This article will explain the Big Short and the 2008 subprime mortgage collapse in simple terms.

This post is a little longer than usual–maybe give yourself 20 minutes to sift through it. But I promise you’ll leave feeling like you can tranche (that’s a verb, right?!) the whole financial system!

Key Players

First, I want to introduce the players in the financial crisis, as they might not make sense at first blush. One of the worst parts about the financial industry is how they use deliberately obtuse language to explain relatively simple ideas. Their financial acronyms are hard to keep track of. In order to explain the Big Short, these players–and their roles–are key.

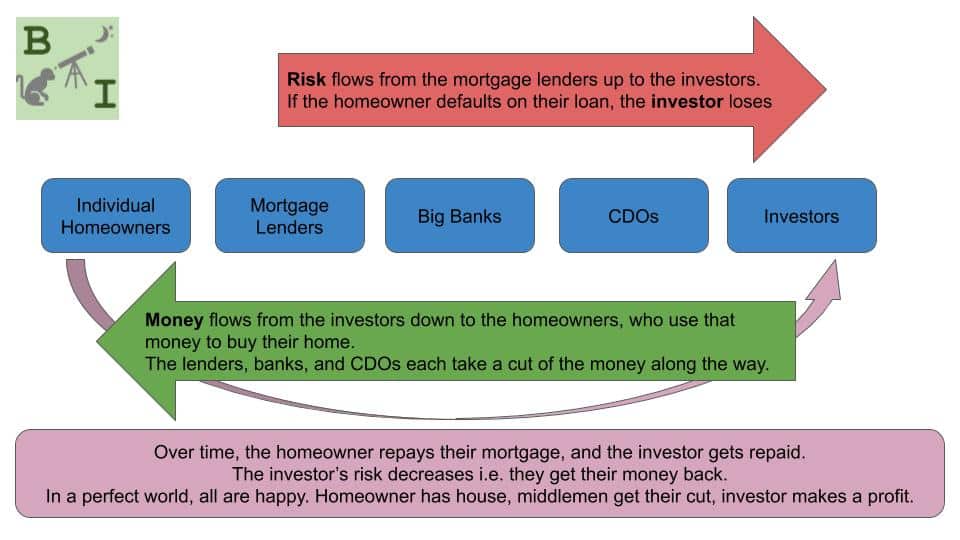

Individuals, a.k.a. regular people who take out mortgages to buy houses; for example, you and me!

Mortgage lenders, like a local bank or a mortgage lending specialty shop, who give out mortgages to individuals. Either way, they’re probably local people that the individual home-buyer would meet in person.

Big banks, such as Goldman Sachs and Morgan Stanley, who buy lots of mortgages from lenders. After this transaction, the homeowner would owe money to the big bank instead of the lender.

Collateralized debt obligations (CDOs)—deep breath!—who take mortgages from big banks and bundle them all together into a bond (see below). And just like before, this step means that the home-buyer now owes money to the CDO. Why is this done?! I’ll explain, I promise.

Ratings agencies, whose job is to determine the risk of a CDO—is it filled with safe mortgages, or risky mortgages?

Investors, who buy part of a CDO and get repaid as the individual homeowners start paying back their mortgage.

Feel lost already? I’m going to be a good jungle guide and get you through this. Stick with me.

Quick definition: Bonds

A bond can be thought of as a loan. When you buy a bond, you are loaning your money. The issuer of the bond is borrowing your money. In exchange for borrowing your money, the issuer promises to pay you back, plus interest, in a certain amount of time. Sometimes, the borrower cannot pay the investor back, and the bond defaults, or fails. Defaults are not good for the investor.

The CDO—which is a bond—could hold thousands of mortgages in it. It’s a mortgage-backed bond, and therefore a type of mortgage-backed security. If you bought 1% of a CDO, you were loaning money equivalent to 1% of all the mortgage principal, with the hope of collecting 1% of the principal plus interest as the mortgages got repaid.

There’s one more key player, but I’ll wait to introduce it. First…

The Whys, Explained

Why does an individual take out a mortgage? Because they want a home. Can you blame them?! A healthy housing market involves people buying and selling houses.

How about the lender; why do they lend? It used to be so they would slowly make interest money as the mortgage got repaid. But nowadays, the lender takes a fee (from the homeowner) for creating (or originating) the mortgage, and then immediately sells to mortgage to…

A big bank. Why do they buy mortgages from lenders? Starting in the 1970s, Wall St. started buying up groups of loans, tying them all together into one bond—the CDO—and selling slices of that collection to investors. When people buy and sell those slices, the big banks get a cut of the action—a commission.

Why would an investor want a slice of a mortgage CDO? Because, like any other investment, the big banks promised that the investor would make their money back plus interest once the homeowners began repaying their mortgages.

You can almost trace the flow of money and risk from player to player.

At the end of the day, the investor needs to get repaid, and that money comes from homeowners.

Enjoying this article? Subscribe below to get new articles emailed straight to your inbox

CDOs are empty buckets

Homeowners and mortgage lenders are easy to understand. But a big question mark swirls around Wall Street’s CDOs.

I like to think of the CDO as a football field full of empty buckets—one bucket per mortgage. As an investor, you don’t purchase one single bucket, or one mortgage. Instead, you purchase a thin horizontal slice across all the buckets—say, a half-inch slice right around the 1-gallon mark.

As the mortgages are repaid, it starts raining. The repayments—or rain—from Mortgage A doesn’t go solely into Bucket A, but rather is distributed across all the buckets, and all the buckets slowly get re-filled.

As long as your horizontal slice of the bucket is eventually surpassed, you get your money back plus interest. You don’t need every mortgage to be repaid. You just need enough mortgages to get to your slice.

It makes sense, then, that the tippy top of the bucket—which gets filled up last—is the highest risk. If too many of the mortgages in the CDO fail and aren’t repaid, then the tippy top of the bucket will never get filled up, and those investors won’t get their money back.

These horizontal slices are called tranches, which might sound familiar if you’ve read the book or watched the movie.

So far, there’s nothing too wrong about this practice. It’s simply moving the risk from the mortgage lender to other investors. Sure, the middle-men (banks, lenders, CDOs) are all taking a cut out of all the buy and sell transactions. But that’s no different than buying lettuce at grocery store prices vs. buying straight from the farmer. Middle-men take a cut. It happens.

But now, our final player enters the stage…

Credit Default Swaps: The Lynchpin of the Big Short

Screw you, Wall Street nomenclature! A credit default swap sounds complicated, but it’s just insurance. Very simple, but they have a key role to explain the Big Short.

Investors thought, “Well, since I’m buying this risky tranche of a CDO, I might want to hedge my bets a bit and buy insurance in case it fails.” That’s what a credit default swap did. It’s insurance against something failing. But, there is a vital difference between a credit default swap and normal insurance.

I can’t buy an insurance policy on your house, on your car, or on your life. Only you can buy those policies. But, I could buy insurance on a CDO mortgage bond, even if I didn’t own that bond!

Not only that, but I could buy billions of dollars of insurance on a CDO that only contained millions of dollars of mortgages.

It’s like taking out a $1 million auto policy on a Honda Civic. No insurance company would allow you to do this, but it was happening all over Wall Street before 2008. This scenario essentially is “the big short” (see below)—making huge insurance bets that CDOs will fail—and many of the big banks were on the wrong side of this bet!

Credit default swaps involved the largest amounts of money in the subprime mortgage crisis. This is where the big Wall Street bets were taking place.

Quick definition: Short

A short is a bet that something will fail, get worse, or go down. When most people invest, they buy long (“I want this stock price to go up!”). A short is the opposite of that.

Certain individuals—like main characters Steve Eisman (aka Mark Baum in the movie, played by Steve Carrell) and Michael Burry (played by Christian Bale) in the 2015 Oscar-nominated film The Big Short—realized that tons of mortgages were being made to people who would never be able to pay them back.

If enough mortgages failed, then tranches of CDOs start to fail—no mortgage repayment means no rain, and no rain means the buckets stay empty. If CDOs fail, then the credit default swap insurance gets paid out. So what to do? Buy credit default swaps! That’s the quick and dirty way to explain the Big Short.

Why buy Dog Shit?

Wait a second. Why did people originally invest in these CDO bonds if they were full of “dog shit mortgages” (direct quote from the book) in the first place? Since The Big Short protagonists knew what was happening, shouldn’t the investors also have realized that the buckets would never get refilled?

For one, the prospectus—a fancy word for “owner’s manual”—of a CDO was very difficult to parse through. It was hard to understand exactly which mortgages were in the CDO. This is a skeevy big bank/CDO practice. And even if you knew which mortgages were in a CDO, it was nearly impossible to realize that many of those mortgages were made fraudulently.

The mortgage lenders were knowingly creating bad mortgages. They were giving loans to people with no hopes of repaying them. Why? Because the lenders knew they could immediately sell that mortgage—that risk—to a big bank, which would then securitize the mortgage into a CDO, and then sell that CDO to investors. Any risk that the lender took by creating a bad mortgage was quickly transferred to the investor.

So…because you can’t decipher the prospectus to tell which mortgages are in a CDO, it was easier to rely on the CDO’s rating than to evaluate each of the underlying mortgages. It’s the same reason why you don’t have to understand how engines work when you buy a car; you just look at Car & Driver or Consumer Reports for their opinions, their ratings.

The Ratings Agencies

Investors often relied on ratings to determine which bonds to buy. The two most well-known ratings agencies from 2008 were Moody’s and Standard & Poor’s (heard of the S&P 500?). The ratings agency’s job was to look at a CDO that a big bank created, understand the underlying assets (in this case, the mortgages), and give the CDO a rating to determine how safe it was. A good rating is “AAA”—so nice, it got ‘A’ thrice.

So, were the ratings agencies doing their jobs? No! There are a few explanations for this:

- Even they—the experts in charge of grading the bonds—didn’t understand what was going on inside a CDO. The owner’s manual descriptions (prospectuses) were too complicated. In fact, ratings agencies often relied on big banks to teach seminars about how to rate CDOs, which is like a teacher learning how to grade tests from Timmy, who still pees his pants. Timmy just wants an A.

- Ratings agencies are profit-driven companies. When they give a rating, they charge a fee. But if the agency hands out too many bad grades, then their customers—the big banks—will take their requests elsewhere in hopes of higher grades. The ratings agencies weren’t objective, but instead were biased by their need for profits.

- Remember those fraudulent mortgages that the lenders were making? Unless you did some boots-on-the-ground research, it was tough to uncover this fact. It’s hard to blame the ratings agencies for not catching this.

Who’s to blame?

Everyone? Let’s play devil’s advocate…

- Individuals: some people point the finger at homeowners, saying, “You should know better than to buy a $1 million house on a teacher’s salary.” I find this hard to swallow. These people, surrounded by the American home-ownership dream, were sold the idea that they would be fine. The mortgage lender had no incentive to sell a good mortgage, they only had an incentive to sell a mortgage. So, it’s hard for me to put too much blame on the homeowners.

- Mortgage lenders: someone knew. I’m not saying that all the mortgage lenders were fully aware of the implications of their actions, but some people knew that fraudulent loans were being made, and chose to ignore that fact. For example, check out whistleblower Eileen Foster.

- Big banks: Yes sir! There’s certainly blame here. Rather than get into all of the various money-grubbing, I want to call out one specific anecdote. Back in 2010, Goldman Sachs CEO Lloyd Blankfein testified in front of Congress. Here it is:

To explain further, there are two things going on here.

First, Goldman Sachs bankers were selling CDOs to investors. They wanted to make a commission on the sale.

At the same time, other bankers ALSO AT GOLDMAN SACHS were buying credit default swaps, a.k.a. betting against the same CDOs that the first Goldman Sachs bankers were selling.

This is like selling someone a racehorse with cancer, and then immediately going to the track to bet against that horse. Blankfein’s defense in this video is, “But the horse seller and the bettor weren’t the same people!” And the Congressmen responds, “But they worked for the same stable, and collected the same paychecks!”

So do the big banks deserve blame? You tell me.

Inspecting Goldman Sachs

One reason Goldman Sachs survived 2008 is that they began buying credit default swaps (insurance) just in time before the housing market crashed. They were still on the bad side of some bets, but mostly on the good side. They were net profitable.

Unfortunately for them, the banks that owed Goldman money were going bankrupt from their own debt, and then Goldman never would have been able to collect on their insurance. Goldman would’ve had to payout on their “bad” bets, while not collecting on their “good” bets. In their own words, they were “toast.”

This is significant. Even banks in “good” positions would’ve gone bankrupt, because the people who owed the most money weren’t able to repay all their debts. Imagine a chain; Bank A owes money to Bank B, and B owes money to Bank C. If Bank A fails, then B can’t collect their debt, and B can’t pay C. Bank C made “good” bets, but aren’t able to collect on them, and then they go out of business.

These failures would’ve rippled throughout the world. This explains why the US government felt it necessary to bail-out the banks. That federal money allowed banks in “good” positions to collect their profits and “stop the ripple” from tearing apart the world economy. While CDOs and credit default swap explain the Big Short starting, this ripple of failure is the mechanism that affected the entire world.

Betting more than you have

But if someone made a bad bet—sold bad insurance—why didn’t they have money to cover that bet? It all depends on risk. If you sell a $100 million insurance policy, and you think there’s a 1% chance of paying out that policy, what’s your exposure? It’s the potential loss multiplied by the probability = 1% times $100 million, or $1 million.

These banks sold billions of dollars of insurance under the assumption that there was a 5%, or 3%, or 1% chance of the housing market failing. So they had 20x, or 30x, or 100x less money on hand then they needed to cover these bets.

Turns out, there was a 100% chance that the market would fail…oops!

Blame, expounded

Ratings agencies—they should be unbiased. But they sold themselves off for profit. They invited the wolves—big banks—into their homes to teach them how to grade CDOs. Maybe they should read a blog to explain the Big Short to them. Of course they deserve blame. Here’s another anecdote of terrible judgment from the ratings agencies:

Think back to my analogy of the buckets and the rain. Sometimes, a ratings agency would look at a CDO and say, “You’re never going to fill up these buckets all the way. Those final tranches—the ones that won’t get filled—they’re really risky. So we’re going to give them a bad grade.” There were “Dog Shit” tranches, and Dog Shit gets a bad grade.

But then the CDO managers would go back to their offices and cut off the top of the buckets. And they’d do this for all their CDOs—cutting off all the bucket-top rings from all the different CDO buckets. And then they’d super-glue the bucket-top rings together to create a field full of Frankenstein buckets, officially called a CDO squared. Because the Frankenstein buckets were originally part of other CDOs, the Frankenstein buckets could only start filling up once the original buckets (which now had the tops cut off) were filled. In other words, the CDO managers decided to concentrate all their Dog Shit in one place, and super glue it together.

A reasonable person would look at the Frankenstein Dog Shit field of buckets and say, “That’s turrible, Kenny.”

BUT THE RATINGS AGENCIES GAVE CDO-SQUAREDs HIGH GRADES!!! Oh I’m sorry, was I yelling?!

“It’s diversified,” they would claim, as if Poodle shit mixed with Labrador shit is better than pure Poodle shit.

Again, you tell me. Do the ratings agencies deserve blame?!

Does the government deserve blame?

Yes and no.

For example, part of the Housing and Community Development Act of 1992 mandated that the government mortgage finance firms (Freddie Mac and Fannie Mae) purchase a certain number of sub-prime mortgages.

On its surface, this seems like a good thing: it’s giving money to potential home-buyers who wouldn’t otherwise qualify for a mortgage. It’s providing the American Dream.

But as we’ve already covered today, it does nobody any good to provide a bad mortgage to someone who can’t repay it. That’s what caused this whole calamity. Freddie and Fannie and HUD were pumping money into the machine, helping to enable it. Good intentions, but they weren’t paying attention to the unintended outcomes.

And what about the Securities & Exchange Commission (SEC), the watchdogs of Wall Street. Do they have a role to explain the Big Short? Shouldn’t they have been aware of the Big Banks, the CDOs, the ratings agencies?

Yes, they deserve blame too. They’re supposed to do things like ensure that Big Banks have enough money on hand to cover their risky bets. This is called proper “risk management,” and it was severely lacking. The SEC also had the power to dig into the CDOs and ferret out the fraudulent mortgages that were creating them. Why didn’t they do that?

Perhaps the issue is that the SEC was/is simply too close to Wall Street, similar to the ratings agencies getting advice from the big banks. Watchdogs shouldn’t get treats from those they’re watching. Or maybe it’s that the CDOs and credit default swaps were too hard for the SEC to understand.

Either way, the SEC doesn’t have a good excuse. If you’re in bed with the people you’re regulating, then you’re doing a bad job. If you’re rubber stamping things you don’t understand, then you’re doing a bad job.

Explain the Big Short, shortly

You’re about 2500 words into my “short summary.” But the important things to remember:

- Financial acronyms suck.

- Money flowed from the investors down to the mortgage lenders, and the risk flowed from the mortgage lenders up to the investors. In between, the big banks and CDOs acted as middle men and intermediaries.

- When someone feels like their actions have no risk, or no consequences, they’ll behave poorly (big banks, mortgage lenders)

When someone is given what seems like an amazing deal, they’ll take it (individual home owners). - CDOs are like empty buckets. Mortgage payments are like rain, filling the buckets. Investors buy tranches, or slices, across all the buckets. If mortgages fail, then the buckets might not fill up, and the investors won’t get their money back.

- CDOs are intentionally complex. So complex, that not even the people grading them understood what was going on (ratings agencies).

- Buying insurance on something your do not own is a behavior with potential for abuse (big banks)

- Buying insurance on something for more than it’s worth is a behavior with potential for abuse (big banks). This is where most of the money in the financial crisis switched hands.

And with that, I’d like to announce the opening of the Best Interest CDO. Rather than invest in mortgages, I’ll be investing in race horses. Don’t ask my why, but the current top stallion is named ‘Dog Shit.’ He’ll take Wall Street by storm.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

Well written article that provides good insight. I have a few follow-up questions. Perhaps you could fashion these into a Pt. 2?

1. What did the Gov’t bailout consists of? And what do you think would have happened nationally and internationally if we had not bailed out the big banks? Were the banks obligated to pay back that money?

2. Do these bailouts as well as the lack of jail-time (correct me if I’m wrong) for the guys at the top orchestrating this whole scheme send a message of ‘no consequences’ if this were to happen again?

2. Are some entities like the banks in this case ‘too big to fail’? Another example that comes to mind is the auto bailout under Bush?

3. A conversation I’m hearing more and more in this country is ‘affordable housing’ and ‘livable wage’. Do you feel the possibility of buying a house has become too distant for many people because of an ever shrinking livable wage? What’s a possible solution?

Thanks for the great questions.

1) Loans to banks in trouble so that they could pay their debts. If not, the “ripple” that I describe in the post would have been catastrophic.

2a) The thing that should have been done is: change the underlying structure that allowed this to happen. Changes to legislation, to ways the watchdogs operate, etc. Jail time would certainly help, I think, too…

2b) Yes. And we should work to change the system in which that’s the case.

3) Google “Shiller Index.” It tracks the cost of housing compared to other items and to the economy in general. And the cost of housing is higher NOW then it was before the housing crisis bubble burst. That’s wild. What gives? I’m not sure.

I enjoyed reading this. I do think you left out the government as a key player. Continuing to relax lending standards as late as the early 2000s creates the basis for the “housing always goes up” risk models that ultimately got us to this point.

Secondly, as a former “Main Street” banker, I hate that the gambling jockeys at the New York hedge fund “banks” got lumped into the same category as me loaning money to mom and pop entrepreneurs.

Ultimately the moral hazard in the financial sector hasn’t been corrected. The revenue producing staff of financial firms generate deals. If those deals go bad, it can be years later after compensation is paid and the people who generated the deals are off to another firm, retired, or moved out of the industry. The “clown vs crook” defense is real, it’s easy for someone to say “I didn’t know better at the time”.

There are also multiple layers of people approving these transactions at the firm, which is how it doesn’t move into “individuals being held responsible via jail time”.

One unpopular thing that would help is to pay the regulators more. It’s a stacked deck on talent with the IBs and traditional banks pay at least 3x what the regulatory agencies pay.

Hey Robert.

I’m really glad you enjoyed the post. Thanks a ton for the detailed response. Let me break down your reply into the five paragraphs you wrote, and respond one by one.

Did you see my section “Does the government deserve blame?,” near the bottom of the post? I covered Freddie and Fannie’s relaxed lending standards, which I think is similar to what you pointed out.

Fair enough. I don’t know your exact background. I agree with you that Wall Street “gambling jockeys” created a demand for loans to buy and sell. That demand incentivized other people in the system (e.g. “Main Street” bankers) to create more loans. That said, there is clear evidence that Main Street executives (e.g. Countrywide) knew they were creating fraudulent loans for Mom and Pop, and kept doing it because it was their cash cow. I know there were boots-on-the-ground folks who tried blowing the whistle (Eileen Foster)…it’s too bad their voices weren’t listened too 🙁

Agreed.

Agreed. Diluting the responsibility seemed to dilute the consequences. And that doesn’t seem right. The buck has to stop somewhere.

Agreed. It’s the same in many, many industries. Private pays way more than public, so incentives are often skewed.

Cheers!

Jesse

Pingback: Engineering Principles Applied to Money - The Frugal Engineers

Pingback: Personal Finance Unknowns - The Best Interest - It's what you don't know...

Pingback: Index Fund Bubble: Arguments For and Against - The Best Interest

Pingback: The Biggest Lesson from COVID-19 - The Best Interest

Pingback: Why You Should Pay Off Your Mortgage | Money Life Wax

Pingback: The Strategy for Investing in a Recession - Just Start Investing

Pingback: Ideas for Things to do at Home During a Quarantine | BeThree

Pingback: How to Get Wealthy Investing in a Bear Market - Physician on FIRE

Pingback: The Best Leadership Quotes and How to Apply Them - Market World

Pingback: The Best Leadership Quotes and How to Apply Them – Finance Market House

Pingback: The Best Leadership Quotes and How to Apply Them | Share Market Pro

Pingback: 12 of the Best Leadership Quotes - and How They Apply to You! - Partners in Fire

Pingback: Leadership Quotes: The Best & How to Apply Them | Money Life Wax

Pingback: The Best Leadership Quotes and How to Apply Them - Money Saved Is Money Earned

Pingback: The Best Leadership Quotes and How to Apply Them - The Best Interest

Pingback: The Best Leadership Quotes and How to Apply Them | Wealthy Nickel

Pingback: The Best Leadership Quotes and How to Apply Them - HealthyLifey

Hi,

I am fairly new to economics and my teacher recommended I watch the Big Short to get familiar with the ideas behind the 2008 crash. However, I soon become frustrated that I was unable to understand the economics at play, so I decided to do some reading and see what I could figure out. Having read many explanations full of complex jargon, I stumbled across your very clear, yet detailed, blog. Thank you for making these complicated ideas make a large amount of sense!

I have one question… I’m not sure if I’m missing something here but from what I’ve gathered morgage bonds are backed by property as collateral. Therefore, if investors technically own the mortgage through the bond, why do they lose out if the mortgage is defaulted, as surely the investor would claim possesion of the property? Is it because the investor does not invest in one single morgtage, but rather a ‘tranche’ of mortgages, making it impractical for them to claim ownership of defaulted properties. If so, who would claim possesion of a property if the mortgage was defaulted?

One other quick question: if CDOs contain parts of many mortgages, how are these parts decided (is it that one CDO contains the loan for a set stage of mortgage payments?)

Thank you!

I’m so glad you found the article informational and clear!

On your first question…

Let’s say you own 1% of 100 different mortgages. On average, each house is worth $250K. Therefore, you own $250K in debt.

As the homeowners pay their mortgages, you slowly get your investment back. When someone defaults, they stop paying you. But, like you pointed out, you now have 1% equity in the house itself!

So, will that house still be worth $250K? Is your 1% equity still worth $2500? Well, it depends. How has the housing market changed recently?

In the case of 2008, thousands and thousands of mortgages were being defaulted, which meant a huge supply of homes on the market. When supply goes up, price goes down.

The house isn’t worth $250K anymore. It’s now worth $150K. And your share is only worth $1500.

Now multiply that across all 100 homes that you own 1% of. If the market crashes, so does your investment.

Does that help explain it?

—-

On your second question, I’m not 100% I understood it correctly, so let me know if this helps.

First, the world of CDOs is such a tangled web. Ugh.

One CDO could contain hundreds of different mortgages from all over the country, and that CDO could be “filled” with mortgage payments at all different stages of the mortgage life cycle. The CDO manager(s)–real people–decide what mortgages to put in their CDO, how to price those mortgages’ risk, how to slice it up into tranches, and what prices to sell those tranches at.

Thanks again for reading. Let me know if you have further questions.

-Jesse

Pingback: The Best Leadership Quotes to Inspire and Guide You. | BeThree

Pingback: How to Apply the 12 Best Leadership Quotes to Your Life - My Life, I Guess

My understanding is that the players in this film in your words “bought insurance on a house that they knew was going to burn” . I still don’t understand what determines how much money they received after the mortgages failed? Was the value of the insurance for the full value of the mortgages on each house? Finally, for example Burrys first stop he wanted 100 million dollars worth of cds, I still don’t understand what that 100 million buys him.

Hi Phillip. Great questions.

The credit default swap payout can be thought of as the odds on a bet. Some bets are 1-to-1 odds. Other bets are 1000-to-1 odds. People like Michael Burry bought millions of dollars in swaps (aka bets) that had 10-to-1, 20-to-1, or higher odds. The banks that Burry bought from determine the odds, much like a casino determines the odds on a horse race.

When Burry bought $100 MM in credit default swaps, it’s like placing a $100 MM bet.

That makes sensem thank you.

This is so fantastic! I wish something like this had been around when the film first came out. I rewatched it again yesterday hoping I’d suddenly, magically, understand the ideas involved but there’s still so much I don’t get. You answered most of my questions here, but I still have a few more if you don’t mind?

1. How can the banks repay the insurance/Credit Default Swaps if they’re failing due to bad mortgage debt? In the movie, JP Morgan was firing people because they apparently owed 15 billion, or had 15 billion in exposure. (Side question: what’s “exposure” exactly?) So if they had that level of financial trouble, how can they be expected to uphold their contracts and pay out the guys who shorted? And why did JP Morgan at some point try to buy the swaps that Steve Carell’s team owned? The two young guys working with Brad Pitt’s character eventually sold their swaps for like 80 million to Credit Suisse or something. But why on Earth would another bank buy their swaps at all?? Aren’t they worthless if failing banks can’t pay them what they owe? And in the very end when Steve Carell finally agreed to sell, who the heck is he selling to?!? At that point, the entire world’s economy was collapsing so who is left to buy swaps!??! And who is left to pay out for them!?

2. Why did the guys spend so much time toward the end of the film talking about a fraudulent system? It seemed as if the banks were delaying paying them the money they owed for “losing the bet” until they secured their own position. That’s the conversation Christian Bale’s character has with some guy on the phone and the guy goes, “I don’t know what you want me to say,” implying that he was unable to refute the accusation. However I don’t fully understand the accusation, or why the other two young guys were trying to tell the story to a financial journalist (who refused to print it). What exactly did the banks do that was so fraudulent? Whatever it was doesn’t seem to have prevented the main protagonists from getting paid, just delayed it.

3. Ryan Gosling’s character was only introduced to Steve Carell’s team by accident (Thanks to his “fuckstick assistant,” which was hands-down my favorite line in the movie! ?) and because everyone else he tried to convince to go in with him said no. He said people at his own firm laughed at him. But then in the end he got a bonus from his firm. So whose money was he using for the deal, his own or his firm’s? If his bank didn’t agree to the deal and he had to use Steve’s firm instead, how did he make any money for himself? I didn’t get that whole scene between him and the dude from Succession where he talks about dividing up the ice cream sundae. It was obvious that he was going to get paid somehow but I don’t get how. It seems odd that his firm would reward him for something they didn’t support him doing unless he made a ton of money for the firm by going against them and doing it anyway. But then we’re right back to what’s in it for HIM? Why go through all that just to make money for a firm that didn’t believe in him, in hopes of getting a bonus that’s not guaranteed?

Anyway those were obviously more than a few questions so I get it if you don’t have time to deal with all of them but I’d love to hear from you if you do! Thanks!

Hey yzudak, thanks for the questions. I’m glad you found and enjoyed this article. Let me try to address your questions.

1) In my article, read the section called “Inspecting Goldman Sachs.” The U.S. gov’t had to step in because some banks wouldn’t have been able to payout their bad bets, and then the banks that made “good” bets wouldn’t have collected, and then those “good” betting banks would’ve gone out of business too. This would’ve sent ripples across the global economy far more destructive than what actually occurred.

1b) What’s exposure? Exposure simply describes the level of risk (usually measured in dollars) that an organization takes on. For a simple example, let’s look at a casino that takes a $1 million dollar bet on a horse with 20:1 odds. The casino has taken on $20 million in exposure—that’s what they’d have to pay if that particular horse wins. But since the odds are 20:1, the casino is assuming that the horse only has a 5% chance of winning.

1c) Morgan Stanley tried to purchase Steve Carrell’s swaps because Morgan Stanley began to realize that the swaps were actually good bets.

1d) Who was Steve Carrell selling to at the end? I’m not sure. But whoever it was, they were convinced that they could eventually collect on those swaps at full value. They were offering Carrell a discounted rate (e.g. 30 cents on the dollar). Carrell wanted to hold out, convinced that someone would eventually pay his firm a higher rate (e.g. 90 cents on the dollar).

1e) Who is left to pay them out? Someone who likely made good bets themselves, or someone who didn’t have much exposure (oooohh!!) into the real estate bubble.

2) This is an awesome question. It’s easiest to answer via analogy. Let’s say you and I make a bet on an NBA game. I think the Lakers will win, but you think the Lakers will lose. As part of our bet, we agree to make assessments throughout the game. If we assess that the Lakers are in a winning position, you’ll have to give me part of the money that we bet. Similarly, if the Lakers are in a losing position, I have to give you part of the money that we bet. It’s a way of saying, “We agree that the bet appears to be moving in a certain direction, and therefore we recognize that one of us is more likely to be the winner.”

So let’s fast forward to half time of the game. The Lakers are down by 30 points. Clearly, they are losing. But I say, “You know…I still think they have a great chance of winning. Sorry. I’m just not prepared to say that you’re more likely to win the bet.”

You’d probably say, “WTF?!?! How can you possibly believe that the Lakers are more likely to win than lose?!?!” And you’d be right.

In the Big Short, the banks who made bad bets were supposed to be making similar assessments. They were supposed to say, “Gosh, the housing market isn’t looking good. We need to account for the fact that our bets now look like losing bets.”

But they refused to do. They wouldn’t admit they made losing bets, because they’d have to part with their money earlier than they wanted to, or earlier than they were ready for.

BUT WAIT! IT GETS WORSE! Some banks refused to admit they made losing bets UNTIL they went out and bought enough swaps to actually give them a positive position. This is what occurs in the Michael Burry phone call that you allude to. His banker calls him and says, “Hey Michael, we finally decided to mark our bets appropriately, we’ll be sending you some money because we admit that we’re losing that bet.”

And Burry realizes, “You’re only admitting that it’s a losing bet because you went out and bought enough of the OTHER SIDE of that bet to secure a winning position. Admitting that it’s a bad bet is now favorable to you, because you’re admitting that all your new bets are GOOD bets.”

The banks lied. That’s fraud.

3) Vennett was a salesman. And like most salesman, he gets a commission. I believe all the money that Vennett earned was commission. And since he was selling a product that he felt certain would pay BIG, he charged a high commission on his sales.

I’ll try and answer 1 and 2.

They had no intention of paying it back because they didn’t realize it was happening until it was to late.

I think they spent so much time talking about it for movie purposes.

Hey Phil, what’s up? Thanks for chiming in. Yeah, you might be onto something there. I gave some answers too, but yours are cleaner haha.

Thank you so much! This clears things up A LOT, especially the basketball analogy, because frankly I didn’t fully understand how premiums worked either. Much appreciated!!!

Excellent! You’re totally welcome. Thanks for stopping by.

Pingback: Stupid Doctor Tricks: Physicians' Biggest Financial Mistakes - Physician on FIRE

Pingback: The Best Financial Advice of 2020 - Building Self-Reliance

Pingback: 35 Easy Ways to Generate Passive Income in 2020 - Mobile Witch

Pingback: 35 Easy Ways to Generate Passive Income in 2020 | Financial Health Today

Pingback: 35 Easy Ways to Generate Passive Income in 2020 - Savology

Pingback: 35 Easy Ways to Generate Passive Income in 2020

Pingback: 35 Easy Ways to Generate Passive Income in 2020 - The FRUGAL TOURIST

Pingback: 35 Easy Ways to Generate Passive Income in 2020

Pingback: 35 Easy Ways to Generate Passive Income in 2020 - Bella Wanana

Pingback: The Best Leadership Quotes and How to Apply Them - Debt-Free Doctor

Pingback: 35 Easy Ways to Generate Passive Income – Arrest Your Debt

Pingback: 35 Easy Ways to Generate Passive Income – Vincent Bermudez

Pingback: 35 Easy Ways to Generate Passive Income – Unique Balistreri

Pingback: 35 Easy Ways to Generate Passive Income - The Female Professional

Pingback: 35 Easy Ways to Generate Passive Income in 2020 - Money Saved Is Money Earned

Pingback: 35 Easy Ways to Generate Passive Income - Partners in Fire

Pingback: Money habits doctors should make in 2021 – Vts-Finance

Hello,

It is a great article! Thanks for this.

I wanted to know the mechanics of the short. How did Michael Burry actually short this? Can you explain the entire process step-by-step?

Hi Rohit. Thanks for reading. Terrific question!

The answer lies in the section titled “Credit Default Swaps: The Lynchpin of the Big Short.” Start there and read for a few sections.

Michael Burry purchase credit default swaps which act like insurance policies against the mortgage-backed securities.

If the mortgage-backed securities defaulted–that is, if too many homeowners failed to repay their loans–then Burry would get a massive payment through the credit default swap.

Thus, Burry held a “short” position on the housing market.

Jesse – just wanted to say…The Best Interest has changed my life. I’ve incorporated so many of your lessons into my finances, and it’s turned my life around these past 24 months. Thank you for everything.

Thanks Mayur! I appreciate you reading 🙂

Very Informative! Sometimes financial acronyms become very difficult to understand but you have done well research and mentioned everything. Thank you for sharing.

Thanks Mohit!

hello,

thanks for a very detailed article. I have been looking around for hours to understand the movie “The Big Short”. I am just having hard time to understand what were the external environmental factors that caused the market crash. I understand that some of the factors were, competition factors, economics and legal factors. So how exactly we can connect the external factors to the market crash?