Back in September 2019, Michael Burry predicted an index fund bubble. Since I invest in index funds and write about them with relish, I was intrigued. But I quickly moved on.

Then in February 2020, another headline caught my eye. It was an episode of Odd Lots podcast titled, “Why Passive Investing Might Be Distorting the Market.” I immediately listened to the episode, featuring investor and fund manager Mike Green. And then I listened again. Considering a lot of my net worth is currently tied up in index funds, I want to understand why some people think index funds are fools’ gold.

So today, I’m going to play devil’s advocate and talk about both sides of the conversation. Is there an index fund bubble? A market crash around the corner? Or is passive investing still the winning strategy it’s always been?

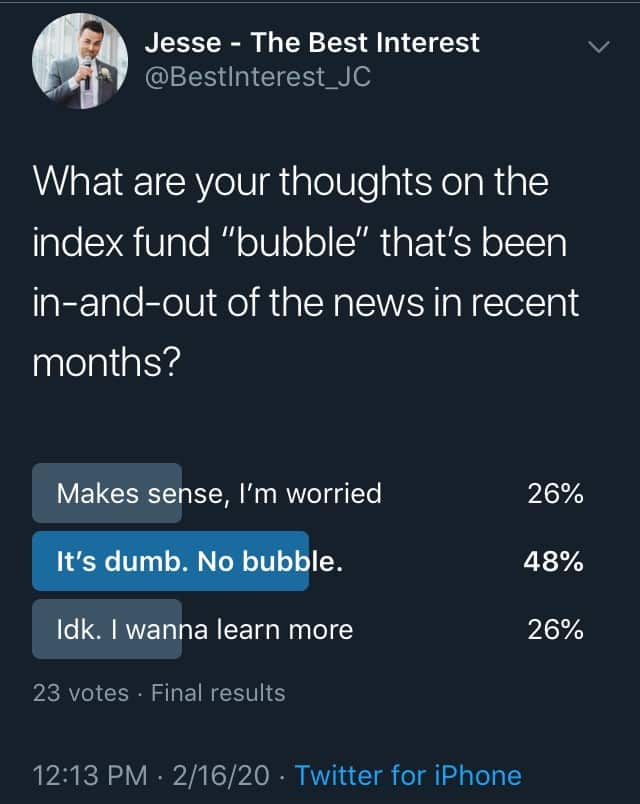

What does FinTwit think?

I ran a quick unofficial survey on Twitter, and here’s how the votes shook down:

23 votes—sounds like an election poll. Still, there’s a fair mix of opinions and the jury is still out. While “no index fund bubble” certainly is the predominant thought, there are plenty of curious and contrarian views. I think examining the different view points is worthwhile.

Below, you’ll find compelling arguments from investors Mike Green and Michael Burry, who both say there is a bubble. Then I’ll follow up with comments from financial analyst Ben Carlson and portfolio manager Ben Felix, both of whom see no bubble . It’s #TeamMike vs. #TeamBen. I’ll also pull some soundbites from Raoul Pal, a former hedge fund manager who now produces financial videos with a silky British accent. And then I’ll add in my own thoughts at the end.

Quick reminder: what’s an index fund?

An index fund owns a wide assortment of assets (e.g. stocks), and owns those assets in proportion to their market share. Uh…that’s a lot of FinSpeak. Let’s break it down.

For an example, let’s look at an S&P 500 index fund. An S&P 500 index fund would own all of the stocks in the S&P 500. Since Apple and Microsoft each make up about 5% of the S&P 500, this index fund would be comprised of about 5% Apple and 5% Microsoft. But Chipotle would only compose about 0.08% of the index, because it’s 0.08% of the S&P. In this way, the index fund is benchmarked to the S&P, like a shadow that follows all of the body’s movements.

Similarly, a “total stock market fund” would own every stock in the market. There are tons of options in the index fund world.

Related articles talking about indexing:

Let’s get into the arguments that claim indexing is now in a bubble.

Part I – Bubble! – “The tail is now wagging the dog”

One of Mike Green’s first points on Odd Lots is this: the original idea behind indexing is that active traders and actively managed funds will dictate how the market behaves, and that a small number of passive investors (e.g. index funds) can simply go along for the ride. The large majority active traders are the dog; the minority passive investors are the tail. The dog does what it wants. The tail only follows.

If dogs don’t do it for you, I like the boat analogy. Think of actively managed funds and active traders as large cruise liners and passive investors as a small canoe. The cruise liner picks its course. The canoe ropes onto the cruise liner and gets a free ride. The cruise liner doesn’t notice the small canoe’s drag whatsoever; its course is unaffected. This big-small relationship is the original assumption behind passive investing. Market behavior is dictated by the active majority, and the passive minority gets a free ride.

However, asserts Green, we now live in a paradigm where active and passive investing are too close in size. Therefore, the fundamental assumption no longer rings true.

Millions of Average Janes and Joes–individual investors–are using index funds to invest huge portions of their income and savings. After all, that’s how many 401(k)s and their non-American equivalents are set up. Green points out how recent U.S. legislation changes are pushing 401(k)s and passive investing even further into the mainstream.

Passive investing is no longer the “small tail.” It’s no longer the canoe. It’s now a fairly large boat, and the active management cruise liner is impacted by towing such a large passive boat.

The past 30 years have seen index funds grow and grow. Index fund inflows are the “single largest transactors in the market by far” Therefore, by definition, they are not passive. Index funds have to be influencing the market. What might this influence look like?

Passive investing influences the market

Let’s go back to our S&P 500 index fund from before. The S&P 500 went up ~30% in 2019. Where does this gain come from?

Some of it probably comes from fundamental growth in the S&P companies. They’re doing better! Active investors respond by saying, “If the company is better, then these stocks are now worth more!”

Alternatively, what happens when millions of individual investors put their retirement savings into S&P 500 index funds? It’s simple supply and demand. Joe and Jane are increasing the demand for S&P stocks, therefore the price will increase.

When Joe and Jane were the “small canoe,” their demand didn’t affect the market. But these passive investors are no longer “just along for the ride.” They are actively impacting the ride. Last year’s 30% price increase is not based only on fundamental growth. Instead, the Average Janes and Joes are artificially increasing the price of the S&P 500 via their demand for index funds.

The effects of “index inclusion”

What about “Company 501;” that is, the first company not in the S&P 500? Well, it does not receive the benefits of being a part of the S&P 500 index funds. It does not receive the demand that occurs from inclusion in that index fund, and this exclusion affects Company 501’s price.

Mike Green says that historical data clearly shows this growing impact on asset values–it’s called “index inclusion.” This is true for all sorts of index funds. They include some stocks, exclude others, and there’s a recognizable delineation between those included and excluded.

Green says there’s a “distinct and permanent shift in the valuation and price levels associated with these securities” when they are included or ejected from an index. Companies inside of indices are receiving more attention than they fundamentally deserve. Companies outside of indices, therefore, are getting the cold shoulder. This lack of true valuation is one of the formative factors of a bubble.

“Fire!” in a theater

In the past 40 years, passive investing has done nothing but grow. But eventually, that growth will end. Individual investors will retire. Withdrawals will take place. What happens when you take the money out?

At that point, Green states that the artificial inflation of index funds will cease, and quickly turn south. As more retail investors sell, prices will drop. When investors see prices dropping, they’ll get scared and sell more. The vicious cycle will continue–sell, drop, sell more, drop more–into a index fund crash. It’ll be an old-fashioned bank run.

Or, as Nicholas Nassim Taleb has written, “the market is like a large movie theater with a small door.” If everyone is looking to get out, the only way to do so is to offer the doorman a better price than the other people. Prices will plummet. Pop goes the index fund bubble.

Is it the British accent?

Raoul Pal looks the part, sounds the part, and produces his videos while sitting in front of monitors chock full of financial data. My bulls*** detector is whirring to life, but something about that accent is just so factual.

Pal’s argument is that baby boomers–through no fault of their own–have been dumping too much money into passive funds (pensions, 401(k)’s, etc). When they start selling en masse–which will happen soon!–then pop goes the index fund bubble.

There are 76 million baby boomers in the U.S., and their average age is now 65 years old. The wave of retirees is about to crest. And when they start to pull money out for retirement, we will see the large theater/small door issue. Prices will plummet.

But, says Pal, index funds aren’t the only issue. Boomers will also face issues trying to sell their houses. They’ll have issues trying to sell their material goods. Baby Boomers were such prolific consumers that the economy will be overwrought will all their stuff, and prices everywhere will fall. Growth will cease as markets are flooded with goods. A vicious cycle will ensue.

And then “the doom loop of corporate debt will get ignited.” Oh no, not a doom loop! In short, says Pal, corporations have recently gotten into the habit of:

- Borrowing money (this is the corporate debt)

- Buying shares of their own stock—a.k.a “stock buy backs”

- …which drives the price of their stock higher (P.S. this is an artificial price increase)

- …which makes the company appear more valuable, and usually lets the biggest stockholders (e.g. the executives) get extra rich

And Pal’s right. Corporations have been gluttons for their own stocks in recent years. Just read about Apple’s buyback tactics.

Read more about Raoul Pal’s “doom loop.”

Eventually, these corporations will have to pay back their debts. And their artificial valuations will come back to Earth. Stock prices will plummet. Indexes and pension funds will plummet. And Baby Boomers’ selling will cause further pricing drops.

It’s a perfect storm (is Pal just George Clooney in disguise?).

And thus, claims Pal, the third Baby Boomer crash will occur. And every good story has the symmetry of threes.

Enjoying this article? Subscribe below to get new articles emailed straight to your inbox

Problems with Pal

My core issue with Pal is that he’s as much a story teller as he is fact teller. And therefore, it’s hard to tell if he’s selling olive oil or snake oil.

For example, this sounds impressive: “The baby boomers accumulated the greatest concentration of wealth the world has ever seen. And they’ll destroy it too.” Whoa! Rise and fall. The double-edged sword. The boomer giveth, and the boomer taketh away.

Pal provides facts to back up his claims. But most of his facts are arguable at best.

The 2000 Dot Com bubble? It happened because Boomers flooded the stock market with their investments, says Pal. And then “everything got dashed on the rocks, as those markets collapsed.”

The Baby Boomers–then age 45 on average–turned to real estate, says Pal. Can you guess what happened next? The 2008 Subprime Mortgage and Financial Crisis! Baby Boomers are so many in number, says Pal, that their sum-total behavior can’t help but create bubbles.

After 2000 and 2008, the Boomers were worried about their retirement savings, goes Pal’s argument. So now they’ve got to take risk, and they were forced to do so in the stock market. Well, what’s the easiest way to invest in stocks? Through passive investing! And as we’ve now learned twice–according to Pal–where the Boomer money goes, a bubble will soon follow.

It’s a nice story. It has symmetry. It has foreshadowing. It’s narrated with a silky British accent.

But that doesn’t mean it has an iota of truth. Euphoric day-trading of “.com” companies led to the 2000 Dot Com bubble. Passive investing is the exact opposite of that kind of behavior! Perhaps the money is coming from some of the same people, but that’s not evidence of the existence of an index fund bubble. Pal is grasping at straws.

Michael Burry: Big Short to Big Bubble

Michael Burry is an investor and hedge fund manager who correctly foresaw the 2008 financial crisis, and managed to make a boat-load of money for himself and his customers through his correct prediction. If you’ve seen the movie The Big Short, Michael Burry is played by Christian Bale.

Burry’s argument for an index fund bubble is less scary than Green’s, and certainly less apocalyptic than Pal’s.

Burry’s claim is that indexing has caused an artificial bubble that’s inflating stocks inside the index, thus leaving stocks outside the index ripe for the picking. It’s the “index inclusion” argument again.

But where Green sees a dangerous bubble, Burry sees more of an opportunity. Ready for another metaphor?

Imagine a pair of identical twin basketball all-stars. Everything about them is the same, including their skills. Except that one twin plays college ball for Duke–he’s always on TV–while the other plays for Harvard–a good academic school, but not a basketball Mecca.

The average basketball fan would be biased towards the Duke player. He’s on a better team, he gets more media coverage, and has more post-season success. The average fan would certainly believe that the Duke twin has better long-term prospects, and therefore would deserve a bigger professional contract.

But since I built this strawman hypothetical, you and I know the truth! The two twins have the same exact skill set. Therefore, signing the Harvard twin at his lower perceived value would be quite the financially efficient move.

Michael Burry’s claim is that this is what’s happening with passive investing. Near-identical companies are being over- or under-valued due to their index inclusion or exclusion.

Stocks that are inside of index funds are like the Duke twin–they are being over-valued because of their inclusion. While stocks not in the index are like Harvard twin–they are under-valued, and therefore should be targeted by smart people looking to make more money.

In my opinion, this is less of an “index fund bubble” and more of an “anti-index opportunity.”

Burry is simply saying, “There’s an inefficiency here, I’ve discovered it, and I plan on making money off it. P.S.–come invest with me so we can both make money together.”

Good work, Mike! Go exploit that inefficiency!

Price Discovery is becoming fragile

Burry’s second claim is that price discovery is becoming fragile. “Price discovery” is a fancy term for “buyers and sellers determining a price where they’re willing to make a deal.”

Think about Craigslist. Someone wants $200 for a used snowblower. Snow?! Yes, in Rochester it helps to have a snowblower. So, you take a look at the snowblower and counteroffer $150. The owner haggles back to $175…and you have a deal! That’s price discovery.

Typically, stock market price discovery involves many buyers and sellers conducting detailed analyses of a company’s holdings and profits and cash flows–all of the fundamental business metrics.

But passive investing doesn’t care about those fundamental metrics. Instead, passive investing simply follows the leader. It assumes that others in the market have already done the fundamental research, and that the current price of a stock is “right.”

It’s a little bit like saying, “The last Craigslist used snowblower went for $200, so I’ll buy the next one for $200 sight unseen.” Are you sure you want to trust the last buyer and seller? What if they were dopes? Don’t you want to look at the snowblower and make a decision for yourself?

Since passive investing doesn’t rely on price discovery, Burry argues that prices are now dangerously skewed from what traditional price discovery would suggest. This cannot go on forever, and eventually the prices will snap back to where they fundamentally belong.

Or, you could say, the index fund bubble will pop. This, Burry says, is very similar to how housing and CDO pricing behavior malfunctioned before the 2008 crisis. It will be a painful, painful snap.

Part II – The other side: Index funds are fine

While I appreciate the logic behind Misters Green and Burry and Pal, there’s plenty of good money still betting on index funds’ future success. Let’s start with Ben Carlson. Ben is financial analyst, author and blogger (nice!), and podcast host. I’m a big fan of A Wealth of Common Sense (the blog) and Animal Spirits (the podcast). Thanks for sharing all the good work, Ben.

Anyway, what does Ben have to say about the index fund bubble and passive investing?

The tail is not wagging the dog.

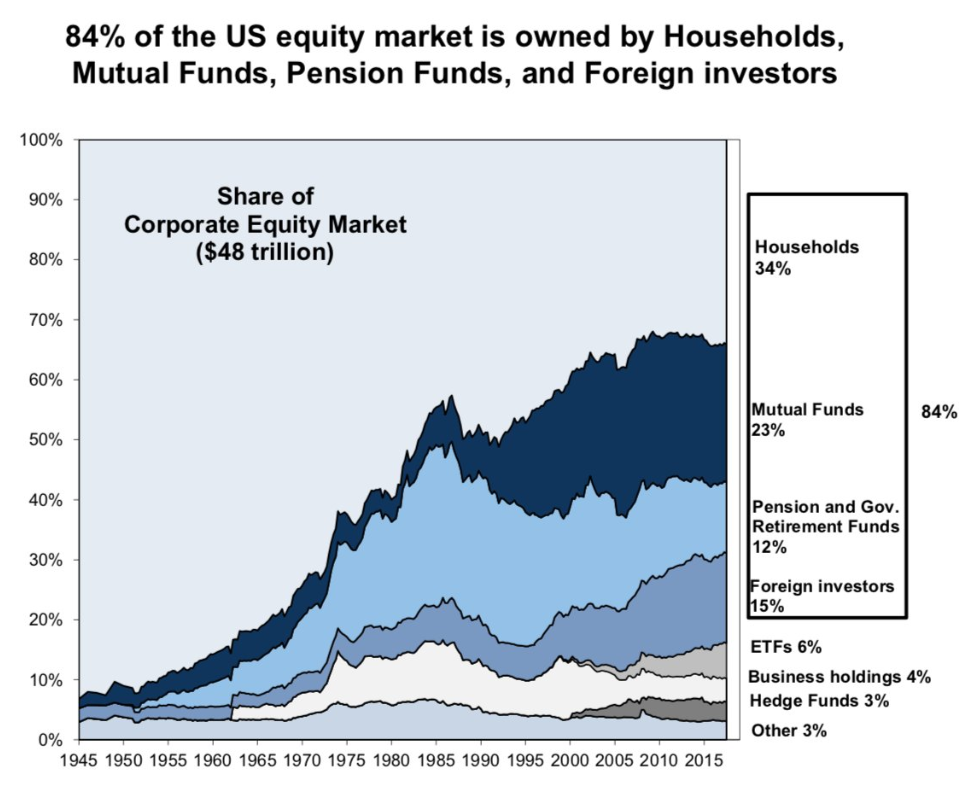

First, let’s get back to dogs and tails and boats. Carlson writes, “Index funds hold less than 15% of shares in public companies.” While this is a growing number–it was 3.3% in 2002 and 6.8% in 2009–passive investing is neither a majority nor plurality.

If we combine all exchange traded funds and all mutual funds, that percentage rises to about 35% ownership of all shares. That means that active investors–the dog–own at least 65% of the equity market, and therefore are still wagging the tail. All is well in the dog/boat metaphor universe, says Carlson.

Bias! Bias! Read all about it!

Another of Carlson’s arguments is that active investing, by nature, is biased against passive investing. Passive is stealing active’s business share, and now active is biting back.

Passive investing shadows what the active investors are doing. But rather than spending money on research and trades, passive investing keeps expenses–and fees–to a minimum. Passive has all the profits of active investing, but none of the costs: ipso facto, passive investing is better. And the active investors don’t like it! The “index fund bubble” is their propaganda technique.

Besides, let’s consider any and all claims that passive investing is doing something “wrong.” Logically speaking, anything that passive investing is “doing wrong” first has to be done by active investors.

You can’t blame your shadow for flipping you the middle finger–the shadow only copies the source. Similarly, passive investing only copies what active investors are doing. It’s a simple argument in logic.

The price discovery argument

Price discovery is a cop-out, says Carlson. There is way more trading occurring today than most times in the stock market’s history. In the book Index Revolution, author Charley Ellis writes that about 95% of all trades today are done by active managers–there’s plenty of opportunity for price discovery. It’s all about trading volume.

This means that the prices aren’t skewed. The prices aren’t a stretched rubber band, ready to snap back. There’s no index fund bubble, waiting to pop. Instead, the active investors are setting the prices and price discovery is healthy.

So what’s Michael Burry worried about?

Besides, Carlson says, when else in life do we expect individuals to actively partake in price discovery? Do you haggle with the grocery cashier about the cost of oranges? No! All over our economy, prices are set and individual consumers simply choose to buy, or not. They don’t barter or bargain.

I’m not sure I agree with Ben’s point here. It’s true: we don’t haggle at grocery stores. Instead we’re presented with Hobson’s choice–we either take it, or leave it. If you don’t want to pay $12 for a bag of oranges, you don’t have to.

But are people thinking about Hobson’s choice when they passively invest in index funds? I don’t think so. I think a lot of people are “blindly” putting their bi-weekly 401(k) contributions into index funds, regardless of the price. There’s not much “take it, or leave it” going on. It’s just “take it.”

My conclusion: index investors might be blindly buying in, but they’re still buying at a price that was intelligently discovered through the fundamental analyses of active investors.

Ben Felix from YouTube

Ben Felix is a portfolio manager at PWL Capital, and popular creator of YouTube financial/investment videos.

I really like one of Felix’s foundational arguments against the idea of the bubble. That idea is: assets under management do not set prices; instead, trading sets prices.

So Green and Burry should not be asking, “How much money is in indexes?” Instead, the question should be, “How much trading is done by indexing?” This means that the size of the boats doesn’t matter. In fact, it means the boat metaphor doesn’t really make sense.

So let’s relate it back to the quote from Charley Ellis: 95% of all trades today are done by active managers. That means that price discovery is dominated by active trading. And it means that there shouldn’t be any bubble driven by price discovery.

Blackrock, another investment management firm, estimates that for every $1 of passive trades, there are $22 of active trades. Again, this points to the same conclusion: there is no issue with price discovery.

Some ideas from the academics

Felix quotes a couple serious economics papers–one by Fama/French, another from Palia/Sokolinksi.

Fama & French came to the conclusion that it doesn’t take much active investing to create an efficient (i.e. non-bubble) market. Passive investing, they say, is pushing bad active managers out of the market. And those who remain? Only the skilled active managers. It’s survival of the fittest. Culling the weak should only make the market more efficient. More efficient = better price discovery = no bubble.

Palia and Sokolinski have a really interesting theory. In brief, they claim that index funds drive down the cost of short selling, which makes short selling more efficient, and that leads to better price discovery.

They start with the simple truth that index funds hold onto lots of stocks. And since the supply of stocks is high, index funds can easily lend out those stocks to short sellers (people betting that a stock will go down). The short seller pays the index fund a small fee, which gets passed onto the passive investor in the form of low costs.

However, since there are so many index funds out there, the short sellers have many different options of where they borrow stocks from. With high supply comes low prices. They can find their short sources very cheaply. This makes the cost of shorting go down.

And thus, conclude Palia and Sokolinski, passive investing is creating a more efficient market for short sellers, and a more efficient market leads to better price discovery.

Part III – Home-grown arguments and takeaways

Now that you’ve heard the smart people talk, let me bless you with my pro-index ideas.

First, index investing is self-corrective.

To wit, let’s take another look at Michael Burry’s argument: “passive investing has an inefficiency in undervaluing non-indexed companies, and I plan on taking advantage of that.”

If Burry is correct, then more active managers will follow his lead and make their money. And right behind them will be their shadow a.k.a. passive investing. The market is a self-correcting system, where money flows towards the best values. Passive investing simply follows that flow of money.

If passive gets too influential, then the smart active managers will exploit the problem. Inefficiencies will balance themselves out in the long-term. And passive investing is a long-term technique.

Second, it’s easy to avoid the pitfalls of index inclusion.

Index funds don’t have to exclude stocks. Many investment managers (like Fidelity and Vanguard) offer total market index funds. They include high and mighty S&P companies and all of the “company 501’s” out there that might be excluded from other index funds.

Therefore–if there is an index inclusion bubble–the total market index funds own both sides of that bubble.

A total market fund would only be exposed to a bubble that includes entire asset classes. For example, one could claim that stocks in their entirety are overvalued, but that commodities are undervalued. Therefore, a total U.S. stock market index fund would still expose you the bad outcomes of bursting bubble!

If this concerns you, then diversify your index investing via a lazy portfolio. There are indexes that track bond markets, international markets, different sized companies, commodities, REITs, etc. You can spread out your investments across multiple asset classes to reduce your risk.

Takeaways

Green and Burry both make good points. Pal tells a nice story. I’m really glad I took some time to understand those ideas. Carlson and Felix support the ideas I’ve always heard: the wisdom of people like Jack Bogle and Burton Malkiel. What actions am I taking after all this conversation?

Reading. Lots more reading. I want to learn more about Mike Green, Michael Burry, and and their anti-passive compatriots. After all–they did compel me to type up 4000 words of arguments that go against my investing strategy. But I also want to remind myself of the reasons why I started indexing in the first place: Malkiel, Bogle, and people like Ben Carlson and Ben Felix.

But I will be staying my course, at least for now. I have not been convinced to move away from indexing, or that there’s an index fund bubble. Indexes still float my boat, and I think the bubble argument has more bark than bite. I’m in it for the long run. I do not think hand-picking individual stocks is the way to go.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

Well that made me feel anxious and then not anxious about having half my networth in index funds… sounds like I can stay the course. Some are SP 500 and some are total market. I’m not trying to get rich I’m just trying to build security and indexing still seems like the way to go!

Hey Justin. Thanks for reading and commenting. I’m right there with you. The arguments made me feel anxious too. But I’m staying the course. My Lazy Portfolio (large cap index fund, small cap index fund, bond index fund, and international index fund) makes me feel like I wouldn’t be too exposed even if there was a bubble.

-Jesse

Pingback: Plutus Awards Weekly Showcase: April 3, 2020 - The Plutus Foundation

Bravo.

Cheers!

Pingback: 35 Easy Ways to Generate Passive Income in 2020 - Mobile Witch

Pingback: 35 Easy Ways to Generate Passive Income in 2020 | Financial Health Today

Pingback: 35 Easy Ways to Generate Passive Income in 2020 - Bella Wanana

Pingback: 35 Easy Ways to Generate Passive Income in 2020 - Savology

Pingback: 35 Easy Ways to Generate Passive Income in 2020 - Money Saved Is Money Earned

Pingback: 35 Easy Ways to Generate Passive Income in 2020 - Money Mix

Pingback: 35 Easy Ways to Generate Passive Income in 2020 - Wallet Squirrel

Pingback: 35 Easy Ways to Generate Passive Income - Partners in Fire

Pingback: 35 Easy Ways to Generate Passive Income in 2020

Pingback: 35 Easy Ways to Generate Passive Income in 2020 - The FRUGAL TOURIST

This was an excellent article presenting both sides of the argument. I was in the bubble camp initially but agree that long term, markets correct and passive will follow active lead. The rapid flow up capital into index in a relative short amount of time is a little concerning though. Thanks for writing, I enjoyed.

It’s a wild topic, right? Hard to know what’s right. Thank you for reading!

Pingback: 35 Easy Ways to Generate Passive Income - The Female Professional

Great article – I’m glad I came across it. FYI, Buffet put 90% of his wife’s assets in VFIAX and Munger loves low cost, low turnover Vanguard funds. I think Average Joe can trust Warren’s and Charlie’s assessments. Bogleheads are not going extinct anytime soon.

Hey, thanks G. Spencer!

Thanks for the article! I read most of it. (It was long aha) I appreciated hearing both sides of the story and also all the clever metaphors and illustrations. This definitely gives me more confidence in my decision.

Hi Daniel! Agreed–it IS long haha! I appreciate you coming by to read.

Hope to see you coming back, let me know if I can help.

-Jesse

Pingback: Thursday’s Top Three (TTT #011) – Money Savvy Ladies

This was a _great_ article – I read it 3x. I’m also a passive investor, but I think it is important to challenge your thoughts/beliefs.

One minor critique: you provide links to Ben Carlson, Ben Felix, and Mike Green, but no links to claims made by Michael Burry or Raoul Pal. As someone who is willing to entertain the other side, I’d like to hear their thoughts first-hand.

Dharma turtle, hello! Thanks so much for the kind words. That’s a terrific critique, and it has been amended! I included a couple links into the article in the right spots.

Cheers!

Jesse