Every year, Vanguard publishes a mammoth report called, “How America Saves,” sharing data from Vanguard’s 4.9 million employee retirement accounts (401(k), 403(b), etc).

Let’s take a peek at the data and see how you compare. Are you saving enough?

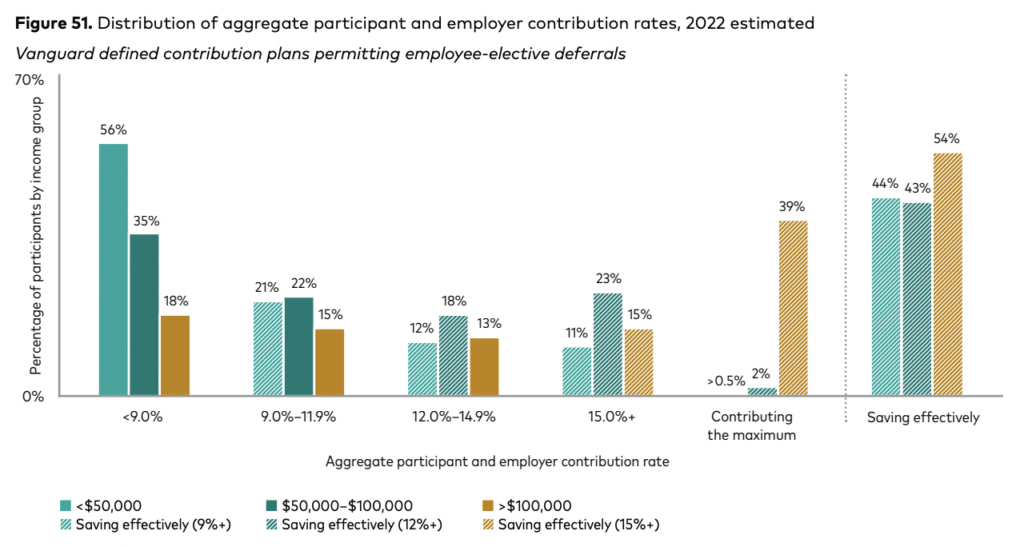

Savings Rate

The median deferral rate in 2022 was 7.4% of salary from the employee, plus another 3.9% from the employer.

Not bad! Remember, this data does not account for any other types of savings (IRA, taxabale brokerage, HSA, etc).

Ideally, a total savings rate is at least 15%. Even better at 20%. Anything above that and you’re killing it! So, 11.3% into a retirement account is a solid savings rate. Good work, America!

Based on Vanguard’s subjective (but quite reasonable) opinion, roughly 40-50% of Americans are “saving effectively” via their employer-sponsored retirement accounts.

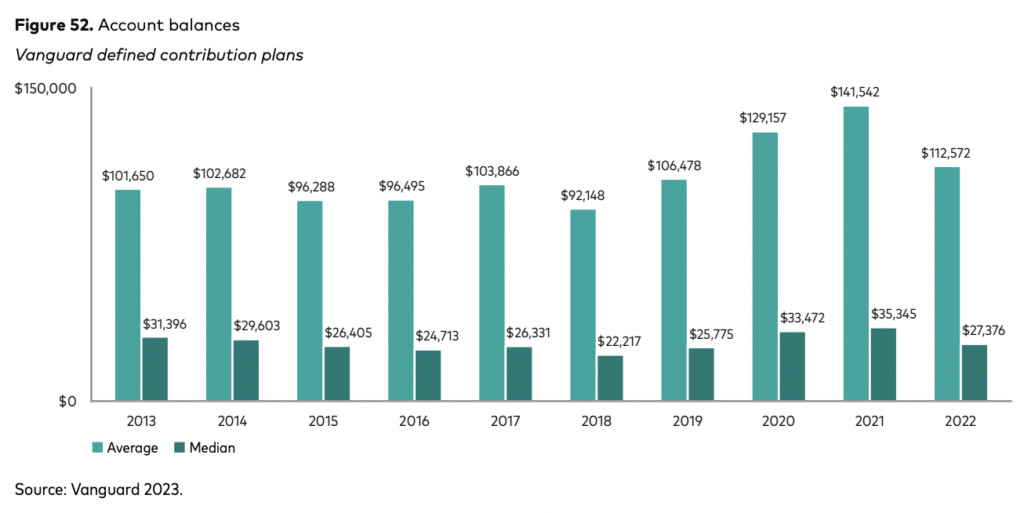

Average Balance

The average (mean) participant balance in 2022 was $112,572, and the median balance was $27,376. That’s down ~20% from 2021 – not a big surprise, considering market performance in 2022.

This skew of mean >> median happens a lot in financial data! A few big fish drag the average up, but affect the median much less. About 60% of participants have an account less than $40,000, while 12% have accounts larger than $250,000.

But wait! Despite this “skew,” we still need to face the fact that the average person only has $112K saved for retirement?! That’s way too low. And scary! …right?

We need to pause. This is a prime example of the famous quote:

There are three kinds of lies: lies, damned lies, and statistics.

Why? Because significant retirement savings exist outside of 401(k) and 403(b) accounts. The median participant in this study is 43 years old and the median account age is seven years old. Those numbers don’t jive! How can a 43-year-old only have a seven-year-old 401(k)?

Answer: they’ve switched jobs and rolled their old 401(k) into IRA accounts. That’s what I did!

I would appear in this study as a 33-year-old with an 18-month-old 401(k), with an approximate balance of $15,000. The study would not be aware I used to have a 6-figure 401(k) at my old job that I rolled over into an IRA when I switched careers at the end of 2021.

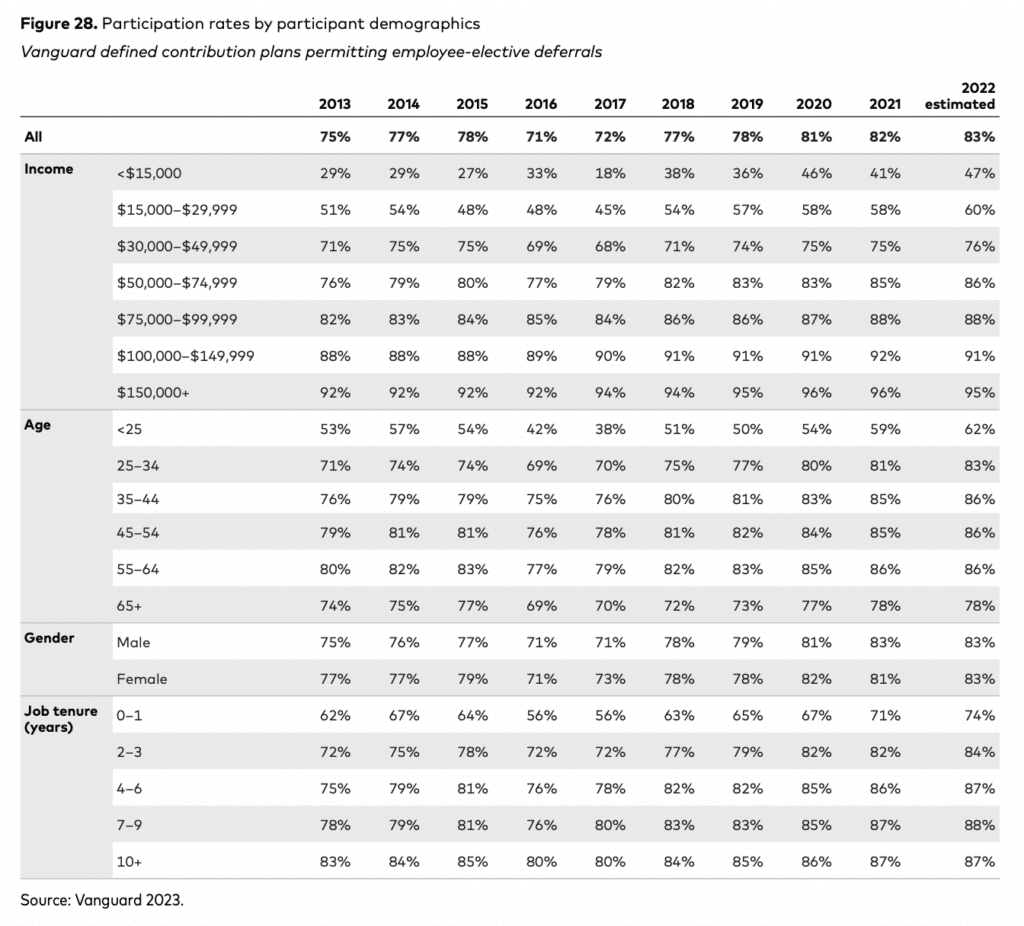

Participation

While plan participation is growing year after year (nice!), the sore spots are obvious: poorer, younger, and less tenured workers are saving less than their richer, older, more experienced counterparts.

This isn’t surprising at all. But it’s all the more reason for widespread financial education. Share The Best Interest with a friend in need!

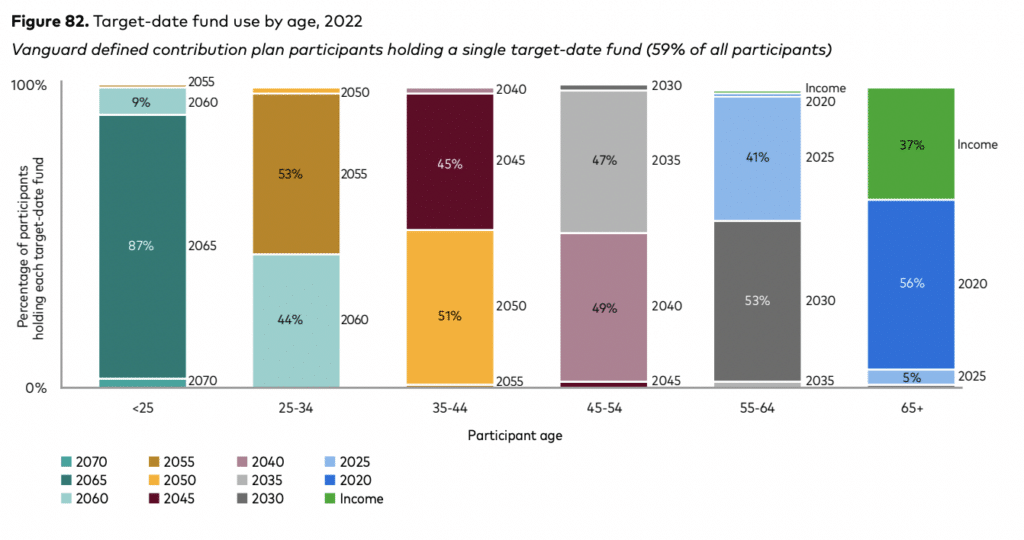

Target Date Funds

A whopping 83% of all participants used target-date funds, and 71% of them had their entire account invested in a single target-date fund in 2022. In total, 63% of all invested dollars were invested in target date funds.

Target-date funds are a good (sometimes great) solution for 99% of you. They are typically priced fairly (I’d like them priced lower, but I won’t quibble) and the automatic age-based allocation removes many potential allocation errors.

In fact, if a Vanguard investor holds only one fund in the 401(k) or 403(b), it’s almost guaranteed to be a target date fund. On the whole, that’s a good thing.

And to an amazing degree, participants are using age-appropriate target-date funds exactly as Vanguard would have intended.

Gliding Toward Retirement

Are investors holding the right amount of stock exposure as they age?

Yes! It’s reasonable for investors to glide down from ~80-90% stocks in their 30s to ~50% stocks near retirement.

But the most enlightening aspect of this table is how fearful investors were in 2005 (in the aftermath of the Dot Com bubble bursting) and 2010 (after the Great Financial crisis). Young investors were only 60% stocks!

Market history would tell us that’s unwise. But written history would remind us of the pain investors feel when they lose money, and the conviction they feel to “not get burned again.”

It’s an important reminder for all you readers. Don’t put yourself in a position where your amygdala convinces you to “sell to survive.”

Getting the “Match”

The “match” in a 401(k) plan is free money from your employer, and virtually always worth pursuing. The majority of participants are getting their full match (left), and even more so when the retirement plan automatically bumps up savings rates year after year.

Automatic Enrollment

The #1 reason people don’t save in their 401(k) plans is because they don’t sign up in the first place. Gah! There is no substitute for lost time!

Thankfully, more and more employers are utilizing automatic enrollment, so their employees start saving from Day 1.

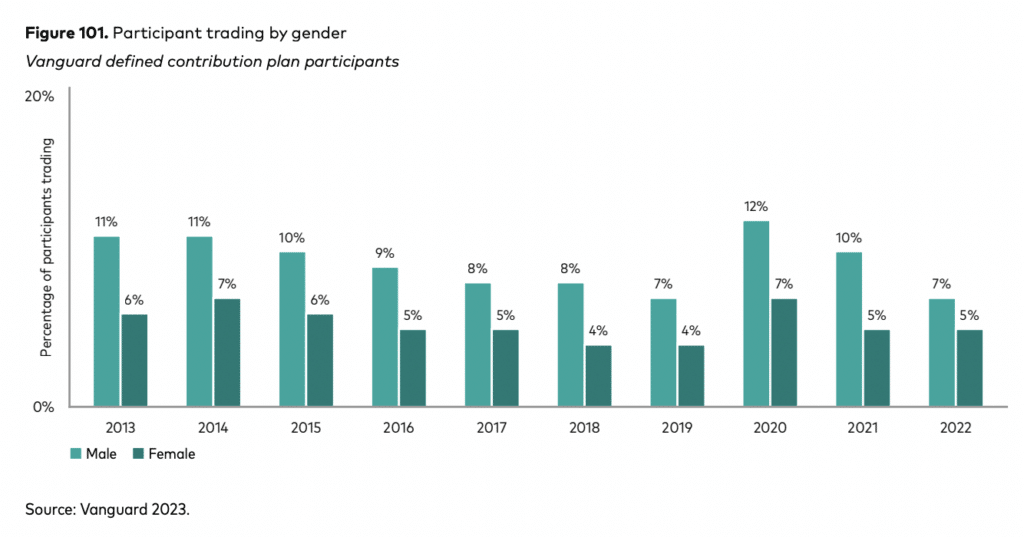

Trading

The best investors are either dead or have forgotten their passwords.

The next best are single women. Then married women, dragged down by their husbands. Then married men, dragged up by their wives. And last are single men, left alone to their devices.

Why?

Trading. Men trade more than women, jumping on winners and abandoning losers after it’s too late. Hence, they underperform.

But on the whole, investors are doing a good job “staying the course.” The data below shows that most investors are looking at their 401(k) balances less than once a quarter. The more you obsess, the more likely you are to act…and shoot yourself in the foot.

If you’re a man, invest more like a woman. If you’re a woman, invest more like you’re dead. Stop trading!

If you have any questions about your workplace retirement plan, send in a question to The Best Interest!

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!