are taxed as income.

- Note: annuitization distributions are the planned, regular outflows from an annuity, whereas withdrawals are unplanned or lump sum in nature.

- And there are still many “gotcha” situations that are beyond the scope of this post. Consult a pro.

Example of An Annuity

Suppose you buy a $100,000 immediate annuity. You begin collecting $500 per month, or $6,000 per year. This annuity has a 6% payout rate (6,000 / 100,000 = 6%)

“So, I’m getting a 6% guaranteed rate of return forever? Not bad!!!”

No, no, no. The payout rate is NOT the same as a rate of return. This is a vital point.

Why? Because the payout is, in essence, paying you back your own principal. Whereas a true rate of return represents capital returned in excess of your initial principal.

To understand the true rate of return of an annuity, we must know how many payments someone will receive. Or in other words, how long they’ll live. Naturally, this is an impossible task. We can’t predict the future.

But for the sake of this article, let’s examine the 6% payout annuity over three potential timelines: if the annuitant lives for 15 years, for 25 years, and for 35 years. The following results can be easily replicated using a spreadsheet.

If the annuitant collects for 15 years, the annuity will have an internal rate of return of (-1.29%). That’s worse than a bank account. That’s worse than sticking money under the mattress.

You didn’t even get your initial principal back! Want to change that? It’ll cost you a fee.

If the annuitant collects for 25 years, the annuity will have an internal rate of return of +3.34%. For comparison, the worst 25-year period in stock market history returned 3.78% per year. The median 25-year period returned 9.08% per year. Results for the more conservative 60/40 stock/bond portfolio are 5.04% per year and 9.00% per year, respectively.

If the annuitant collects for 35 years, the annuity will have an IRR of 4.86%. The worst 35-year period in stock market history returned 5.34% per year, with the median 35-year period returning 10.30% per year. For the 60/40 portfolio, 6.72% and 9.15%, respectively.

For these reasons, annuities frequently do not make sense. This is especially true for young individuals with long investing timelines ahead of them. They can withstand the volatility of risk assets (stocks, bonds, etc.) and do not need the volatility dampening provided by an annuity.

What’s the Surrender Period?

Annuities are infamously illiquid. You cannot simply withdraw your money, as you might by selling stocks. Not only might you get unfavorable tax treatment by withdrawing money from an annuity, but you might even pay a fee.

The “surrender period” is the time at the beginning of an annuity during which you have to pay a “surrender charge” to withdraw. These charges are typically less than 10% and decrease over time.

The existence of surrender charges highlight two important points:

- Ensure you fully understand your annuity before you purchase it

- Never contribute money to an annuity that you could conceivably need before the surrender period ends.

If you buy an annuity, you should have a Winston Churchill mindset: never surrender.

Fixed vs. Variable

Fixed annuities are safe and dependable. They come with guaranteed future annuity payments. They can’t go up or down in value.

But variable annuities split the initial accumulation dollars into two buckets: one fixed, one variable. The sizes of these two buckets depend on the specific annuity. The fixed bucket acts like a fixed annuity. But the variable bucket is typically invested in mutual funds and can grow or shrink over time.

Criticisms

Most annuities are overpriced. They carry huge commissions, which you pay upfront.

They are hard to understand, even for financial professionals. I can easily explain any mutual fund or ETF simply by Googling it. I cannot do the same for annuities.

And annuities are illiquid. They cannot be easily dissolved or sold, less you pay a steep surrender fee.

Do annuities have a place in the financial landscape? Yes, albeit a very small one.

But are the fees and commissions structured such that annuities are grossly oversold? Ab-so-lutely.

Annuities vs. Life Insurance

Annuities and life insurance are similar and often confused. But they have opposite payment structures and protect against different downside risks.

With life insurance, the purchaser pays many premium payments over a long period of time. At death, their beneficiary receives a death benefit. Many payments in, lump sum out, protecting against unexpected death.

With an annuity, the purchaser makes a lump sum payment upfront, then receives multiple payments over a long period of time. Lump-sum in, many payments out, protecting against unexpected longevity.

What Is a Non-Qualified Annuity?

Many annuities are bought within tax-advantaged retirement accounts, like 401(k) and 403(b) accounts. These are considered qualified annuities. Both the contributions and the earnings are subject to tax at distribution since the dollars were invested on a pre-tax basis.

Annuities purchased with after-tax dollars are considered non-qualified annuities. Only the earnings from a non-qualified annuity are subject to tax at the time of withdrawal. The contributions are not taxed, as they’ve already been taxed once.

My Opinion on Annuities

Three significant themes jump to mind when I think about annuities.

The first theme is “risk and reward.” Purchasing an annuity decreases your future uncertainty and risk. But you pay a price in diminished future rewards (recall our example before as compared to long-term stock market performance). Understanding that fundamental risk/reward trade is the first step in determining if an annuity is right for you.

The second theme is bad incentives. Insurance salespeople are grossly incentivized to sell annuities. Thus, most annuities are sold to people who do not need them. Some salespeople are ignorant rubes. Others are cunning sharks. And almost none of them are truly acting in their customers’ best interests. Don’t get fooled by a rube or a shark. Do your due diligence.

And the third theme involves pie. Your dollars determine the size of your pie. And using traditional risk assets (stocks, bonds, alternatives, etc), you can grow your pie. But when other people get involved, they want some of your pie. Naturally, this leaves less pie for you.

The question, then, is, “Are these other people growing your pie faster than you could on your own? Are they keeping your pie safe? What value are they providing?”

We’ve covered answers to all these questions.

Annuities take ownership of your pie and immediately remove a large slice (the commission). They limit your ability to eat your own pie (illiquidity). It takes them decades to grow your pie (rate of return vs. payout rate). And even once the pie has grown, it’s smaller than what you could’ve done on your own.

Annuities are a bit like opioids. They are sold as painkillers to soften a harsh world. They manufacture a warm, fuzzy feeling. But depending on who you ask, the downsides outweigh the benefits.

Are opioids a bad metaphor? Maybe. But certainly not as bad as, “I’m the Martin Luther King Jr. of selling annuities,” right?!

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

Great informative post on Annuities. I think your metaphor of opioids is very good and the sales are being pushed on people like a drug dealer. They want to get you hooked and locked in. While I would never buy an annuity personally I believe there are a few cases where they are useful.

While I wholeheartedly agree there are many “bad annuities” (i.e. variable, EIAs, etc.) that are being sold by sleazy bank “advisors,” I think you overlooked the benefits of an ordinary deferred/immediate income annuity (i.e. “private pension”) and how it can provide stable monthly cash flow for retirees.

I think about my mom. She was a 35+ year medical professional and does not understand investing. All she knew was to earn, save, and manage cash flow (budget). Now that she is retired and unable/unwilling to earn employment income she wanted to have a predictable monthly cash flow in her retirement that is not dependent on various market outcomes.

So, I asked what she wanted in monthly income that would enable her to enjoy her hard-earned wealth. We took that number, subtracted her Social Security amount, and identified the income gap. We then contacted several highly-rated carriers for quotes on what they would need upfront to fill her monthly income gap. We reviewed each of the quotes and implemented.

Now she has two sources of “mailbox money” (social security and income annuity) that enable her to consistently budget and enjoy retirement regardless of what the market does. The rest of her assets are invested in a diversified portfolio consistent with her risk tolerance that can be used for discretionary expenses, legacy, other needs, etc.

Did the insurance company/rep receive a commission on her income annuity? I’m sure he did, but the value my mom is getting from the annuity enables her to budget, eliminates longevity risk, and protects her from market volatility, especially during a time where she is unable/unwilling to work.

When you ask my mom to describe her portfolio she will say her SS and income annuity are her “base pay” (predictable) designed to pay for her needs and her investments are her “bonus pay” (unpredictable) designed to pay for her wants. Sound familiar?!

If I had read this blog post prior to helping my mom I would have likely steered her away from “all annuities” convincing her they are “all bad.” Those simple income annuities that do NOT have surrender periods, underlying variable investments, complex cap rates, and other expensive features are worth a honest and hard consideration.

My mom does not want to “hit home runs” (i.e. investment performance) with her portfolio anymore, she wants to hit “singles” and “doubles” while enjoying her retirement.

Love reading your stuff, but wanted to chime in on how I helped my mom with what I considered a “good annuity” that is simple to explain. Perhaps you can consider this angle in future content.

Hey Joe! Thanks for the thoughful message. I can appreciate everything you’ve said.

Yes – the simple, fixed, immediate annuities you write about are as good as annuities get.

It’s funny though. Those annuities are ~bought~, just as you did with your mom. They are not ~sold~. The reason, of course, is that the commission is so low that the agents/advisors don’t feel compensated to sell them. I’m making a different argument though. Let’s get back to your point.

It sounds like this annuity was a good fit for you mom. That’s extremely important! I don’t discount that fact.

Playing devil’s advocate, I would still point out some mathematically reasons I’d avoid all annuities – even the one like your mom has. Namely, the issue is the risk/return profile over time.

If the annuitant dies early, the annuity is either guaranteed to be a loss or, at best, a return of principal.

If the annuitant dies late in life (e.g. 25+ years after buying the annuity), the best IRR of annuities I’ve ever seen is ~6-7%. If I have to wait 25 years for my ~7% annualized return to pan out, I’d rather invest elsewhere.

I have a podcast episode coming out in August where I dive into this rationale in detail. I’ll share it with you when it publishes.

Best,

Jesse