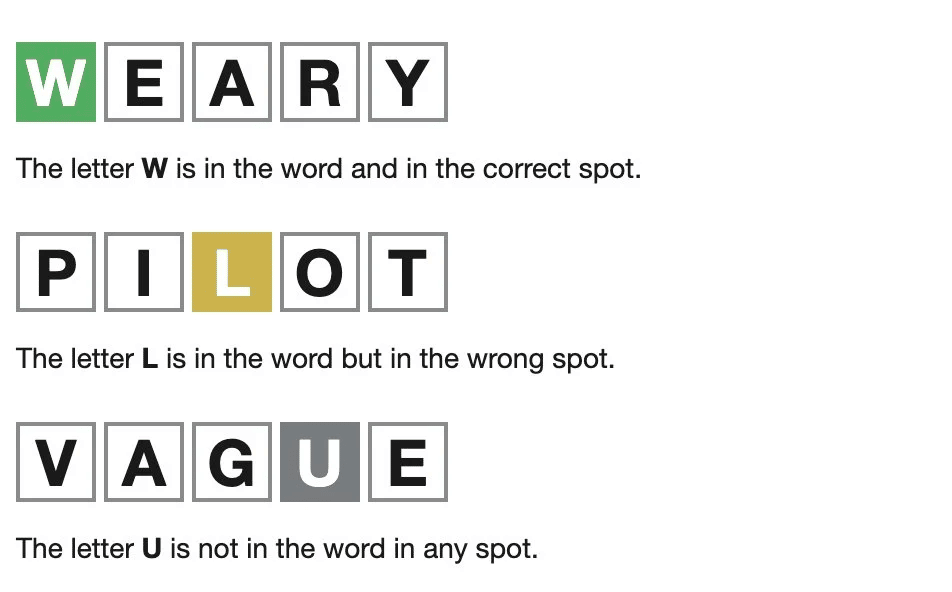

For you cave-dwellers, Wordle is a word-guessing game where you have six guesses to correctly find a 5-letter word. After each guess, you learn which letters you’ve guessed correctly and if you placed those letters in the right/wrong spot.

There are two competing Wordle strategies, and numerous variations balancing the two extremes:

- Win quickly at all costs. Find the word in as few guesses as possible.

- Take it slow and don’t lose. Ensure you find the word within your six guesses.

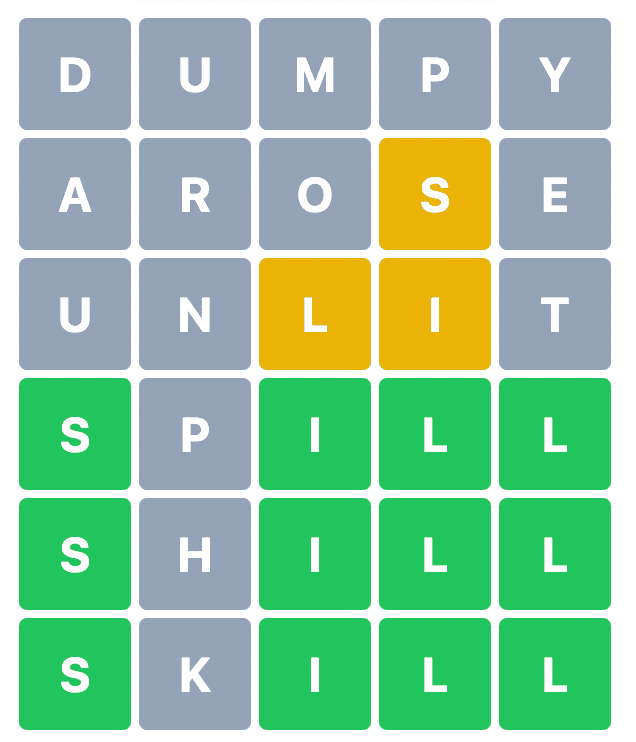

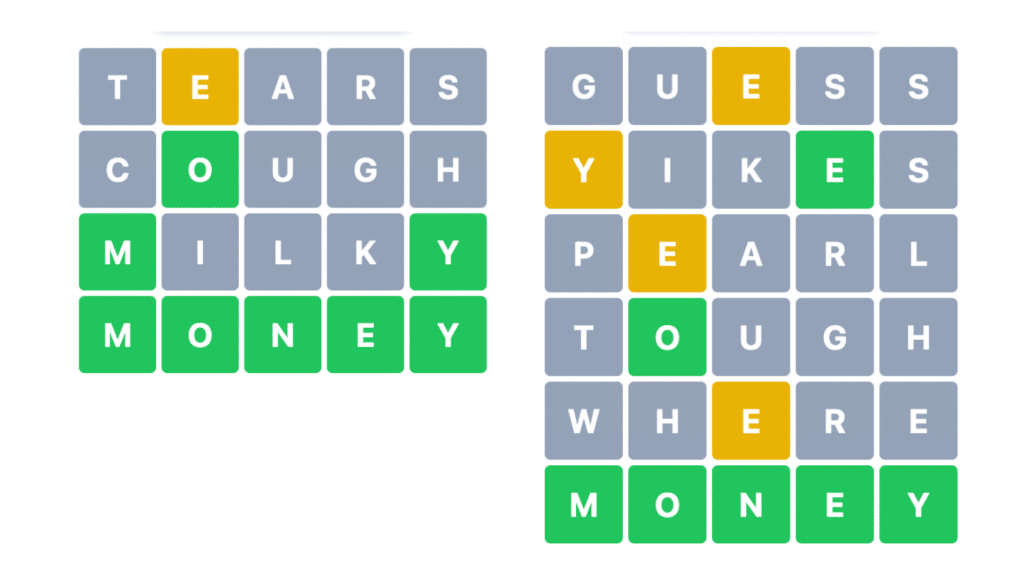

The first strategy is a sniper rifle, showing off your smarts and skill to hone in on the right answer. But it runs the risk of ruin. By not diversifying across the alphabet, you might hit the SPILL/SHILL/SKILL problem seen below and lose.

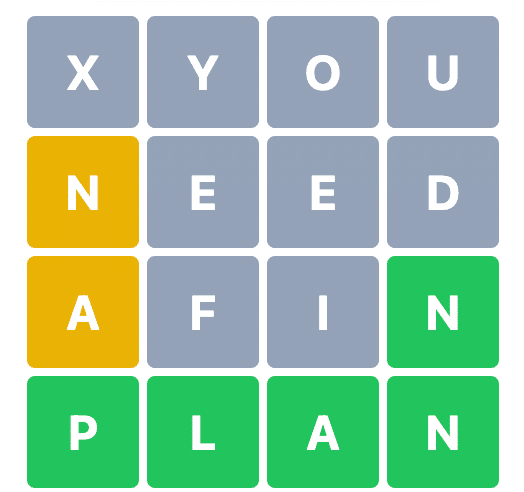

The second strategy is slower, but it also minimizes the chances you’ll ever lose the game (like above). Instead, this slow strategy aims to figure out all five letters (and probably which location a couple are in) with one or two guesses remaining.

The first strategy is upside maximization. The second strategy is downside minimization. Some Wordle players opt for a mix of the two.

Wordle is just a game. But problem-solving, whether in games or “real life,” is a universal skill.

Financial planning is one of my favorite “real life” puzzles, and each person’s circumstances are the pieces (and there are way more than 26 unique options). There are a multitude of “right” and “wrong” plans. Two plans can get you to the same destination, but the one that helps you sleep at night is better than the one giving you agita.

A good plan, ideally, accounts for both your specific circumstances and your unique goals.

Some people want to maximize. They want to earn as much money as possible, spend lavishly, and leave millions behind for their heirs or charity. They want to see how high the bar can go. But these “high-risk” plans have downsides too. Namely, they have a higher probability of failing to achieve their owner’s goals. They might SPILL/SHILL/SKILL their way to failure.

Other people prefer downside minimization. They want to hedge their bets wherever possible, ensuring the bar never falls below a preferred threshold. This plan can never attain the conceivable heights of a maximized plan, but that’s by design! In Wordle terms, their only goal is, “Don’t lose!”

Most people prefer a blend of the two.

In Wordle, you can stumble into the right word despite a bad strategy. Similarly, many financial plans “work,” despite being clearly suboptimal. The difference, of course, is that Wordle mistakes won’t cost you hundreds of thousands of dollars.

But if you make a mistake in financial planning, you might retire with $800,000 instead of $900,000. Or you might pay $20,000 in capital gains taxes instead of only $10,000. That’s consequential! You’ll survive in either case, but one option is strictly better than the other (unless you prefer having less money?).

I’ve embedded myself in personal finance for the past 4+ years and in professional financial planning for the last 13 months. One of my biggest takeaways from financial planning is that efficiency matters.

Some financial plans don’t work at all. Most financial plans work “just fine.” And some financial plans are beautifully efficient, looking for dollars – earned or saved – in every nook and cranny of your financial life. A percent here, a few tenths there…it really starts to add up.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!