I’ve asked financial experts how they budget. This article breaks down their strategies. You’ll see tons of commonality between their budget basics.

I track every single dollar in my budget. But that method might not work for you. I’ve tried to get friends, family, coworkers to use the methods I use…they all felt it was a bit too hands-on and complicated. Maybe I should listen to them?

- Here’s my 2019 Budget

- And here’s my 2020 Budget

So I put up my Bat Signal and asked other financial writers about their budgeting habits. They responded! Let’s dig into their budget basics.

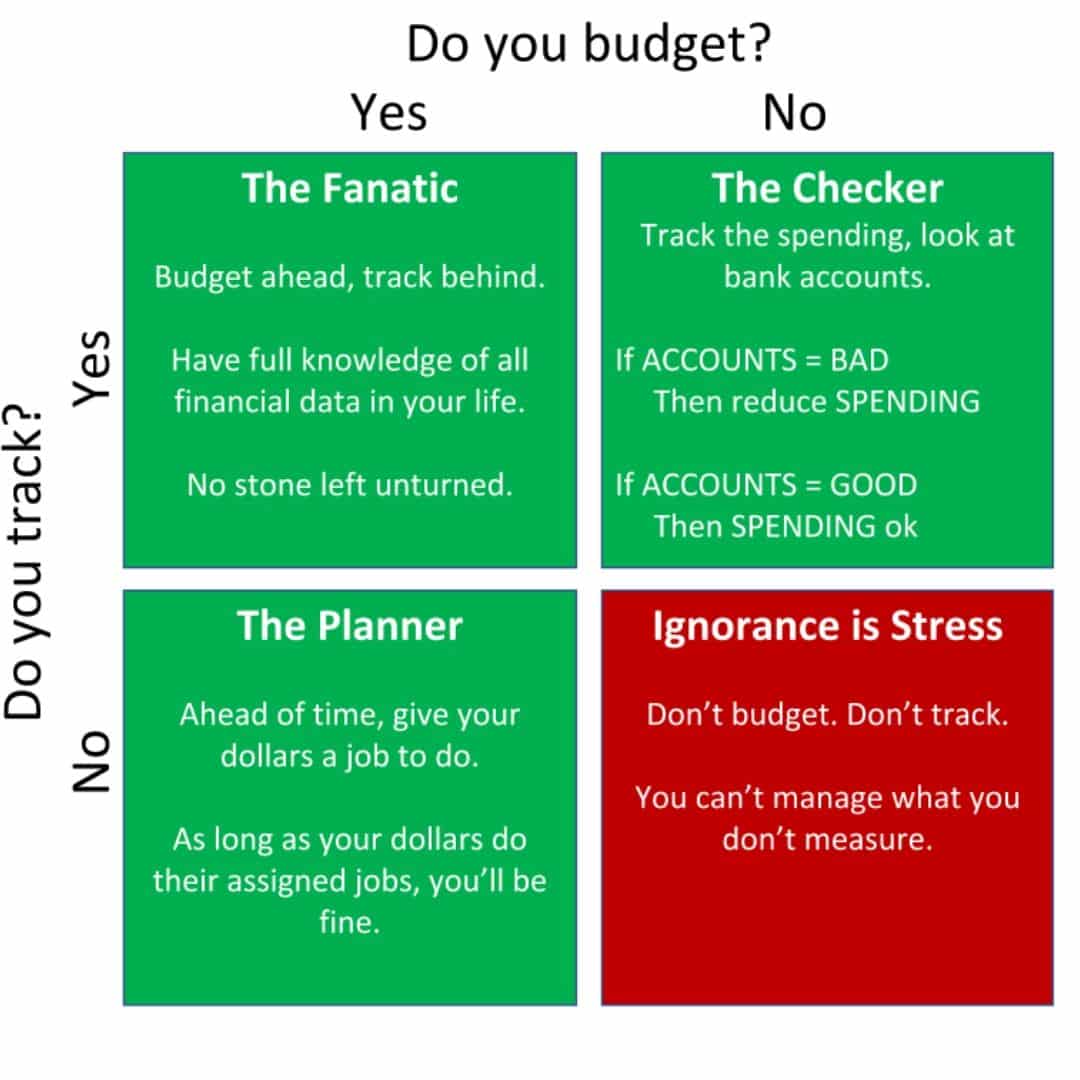

Budgeting vs. Tracking: The Two Budget Basics

There are two main behaviors I’ll refer to from here on out: budgeting and tracking.

Budgeting is the process of setting limits on your spending. Typically, it’s done via categories, or giving specific dollars a “job” to do.

Jesse took $200 from his recent paycheck and budgeted it towards next month’s groceries.

Tracking is the process of recording purchases and expenses.

After the trip to Wegmans, Jesse tracked the $70 receipt. Combined with his other shopping trips, he’d spent $225 on groceries this month.

While I get into this level of detail in my budget—specific expenses in specific categories, every time I spend money—I learned that I’m an outlier!

This isn’t how most experts budget. Instead, most other people use far simpler methods of budgeting and tracking.

As you’ll see below, some folks budget, but don’t track. Other folks track but don’t budget. Many people do both but do so infrequently (every month or so). Those are the budget basics.

Plan the Work: Budget, but Don’t Track

This first of the budget basics involves planning ahead but not double-checking your spending after the fact.

A Dime Saved blog uses the “Envelope system” to budget without any tracking. In its original form, the Envelope system literally involved placing cash bills into different labeled envelopes.

Need groceries? Grab cash from the Grocery envelope.

Trip to the movies? Grab a $20 from the Fun envelope.

No money left in the Dining Out envelope? Then you can’t dine out. There’s no funding for it!

That’s exactly why the Envelope system works without tracking. You can’t overspend a category, because you simply won’t have money in that envelope to spend. Or, as A Dime Saved describes it, “It’s pretty much all on auto-pilot.”

Nowadays, the Envelope system is frequently utilized in electronic budgets. I use it via the YNAB app. However, since it’s digital, the YNAB envelopes aren’t physically real and aren’t filled with actual cash. That’s when Budgeting with Tracking systems makes sense.

The Envelope System is one of the budget basics.

Data Fanatics: Budgeting + Tracking

A lot of the bloggers I spoke with described their use of long-term budgets with follow-up tracking. This is what I do, too.

Capture the big data, don’t sweat the details. It’s a great example of Pareto thinking. Do 10% of the work, but still get 90% of the results. I like that efficiency.

Mr. SR at Semi-Retire Plan plans his budget verbally twice per month with his partner, and then compares weekly spending against that budget. It lets them “work towards [their] saving goals [and] get the benefit to [their] marriage of being on the same page for the following two weeks.”

The Keeping Up with the Bulls blog and Marc from Vital Dollar both use spreadsheets to rough out monthly budgets, and then compare their end-of-month bank accounts against what they’d budgeted. Budget conservatively, then track one time per month to make sure you’re keeping lifestyle inflation in check.

I use YNAB, and so does Natalie from Go from Broke. YNAB works tremendously well, but also asks more of its users than most other systems.

Like other envelope systems, Natalie points out that YNAB suggests you “only budget what you have, not what you expect.” Importantly, the YNAB interface makes it easy to ask yourself “what does this money need to do before I get paid again?”

Enjoying this article? Subscribe below to get new articles emailed straight to your inbox

Tracking, no Budgeting

The thought process behind “tracking only” is simple:

Budgeting is predictive and therefore far less important than tracking your total amount of actual spending. Total spending, when compared to your total income, gives you all the data you need to make informed decisions.

I heard this theme over and over from this “Trackers only” budget basics group. In this case, the budget basics don’t involve budgeting at all!

“The Poor Swiss” says, “I found out over the years that the limits in themselves were not as useful as tracking expenses.”

The limits, in this case, are the amounts you set in your budget. The budget, by definition, is a hypothetical limit that you place on yourself. Whether you’re over, under, or right on target…that only depends on your actual spending behavior. And tracking is what records that actual spending behavior.

In other words, tracking is the most important of the budget basics.

Kevin at Just Start Investing operates on a similar system. He tracks his spending once per month. Kevin writes, “I keep a rough pulse on my spending and know if I need to reign it back a little to make sure I am hitting an appropriate savings number.”

No micromanaging to the point of frustration. Just an occasional course check, readjusting as needed. Hands-off is simple—budget basics.

I’d paraphrase Andrew at Wealthy Nickel, but his explanation of his family’s monthly tracking system is succinct and on-point. He writes:

“If you’re living paycheck to paycheck, I think our budgeting system would be too lax, but it works for us and our situation perfectly. We are at the stage where we have ingrained frugal habits and live below our means, so I am more interested in making sure our overall expenses stay in line and our savings rate and net worth keep going up.”

Well said, Andrew!

Ask yourself: if you or your significant other lost their job, would you be able to pay the mortgage, cover the bills, put food on the table?

If not, there might be some extra spending in your budget that’s dragging you into the “Two Income Trap.” Be careful with your budget basics!

Ignorance is Bliss: No Budget, No Tracking

Nobody (!!) I spoke with falls into this category. The budget basics implore you to at least have a budget.

Every respondent used some form of budgeting or tracking. Every. Single. One. Ignorance is not bliss, it’s stress!

That might be the most important takeaway from this entire post. These financial experts all find that budgeting and/or tracking should be used as a consistent benchmark to inform future spending.

As I mentioned weeks ago, one of the largest sources of financial unhappiness is not knowing your financial status. It’s that simple.

The act of informing yourself—via budgeting or tracking—will likely shed light on the dark corners of your financial life. And that light provides a new perspective, one that can be acted upon. You have to do something. That’s the simplest advice of all budget basics.

Once you know where you are in the world, you’ll feel less confused and more content.

I hope you learned something useful, applicable, to your lives. If this is how experts budget, maybe I should incorporate these ideas too? What do you think?

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

Pingback: Temet Nosce: know yourself. Learn and re-wire your "BUY THAT!" brain

Pingback: Adherence: give yourself a chance to actually stick to your new habits

Pingback: A Real Life Example of a Budget - Just Start Investing

Pingback: Personal Finance Unknowns - The Best Interest - It's what you don't know...

Pingback: A Wintry Emergency Fund Anecdote - The Best Interest

Pingback: What's Next? - The Best Interest - Future steps, one day at a time

Pingback: A Lot Can Change in Ten Years - The Best Interest - Long Term Thinking

Pingback: Personal finance and mental health in 2020 - The Best Interest

Pingback: How Experts Budget: The Best Interest Budget Survey - The Global Centre for Risk and Innovation

Comments are closed.