Play along with me today.

If you start early, you have six decades from your first investment until your dying breath. Your 20s to your 80s.

What if we knew how those six decades would play out? What if we knew that:

- Decade A would return 16% per year. Nice!

- Decade B would return 12% per year.

- Decade C = 8% per year.

- Decade D = 4% per year.

- Decade E = 0% per year.

- Decade F = -4% per year.

But for the sake of this fun exercise, we don’t know the order of those decades. Which decade will happen first? Last? In between? We don’t know.

But if you got to choose, how would you want to sequence your decades?

Would you want the best years early on, to kickstart your returns? Would you prefer to spread the returns out over time?

The market itself gets to the same spot, regardless of the sequence. The associative property of math ensures that. 8*6*3 = 6*3*8 = 3*8*6.

But your portfolio is drastically affected by the sequence of returns. You read that right. The order of returns affects how much money you’ll end up with.

Why?

Because you’re buying investments in your early years. Only buying. And you’d prefer to buy low.

And because you’re selling investments in your latter years. Only selling. You’d prefer to sell high.

The order of market returns will affect how good of a deal you get when buying and selling.

A Simple Example

Here’s a simple example.

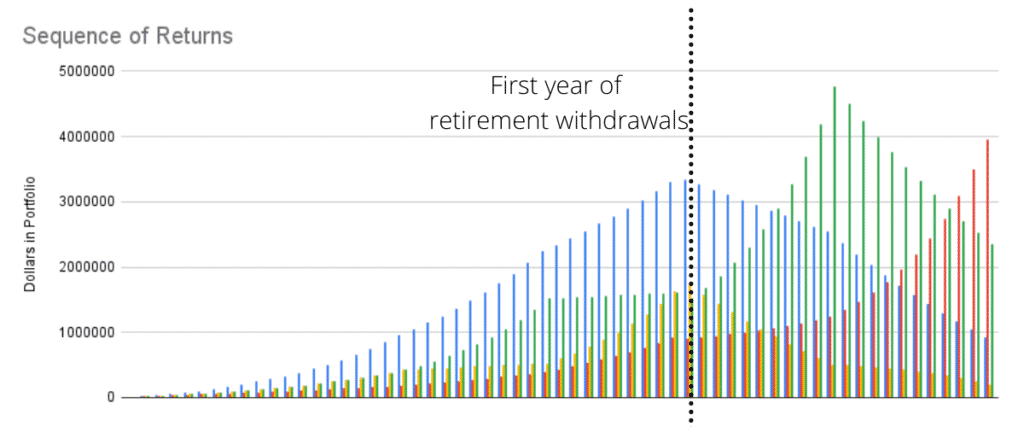

Four hypothetical investors save $10,000 per year for 40 years and then spend $80,000 per year for 20 years in retirement. Save, retire, spend. I’ll show these four investors below, each with their own color.

The blue investor sees the best decades first, worst last. Her order is A, B, C, D, E, F.

The red investor is the opposite. Worst first, best last. His order is F, E, D, C, B, A

The yellow and green investors see a “realistic” mix.

Yellow sees D, C, E, B, F, A.

Green sees D, C, B, E, A, F.

All four investors hit their 80th birthday with money in their portfolio. That’s good. But the red investor has almost $4 million, compared to the yellow investor’s $200K. That’s a big difference.

Look at how similar Yellow and Green’s sequences are, but how different their final portfolios are! Even a small difference in sequence can lead to a big difference in outcome.

Sequences of returns matter. These four investors saw the same 6 decades, but in different orders. And their final portfolio size varied considerably.

What’s the Point? Market Returns Aren’t Random…

Of course, market returns aren’t predictable by decade, nor random in their order.

Market returns happen for real-world reasons. And they ebb and flow. They exhibit both momentum and reversion to the mean. That’s a fancy way of saying, “We have good decades, we have bad decades, but markets have a tendency of ‘averaging out.'”

None of these four investors’ returns are completely realistic. But they highlight important ideas.

Preventing a “Yellow Investor” Fate?

How do ensure we don’t run out of money (like the yellow investor almost does)?

I know what we can’t do. We can’t control the markets. We can’t ask for more than we’re given.

But we can control our exposure to the markets. We can control our asset allocation. We can control how much of our money is exposed to volatile stocks. And to calmer bonds, to dead calm cash, to alternatives, and to real estate. Etc.

That is the essence of portfolio construction and portfolio management. You can’t control the markets. You can control your exposure.

If you’re growing your investments with decades ahead of you, you can pursue high risk and high growth. But as you glide into retirement, your asset allocation should ‘risk down,’ ideally becoming less exposed to sequence of returns risks.

Another important takeaway is that bad markets are good for buyers.

We’ve seen a volatile 2022 in the markets, and some of my peers are reacting with fear. Why?!

If you’re young and buying and growing, don’t feel bad when the market is down. I realize that it’s not fun to watch your accounts decrease. But you’re not investing for fun. You’re investing to build wealth! And that wealth-building benefits from lower purchase prices.

Bad markets are good for buyers.

Summary

The market’s returns aren’t promised. The sequence of returns might not work in your favor. But you can still be a successful investor.

Start early, stay steady, rebalance, and re-allocate. It’s that simple.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!