We can solve the student loan debt crisis. We need a student loan proposal that offers assistance with the interest payments. The math is simple.

Principal vs. Interest

I’m not going to suggest that we forgive the principal of student loan. If I borrow $20 from you, I’ll pay you back.

However, the principal—the $20—is not the problem with student loans. The problem is the interest–or, as I’ve described it before, debt’s “silent assassination technique.”

People are paying thousands of dollars per month against their loans, but sometimes less than 10% goes towards their principal. The rest pays off interest. That’s an issue, and my student loan proposal offers a solution.

If someone is $100K in debt at 5% annual interest, their minimum payment is $407 per month. That minimum will pay off the monthly interest and zero principal. They’re treading water. No progress. They drown in interest if they pay any less.

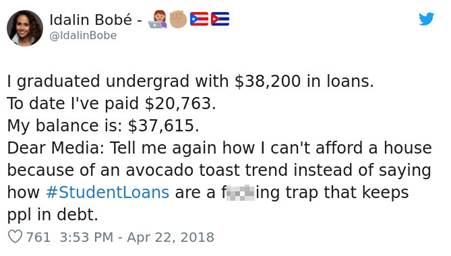

This is what Ms. Bobé describes in her Tweet, above. $20,000 in payments, but only a $600 decrease in her principal. I’d drop an F-bomb, too.

Can we simply “forgive” all interest? Some moral codes would say it’s the right thing to do. But I worry that it’s too drastic, leading to further complications. It will only pass the buck. We rather have people lift themselves up by their bootstraps. But first they need boots.

So this student loan proposal offers them a hand, then lets them do the rest. A government assistance program to help pay the interest on student loans could work. If the individual addresses the principal, then government (our tax dollars) can help pay interest.

But that’s a free handout?!

Did Jesse just propose free government handouts?! Perhaps you haven’t been paying attention to the COVID-19 pandemic, but the government can pass out handouts if circumstances required them.

Related articles about COVID-19:

- Ayy Corona! The Stock Market and Coronavirus

- Viral Stock Market Strategies

- The Biggest Lesson from COVID-19

You might be diametrically opposed to such a solution. There are plenty of valid arguments against what I’m suggesting.

But keep in mind, the government is already helping certain groups of borrowers in very similar ways. Programs such as PAYE, REPAYE, IBR, ICR, and PSLF all help certain classes of workers repay their loans. It’s a good start, but these programs are limited in breadth.

This student loan proposal would open up avenues of assistance to all borrowers. We can even create economic incentives that encourage people to pay more towards their loans. The larger percentage of their income that they put towards the loan, the more interest Uncle Sam will pick up.

- This will save the individual money. They pay less interest.

- This will save the government money. If the loan is repaid sooner, less interest will accrue. Less interest = less help from Uncle Sam. The math works out.

It’s a win-win.

Student Loan Proposal Math Time

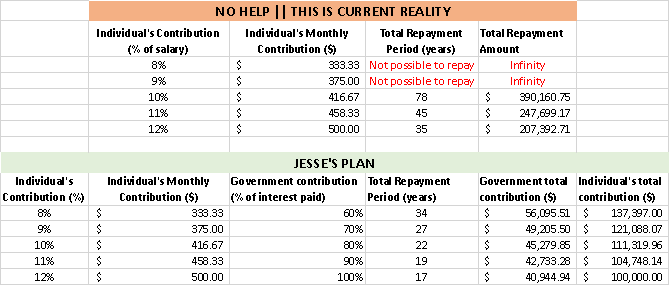

Let’s look at an example graduate. This person earns a $50K salary (assume no raises ever, to keep it simple), but is $100K in debt. Their debt has a 5% interest rate. You know this person. She’s a teacher, or a nurse, or the guy in the office who’s great at spreadsheets. It’s a normal person, and this level of debt is a normal situation. Remember this loan: $100K in debt, 5% interest rate, at a $50K salary.

If this person “only” puts 8% of their salary ($333 per month) towards their loan in today’s paradigm, they will drown in debt. No hope, no end in sight. Forever. Is that a system we want to maintain? Is that reasonable, or moral? I don’t think so, and I want this student loan proposal to fix that.

If this person repays their loans using 10% of their salary—$417/month—they will end up paying a total of $390K over 78 years. That is crazy.

So, let’s apply my student loan proposal. A person paying that same 10% of their salary in my proposal would get 80% of their monthly interest covered. Reminder: that’s what this student loan proposal is all about. It helps the debtor with their interest payments.

By helping with the interest, this particular loan would be paid off in 22 years, using $111K of the individual’s funds and $45K from the government.

That’s a difference of $233K ($390K vs. $111K + $45K) and 56 years (78 vs. 22) of payments. How is this stark difference possible? Because interest is the killer. If we help with interest, then repayment becomes attainable.

And in this student loan proposal, the individual is incentivized to pay more if they’re able. If they contribute 12% of their salary—$500/month—then the government covers all interest payments. This particular loan would be repaid in 17 years, using $100K from the individual and $41K from the government. Both the individual and the government save money when the individual pays more.

Paying off this article

The actual numbers and percentages can be massaged. More strict, more lenient…I’m open to ideas. There are plenty of creative ways to pay off student loans.

The simple truth is: this wave of loan interest is crashing over normal people with normal salaries, sweeping them out 40 years into their lives with no life raft.

If we help with the interest, we give them a port in this storm. Isn’t that worth doing?

If you enjoyed this article and want to read more, I’d suggest checking out my Archive or Subscribing to get future articles emailed to your inbox.

This article—just like every other—is supported by readers like you.

Pingback: In the long run, what's the cost of debt? For some, it's opportunity missed...

Pingback: Personal Finance Unknowns - The Best Interest - It's what you don't know...

This proposal presents a promising solution to the student loan crisis. By introducing Income Share Agreements and holding colleges accountable for affordability, it offers a progressive approach to tackling this systemic issue. Kudos to the author for advocating for meaningful change!