I started the Best Interest in mid-December 2018. It’s been a year! And this also marks one year since I’ve been tracking every single expense in my budget. E-v-e-r-y-t-h-i-n-g. So today I’ll share a few fun stories and lessons from Year One of the Best Interest.

Thank you!

A huge, huge thank you to everyone reading. I don’t write here because of the financial gain–it’s non-existent. I write here because you’re reading and because writing is fun.

Sharing freely with you is completely worthwhile. And you sharing your attention with me is a privilege that I don’t take for granted.

Every small compliment you’ve given me is extremely meaningful. I love answering your questions, your Tweets, your Reddit comments.

Some Stats

My first “full month” had 99 readers stop by. I was ecstatic! The past three months have had 3000, 4000, and 5000 readers, respectively. I’m 30x, 40x, and 50x as ecstatic. And with that rate of growth, I should pass the billion reader point around September 2021. Can someone involved in a pyramid scheme please check my math?

If you’re anything like me, the thought of writing a book seems daunting. It’s what those other people are capable of; not me. How the heck does someone sit down and put together 200 pages of coherent thought? I recently ran an audit on the Best Interest, and I just surpassed 50,000 written words…which is about the equivalent of 200 printed pages. Turns out, a lot of our limitations are self-imposed.

On Writing and Blogging

I think I’ve learned to be a better writer and better teacher. Writer’s block is a real thing. Alternatively, when a few thousand words just flow from a single brainstorm–magnifico! I’m still batting about .300 on my jokes. At least that’s consistent.

I’ve learned a lot about the logistics of blogging. Getting traction is tough, especially when there are literally thousands of people writing about identical personal finance topics. The supply of personal finance content is overwhelming. So the demand for any specific content–i.e. my writing–is low.

But that’s an awesome life lesson. Having a skill is fine, but what does the demand for your skill look like? Are you bringing something unique to the table? If you don’t love it for it’s own sake, then it might become a drag when you don’t find fame and fortune.

Spreading the word…

I’m proud that my writing and content is highly regarded. Those of you offering to give back to me–it’s an honor!

If you want to help, just share my blog with people you know. There is a cost: attention. But if you think my writing is worthy of someone else’s attention, I’d love it if you shared it with them.

Post a link on Facebook. Send your Uncle Dave the article I wrote about him. If you found a post particularly useful, let your tribe know about it. Simple grassroots sharing. That’s all I’ll ask, and I’d be so appreciative.

I don’t make many special efforts to cater to Lord Google, and that’s one place where I’m left behind. Many other blogs do a great job molding their blog specifically so that Google’s ranking system lists them highly. For the uninitiated, this is called “SEO,” or search engine optimization. Then, people who use Google (know any of them?) are most likely to find those blogs. I’m dipping my toe into learning SEO, but I’ve got room to grow!

For a while, I was serving ads on the blog, spamming you with images of tapeworms and “Doctors COULDN’T BELIEVE when the healthy dog showed up with THIS.” Oh my god, Fido!? Better click!

But once I realized I was earning only 20 cents a month via your advertising torture, I decided to stop. Bad investment. So I implemented the Best Books. These books contain lessons that out-value their sticker price. There’s no fee to you beyond the normal price. Each purchase nets me between 30 cents and a dollar per book, and it’s something I stand behind 100%. Or even better, see if your local library has a copy. Everybody wins, except Big Tapeworm Pharma.

A Year of Budgeting

As I mentioned in the opening, I started a hardcore budgeting habit one year ago. I use the app YNAB–I can’t recommend it enough (know anyone looking for budgeting software for Christmas?!).

Note: you and I both get a free month of YNAB if you end up signing yourself (or someone else) up with the link above. No extra cost to anyone involved. You get a 34-day trial, and then an additional free month. That’s two months to figure out if you like it!

I know exactly where my money is going, and I know exactly where I can focus my effort to make the biggest changes. I know how much I’m spending on lattes, Chipotle, and avocado toast. P.S. it’s not going to make a big difference, Suze Orman.

Has this level of detail been overkill? Quite possibly. I wrote an in-depth post about how other financial writers operate their budget. My system is skewed towards “way too detailed.” Many people get similar results with less effort. But my system allows me to give the following analysis with absolute confidence.

Here, in order of significance, are my biggest expenditures in 2019:

| Category of spending (note: these are my subjective category titles) | Percent of total spending |

| Mortgage, insurance, property tax | 35.8 |

| Groceries | 8.9 |

| Generic Fun Money | 6.7 |

| Vacation | 5.6 |

| All Misc. Items (too small for own category) | 5.2 |

| Utilities | 5.2 |

| Restaurants/Bars | 5.0 |

| Friend’s Wedding (1) | 4.8 |

| Medical | 3.6 |

| Gasoline | 3.4 |

| Home Maintenance and Interior Design | 3.2 |

| Gifts | 2.5 |

| Auto Maintenance | 2.5 |

| Subscription services | 2.3 |

| Charity | 1.7 |

| Car Insurance | 1.6 |

| Hiking Gear | 0.9 |

| Friend’s Wedding (2) | 0.6 |

| Internet | 0.4 |

| Clothing | 0.3 |

What’s missing? For starters, savings! I consider the money I save separately from the money I spend. And taxes are missing too. Ugh.

Savings and Taxes

The financial blogosphere seems to create a…”measuring contest”…out of savings and savings rates. People enjoy reading articles like, “Here’s How I Saved $100K by age 15” just like they enjoy “Here’s How I Lost 400 Pounds.” CNBC, Forbes, MarketWatch…these sites have daily headlines about a someone living in their parents basement and becoming a millionaire at age 27. It makes for a good story!

A lot of my peers–many of whom I admire for the quality of their blogs–share monthly updates about how much money they have. On one hand, I totally get it: it’s a way to build trust with readers. “Not only am I talking about good financial habits, but look at how much money I’m making by walking the walk.”

But, it’s hard to share absolute money totals without some of the “feel bads.” I trust that the content of my writing stands on its own merit. I hope that by sharing the following relative figures, I’m getting the best of both worlds.

On average in 2019, I saved about $1.50 for every $1.00 I spent. That saving gets split between retirement, emergency fund, Health Savings Account, and my normal bank savings account. Like every white belt financial guru says, I pay myself first. It’s not a ton. I’m not going to retire next year. But I think that saving while young will pay off down the line. I’ll detail this a bit further down.

What else is missing from my breakdown? Taxes. The tax man is inevitable, so I’ve only looked at my net, or post-tax, dollars. If I were to include them, income taxes and other payroll deductions (social security, medical insurance, etc) would be 2.1x as impactful as my mortgage. Put another way: taxes would add an additional 75% onto the table. Gee whiz, Uncle Sam.

Enjoying this article? Subscribe below to get new articles emailed straight to your inbox

Measuring, then managing

I’ve quoted Peter Drucker many times on the Best Interest: “You can’t manage what you don’t measure.” That’s why I decided to start operating my budget so holistically. Via detailed measurement, I can implement better fiscal management.

What have I learned? If I sum up all the “fun” or “extra” expenses in 2019, it’s 23.7% of my total spending. Now, having fun is…well, fun. That’s the point! I don’t really want to decrease that spending, because I enjoyed it all. I still think I’m on the good side of the Fulfillment Curve. But I do realize that an opportunity exists. If push comes to shove, I can rein in that Fun spending considerably.

Another great outcome: I now have clean data to use for future budgeting. How much should I plan for next summer’s weddings? How much should I earmark for gas, Christmas gifts, quick fixes around the house? I thought I was spending 3x more on Groceries than on Dining Out, but turns out it’s only about 1.8x more. There’s a lot of useful information I can take from the past year’s data and apply to the future.

Another interesting factoid: my month-to-month spending variation was way higher than I thought it would be. My “highest” month saw 70% more spending than my “lowest” month. A single, fixed budget would not have worked for me. The flexibility of the YNAB software allowed me to roll with the punches and re-allocate money where I needed it.

Compounding in action

Everyone, it seems–from Albert Einstein to Warren Buffett–beats the drum of compound interest and compound returns. If you need another reason to hop on board the Compound Train, I’ve got my own anecdotal data.

When I started writing last December, the S&P 500 immediately took a quick 11% drop from $2650 to $2350. Coincidence?! Umm…yes. Absolutely. But the S&P has since climbed 18.5% from where it was before that drop–from $2650 up to $3140.

The power of compounding is that all my retirement savings saw that increase. The money I saved in 2012 went up 18.5%. Same goes for my 2013 contributions, 2014, and every year since. And yes, the money that I stowed away in 2019 also benefited from this bull market. Every dollar, regardless of when I invested it, saw a positive return in 2019.

Save money, get money

I’m saving money, and the stock market went up. Two separate ways in which my accounts increased. So how much impact did those two separate factors have in my retirement accounts?

About 60% of my 2019 retirement account increase is due to dollars that I saved in 2019. But the remaining 40% of my retirement account increase is due to gains on old investments.

That 40% is, in a way, free money. That’s the point–the goal–of investing. The small price I paid is that I decided not to spend that money during the past 7 years. Rather than using that money to buy stuff, I invested. And now my investments are paying me back.

Granted, I have not yet realized these investment gains. Not realized? It’s a fancy way of saying that my money is still tied up in the market. If the market crashes tomorrow–poof!–there goes my so-called profit. While I can write about the returns here, they’re somewhat imaginary until the day I decide to sell my investments and turn them back into cash. With cash in hand, the gains become real. They are realized.

Since I’m saving for retirement, I might not sell these investments for 20 or 30 years. Since I’m looking so far out into the future, I have no interest in realizing my gains today. To be honest, I don’t even really care that the investments went up this year. Whether they went up or down, it wouldn’t affect my goals or my behavior. I’d still be saving my money, slow and steady. Right now, I’m just trying to save, save, save.

Quick aside: compounding over time

If you’re a personal finance regular, you know this. But if not, strap in for some simple–but mind-blowing–math.

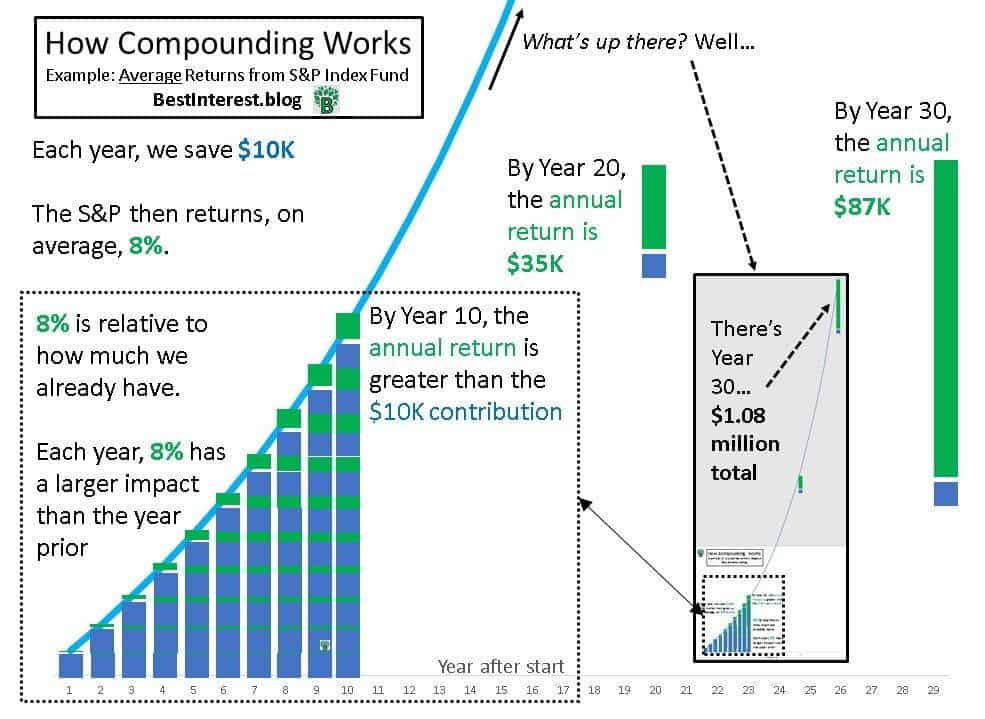

Over long time-spans, the “free money” from compound returns starts to vastly outweigh any individual contributions. Let’s look at a typical American worker–Franklin–as an example.

Simple numbers: Franklin has a 30 year career, saving $10,000 a year (probably in a 401(k) account), and sees a stable 8% annual market return. Everything except the stability of those returns is perfectly realistic.

In Year 1, Franklin contributes $10,000, and the market increase will “give” him an extra $400. 96.2% of that year’s increase is coming from Franklin’s pocket; 3.8% comes from market returns.

But by Year 5, Franklin’s account holds about $61000. He contributes his usual $10K, and the market returns an additional $4000. That’s pretty significant, right?

By Year 10, Franklin has $150K saved. He contributes his typical $10K, and the market returns…$10,800! The market returns are higher than Franklin’s own contributions! And it only accelerates from here.

The market doubles Franklin’s contributions in Year 15, triples them in Year 19, and quadruples them in Year 22. By the time Franklin retires (Year 30), the market is “giving” him $87,000 a year. Franklin has contributed a total of 30 * 10K = $300,000, but he retires with $1.08 million.

That’s compounding.

Right now, I’m still in the early years of Franklin’s curve. But it’s excited to see the early stages of the “acceleration” that speeds up over longer time spans.

If you feel like it’s too late for you the start down this savings path, I highly suggest reading this post. There’s still time, and you can do it.

What’s next? Another year?

I have no plans to stop writing any time soon. I really enjoy writing and sharing and interacting with you all.

Sometimes, the level of effort gets a little high. I’ve probably spent a few hundred hours on this blog project. Burnout is definitely a factor. My enthusiasm waxes and wanes. But overall, the good outweighs the bad.

I might try a couple small ways to make a few dollars, at least to offset the cost of operating a website. Sure, they’re mostly small costs. But losing money on a venture all about personal finance seems…confused. If I do start advertising, I’ll make sure to explain my rationale. I don’t want to violate the attention you so graciously give me.

As for budgeting…I’m so used to my budgeting habits that I don’t foresee changing them. I feel completely safe in my financial life. It’s hard to put a price tag on that, but the ~$80 yearly YNAB subscription is a very low price tag compared to the value it provides me.

Do you have any thoughts on the future of the Best Interest? I hope you’ll let me know. Thank you very much for your readership over this first year.

I hope you’ll keep coming back!

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

-Jesse Cramer

Pingback: A Lot Can Change in Ten Years - The Best Interest - Long Term Thinking