I recently ran a stock picking competition. The rules were simple. Every morning, I gave the stock pickers two stock choices. I knew that one stock would go up, and the other down—I guess I’m just prescient. The goal was to find the skilled stock pickers, and weed out the unskilled. I was seeking an answer to the question, “Is stock market success just luck?”

Every time a competitor picked correctly, they earned a Franklin Buck™. But every day that they chose poorly, I charged them a Franklin Buck™. I ran the stock picking competition for 100 days, and 100,000 people participated.

That’s right, 100,000 people: it was the 100 Best Interest followers, plus another 99,900 people I know.

Among all these people, I knew I’d be able to find someone with some real skill. A genuine winner. There would be a justifiable pattern of repeated success that would suggest, “For this person, stock market success is a talent, not just a coin flip.”

And I was right.

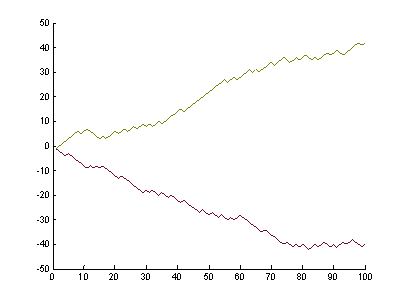

Here are the best and worst competitors’ picks, plotted out for the 100 days.

The best picker ended with $F42. In other words, they had 71 good picks and 29 bad picks. Look at that hot streak starting around Day 35; that’s a lot of Franklin Bucks™!

The worst score ended at -$ F 40, or 70 bad picks to 30 good picks. Consistently terrible through day 75, and then they leveled off. Go fly a kite!

If I ran the competition a second time and you had to invest with one of these two people, the choice would be clear.

Or would it?

This might blow your mind, but I haven’t been forthright. Prescient stock picking? 100,000 competitors? Franklin bucks?! Yes, I’ve fudged some of the details about what’s gone on here.

This wasn’t stock picking. It was actually coin flipping; simple, lucky, 50/50 coin flipping.

And there weren’t 100,000 real people. My 100,000 friends all had dental appointments and dead grandmas’ funerals during the past 100 days, so instead I leaned on my old pal Matlab to simulate the coin flips. I ran 100,000 simulated trials of 100 coin flips each. And the results in the graph above are the best and worst of those simulations.

By the way, Franklin Bucks™ are not yet official currency, although I am working on a crypto deal with the same people who made DogeCoin—keep your eyes peeled!

Despite all this farce, it looks like real data! It looks like a trend, like we should be able to draw conclusions from it. You want to say, “One ‘person’ was obviously a better stock picker or coin flipper than the other…right?”

Random Noise

But it’s all random noise.

In other words, there was zero skill involved in the coin flipping. There is no causation—you can’t say that one person is a better coin flipper than another. It’s random! And that means that prior results—the run of flips that I show you—has no bearing on future results. Each flip is 50/50, despite whether someone has previously been good, bad, or neutral at their flips.

The next competition—which I asked you to invest in—will have zero correlation to this one!

“WAIT!,” scream the critics. “The analogy here is dog crap. Coin flips are pure luck, while stock picking is an enterprise of skill. Stock market success isn’t lucky. These Wall Street people must develop some secret knowledge (e.g. a skill) that I don’t possess, right?”

Well, that’s a terrific question. A recent MIT study looked at various games to see how much “skill” was actually involved.

Coin flipping, one would think, would be 0% skill and 100% chance. While chess—a turn-based game where both players see all information at all times—would be 100% skill.

The MIT scientists “reasoned that if a game were more skill-based, then a player’s performance should be persistent. It might be good or bad, but it would remain relatively constant over multiple rounds.” Magnus Carlsen—the world’s best chess player—is going to beat me 100% of the time, because chess is so highly skilled. The same can’t be said for coin flipping.

On a scale of zero (pure luck) to one (pure skill), coin flipping indeed ranked a zero. It’s pure luck. But moving back towards the stock market, the study also looked at 45,000 mutual funds’ performances from 2005 to 2015, and ended up giving mutual funds a score of 0.32. Some skill, sure, but mostly luck.

Is stock market success just luck? MIT says, “Yeah, mostly.”

Enjoying this article? Subscribe below to get new articles emailed straight to your inbox

Professional stock pickers

Remember, mutual funds are run by professional stock pickers. These are people who might charge 1%, 2%, or more of your portfolio every single year for the luxury of their genius. Perhaps certain individuals demonstrate a particular skill, but the group as a whole is controlled by luck.

While I would never beat chess champion Magnus Carlsen, I could reasonably get lucky and beat most professional mutual funds. This idea is supported by additional studies and hard data in the Boglehead’s Guide to Investing and A Random Walk Down Wall Street.

When you put money into your 401(k) or Roth IRA or a brokerage account, you’ll often be given dozens, hundreds, or even thousands of different fund choices. Which to pick?

Well, you might look at past performance—past 1 year, 3 years, 5 years, etc—and pick a fund that has done well recently. But since mutual funds tend to have luck-driven results, you’d be making a fundamental error.

As the MIT scientists explained, “a player’s performance should be persistent” if the game is skill-based. Only then will performance “remain relatively constant over multiple rounds.” If you look at a mutual fund’s past performance in hopes that performance will “remain relatively constant” in the upcoming years (i.e. the years while you’re invested in it), then your hopes are misplaced. Mutual funds’ past performances are not predictive of future performance. Or more simply, there’s little causation.

Maybe you’ll get lucky and the fund will stay strong. But that stock market success is luck.

Lazy = Good (…at least in stock picking)

So if you don’t look at a fund’s past performance, what do you look at?

The answer, in my opinion, involves the “Lazy Portfolio” that many so-called “Bogleheads” use. Since luck can play a prominent role in investing, this Lazy Portfolio uses a few different tactics to reduce costs and level-out the role of luck.

- Invest only in low-cost funds. Rather than paying a coin-flipper 1% or 2% per year, many index funds only charge 0.1%, 0.05% or even 0% to invest in. They know that they are not doing anything genius for you, and they charge you accordingly.

- Index funds are, by their nature, fairly immune to the coin-flipping luck. Rather than selecting specific stocks to invest in, index funds invest in entire swaths of the market. Index funds bet on the average. The economy usually grows, so average means your portfolio is growing.

- The Lazy Portfolio further hedges its bets by investing in a few different index funds that tend to be uncorrelated. For example, a Lazy Portfolio might invest in a Large Cap (a.k.a. big company) index, a Small Cap (small company) index, an International (not U.S.A.) index, and a Bond (fundamentally different from stocks) index. Generally, the economic forces affecting Large Cap stocks are different than forces affecting International stock and Bonds, etc. Low correlation = less risk.

But, I know a good stock picker!

Most of us know someone in life who seems to buck the trend. So now that I’ve harped on the idea of luck-based stock market success, some of you might have some pretty good arguments about people you know. Let me play strawman lawyer and address a couple arguments…

“My friend has been trading for fun for the past five years, and his portfolio is up 50%! That’s great, right?

While it does sound great, the truth is that the entire market is up 55% since the start of 2015. So while your friend has made some money, he would’ve been better off doing absolutely nothing active, and instead just investing in a passive index funds that tracked the whole market.

“My other friend has been trading for fun for the past five years, and her portfolio is up 200%!!” What’s your criticism now?!

Fair enough! It’s not easy to look at one data point and tell the difference between skill and luck.

But if she’s utilizing leverage at all, she’s playing with fire. Her 200% gains look great thanks to the recent bull market, but she might take an extra long tumble if the market takes a bearish turn.

“Ok jerk. My dad is up 200% and he’s not using your fancy leverage. What’s your story now?!”

Your dad could be skilled. Or he could be one of the coin-flip winners of this round (e.g. the past 3, 5, 10 years…however long it’s been). Granted, the longer he’s been successful, the more likely it is that he is truly skilled.

But let’s say he’s had a hot streak of 6 months. Do you believe enough in those 6 months of results to invest with him for the next 5 years? Will you bet your retirement funds on it?

It takes skill to recognize skill

If you’re still skeptical of what I’m saying here, that’s good. I encourage an open mind, and I’m just one voice in the crowd. Do your own research (and let me know what you find!) and come to your own conclusions.

But if you are considering sticking with your managed mutual fund, or joining an actively managed fund, or paying someone a high percentage (e.g. 1-2%) to manage your investments for you, then consider asking the following questions.

Am I, the reader, an expert enough to determine whether this money manager is actually skilled?

You know your Uncle Dave…the one who runs into chairs and pulls his back every winter shoveling snow? You know how Uncle Dave loves to yell at all the stupid sports coaches? Football, hockey, basketball…doesn’t matter. Dave, despite having zero athleticism or sports history, considers himself to be a sports expert.

“Of course. Of course they would draft another linebacker. We need a quarterback!”

Thanks Dave!

I, like you, would argue that Dave is not expert enough to be saying the things he says. He doesn’t have the experience nor the understanding. But thankfully he also doesn’t have to suffer any consequences when he’s wrong.

When you pick someone to handle your money, you should understand if they’re skilled. And if you don’t possess the experience or the understanding to make that decision, then you might be like Dave screaming at the TV.

Except that your wrong opinion could have dire financial consequences!!

And not just a little skill…

Assuming I, the reader, pick a truly skilled money manager, are they skilled enough to justify themselves?

Remember, someone who sells their services to invest your money can’t just be good. They need to be so good that they beat the market by enough to justify their costs.

If they are average, then they will have average returns. You can get average returns for almost zero cost using passive index funds. Why would you pay someone 2% of your money when you could do that for free?

You don’t pay a contractor to lay shingles only as well as you can lay shingles. You expect the contractor to lay shingles like an expert. By the way, Uncle Dave loves to critique contractors. Dave also once shot a nail gun through his thumb.

If your financial adviser charges a 2% fee, then they need to be average plus another 2%. As of this writing, the S&P 500 is up 23% this year. If my money was being actively managed with a 2% fee, then I’d sure hope my investments were up at least 25.5% (1.23 * 1.02 = 1.2546). That way, after I paid my 2% fee, the leftover money would represent at least an average return.

Otherwise, why am I paying a “skilled” person?

Parting advice: stock market success is mostly luck-based

So if you’re deciding what to do with your money, you should understand the role that luck can play in stock market success.

If some investor or salesman tries to convince you that they’re special, then just go back and think about my winning coin-flipper. His recent results looked special. But his actual talent for picking winners was as real as my stock picking competition itself.

Be wary of a self-proclaimed stock genius. It might just be someone’s Uncle Dave.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

I apologize for the self-serving plug here, but I think a question people might ask is “why the heck work with a financial planner if the market is luck and low cost laziness will provide good returns?”

I’m glad you asked! As a speaker I listened to the other day pointed out “investments are a matter of opinion. Taxes are a matter of fact.” A good financial planner helps with all the things you can control (risk, taxes, income planning, etc.) to accomplish your goals efficiently and effectively. If the only thing a financial professional brings to the table is stock picking, you probably should be skeptical.

That’s a great point, Craig. Thanks for calling that out.

My post (this article) is fairly “one-dimensional” thinking about investing in the market, but you bring up a few other axes to think about.

Putting together a 20-, 30-, or 40+ year plan isn’t straightforward, and goes beyond my simple “what are you invested in?”

Really awesome article!

Personally, I keep most (about 70%) of my investments in index funds, and the remaining 30% in individual stocks. Since I was a little kid, I’ve always enjoyed investing in individual stocks, feeling part of the team, and checking my portfolio each morning. For me, the excitement of investing in individual stocks has actually helped me invest more than I would have otherwise done.

Thanks Nate! I’m glad you liked it.

I’ve heard a few different ideas similar to yours. One of my trusted mentors is almost exactly like you. He tells his advisor to be 70% ‘beta’ (e.g. index funds) and use 30% of his portfolio to seek ‘alpha’–beating the market.

A different view from the late, great Jack Bogle: take 5% of your portfolio for fun money. Single stocks, crypto, whatever. Go enjoy. But the other 95%, apply smart, tested investment principals.

Pingback: Guest post from Jesse at Best Interest – Financial Velociraptor

Pingback: Ayy! Corona: the stock market and coronavirus - The Best Interest