I had a creative brainstorm this week. An idea—that I’ve dubbed bimodal spending—overtook my mind. And now I want to convince you to adopt it in your life.

Bimodal?

First things first, let’s define bimodal.

Out in the real world, it’s common to see normal distributions. They occur when most data clumps around the average, and few data are dispersed at the extremes. A normal distribution looks like this.

Many of us are also familiar with uniform distributions, where data is spread evenly among a range. A uniform distribution looks like this:

But a bimodal distribution, as the name implies, has two (“bi”) modes. It has two distinct peaks, which often occur at opposite ends of the range. A bimodal distribution looks like this:

What is Bimodal Spending?

My creative conception is that we should apply a bimodal distribution to our spending.

Bimodal spending asks you to say either hell yes! or no! to major expenses. Go whole-hog, or go not at all. No middle ground. Keep in mind: the significance of hell yes! fades if you say it too much. You can’t just say hell yes! to everything.

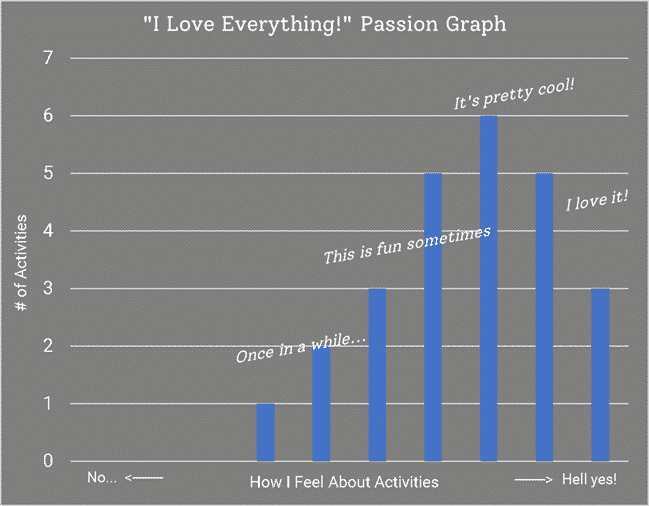

Think of all the things you enjoy. If you’re like me, the list is long. Food, travel, hiking, sports, music. Oh, reading and blogging! Spending time with friends and family. Fostering dogs. I like lots of things!

If I’m not careful, my “passion graph” would look like this:

I could spend $1000’s on each of these pursuits. I could buy lots of stuff, go on lots of adventures. But is this stuff worth it?

I say no. It’s not all worth it. Only some are worth it. We know that luxurious spending brings less fulfillment as we spend more. Why? One limiting factor is time. I don’t have the time to devote to each of these pursuits.

If I try everything, then I’ll spread myself too thin. Being spread thin is not enjoyable. It’s not optimal.

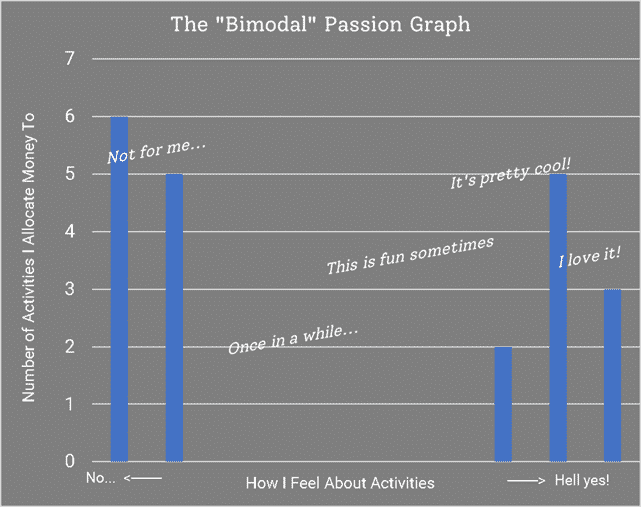

That’s why I’m reimagining my “passion graph” to look like this: a bimodal distribution.

If something is hell yes!, then I’ll devote time and money to it. But if it’s only “kinda fun” or an “occasional pastime,” then I want to prune it from my budget and schedule.

Enjoying this article? Subscribe below to get new articles emailed straight to your inbox

From Bimodal Passions to Bimodal Spending

I want to focus my “fun money” on my hell yes! passions. I want to “rout all that was not life”…or eliminate that which doesn’t light my fire (thanks HDT!). So how does that translate into a bimodal spending distribution?

I want my dollars to either go towards:

- Basic life needs

- Hell yes! passion activities

It should look something like this:

Either the bare necessities or the true marrow of life. Not much in between.

Anything in the middle of the graph will bring me little “fulfillment per dollar.” I want the dollars I spend to do good. Sometimes that’s through charity, giving to others, contributing to group activities, etc. But if I’m spending on myself, I want to squeeze out as much fulfillment as I can.

Here’s a gentle reminder:

Look at the stuff all around you.

That stuff used to be money.

And that money used to be time.

I don’t want to spend money (a.k.a. my time) on average stuff. I’ll pay for the necessities. And after that, I want my spending to make me say, “Hell yes!“

Bimodal Spending = Pareto Principle

Bimodal spending is a rehash of the Pareto Principle, also known as the 80/20 Rule. Focus 80% of your fun spending on your favorite 20% of activities.

Or you can push the ratio even further. Spend 95% of your fun money on your top 5% activities.

The other 95% of your “fun” activities? Spend as little there as you can. They aren’t hell yes! They’re milquetoast. They’ll only pull resources away from the activities you truly enjoy.

Whatever the ratio you choose, it’s amusing that Pareto rears his insightful head yet again!

Ramit’s Rich Life

Bimodal spending is reminiscent of Ramit Sethi’s “rich life” idea. To quote Ramit, living a rich life means having the:

“Ability to spend my time and money on the areas that are important to me.”

Ramit Sethi

How does Ramit suggest you pursue your rich life? Simple. He tells you to “spend extravagantly on the things you love, and cut costs mercilessly on the things you don’t.”

That’s bimodal spending!

Categorize your pursuits as “things you love” and “things you don’t.” Or create a bimodal passion graph!

Spend extravagantly on the right side of your passion graph. And cut mercilessly on the left end of your passion graph. Ramit Sethi is a bimodal spender!

Anecdotal Examples of Bimodal Spending

Friend-of-the-blog Martin loves travel and fine dining. It’s one of his passions. That’s why it made sense for him to spend two weeks in Lima, Peru, and plan a meal at Central (considered one of the best restaurants in the world).

It’s a once-in-a-lifetime experience. The memories of the trip still bring him joy today. That’s a hell yes!

But I contrast Martin’s love of travel against my interest in golf. At one point in life, I had enough time to golf 3-4 times a week. I practiced putts for hours. I could draw and fade the ball. I wasn’t great, but it was a serious pursuit.

But now I only have time to play once a month. I’m constantly out of practice. I don’t have time to regain the skills I once had. I still like golf, but it’s not a hell yes! anymore. That’s why I’m making it a no.

I’m not going to spend $500 for a new set of golf clubs. I’m not going to spend $1000 for a membership at a golf course. For me, those things aren’t worth it.

My hell yes! spending lies elsewhere. I’ll buy $200 hiking boots and a top-of-the-line laptop to support the Best Interest. But not new golf clubs (even though I do like golf).

But Mark (another friend-of-the-blog!) absolutely loves golf. He plays as much as he can. He’s traveled to Ireland to play historic courses. He plays in the rain and snow (because you’ve got to make the golf season count in Rochester!).

New clubs and a course membership help Mark live his Ramit Sethi “rich life.” Golf is a hell yes! for Mark.

Different strokes (get it?!) for different folks. We each get to create our own passion graph and plan our bimodal spending accordingly.

Bimodal Spending in Everyday Life

Even down in the “bare necessities” categories (food, housing, etc.), I’ve found that bimodal spending helps me feel more fulfilled.

Cars: I don’t love cars. I don’t want or need an expensive car. I want to spend as little on cars as I’m able (here’s the Best Interest’s breakdown of car expenses). I plan to drive my Toyota into the ground and then continue to pay for efficient function over form.

Groceries: I love cooking and baking for people. I want to spend extra money to make sure my pizza has the highest-quality cheese. I want to spend money on imported vanilla extract.

But for most meals, I’m spartan. All I need for breakfast are a couple eggs and a slice of toast. 95% of my meals are simple. 5% are extravagant. That’s mostly no and a little hell yes!

My laptop: This example is meta. I’m writing this post on a 5-year-old HP laptop whose cooling fan sounds like a weed-eater. RNGGG-RRNNGGG.

It’s a $250 model that’s way past its prime. But the Best Interest is certainly one of my passions. To support the blog—and soon-to-be the Best Interest Podcast!—I’ve been saving up for a new MacBook.

I’ve waited and waited on buying a new laptop because I didn’t have a hell yes! reason to spend that much money. But now I do! I’ve been budgeting for the laptop for a few months, and now it’s time to pull the trigger.

Dining Out: My girlfriend loves dining out. And I certainly enjoy it too. We’ve started saving our dining-out dollars for hell yes! dining experiences (COVID notwithstanding).

We forgo a few “average” dining-out experiences and save those dollars for unique and memorable experiences.

I’ve had my fair share of $10 burgers. They’re great. But I’d rather save my dollars to widen my palate’s horizons. It’s a quality over quantity decision.

The Second Peak

Is bimodal spending such a cool concept that it will take over the personal finance blogosphere? Or will it fade like a wispy cloud lost in the Andes Mountains?

If you enjoyed this article, share it! There are easy sharing links below.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!