TJ works for a blue-collar manufacturing company. He recently told me how his coworkers are buying GameStop call options on Robin Hood. But when asked, “What exactly is a call option?” They respond:

Well…it’s an investment. You know…it’s an option. It’s like buying the stock but for less money. It’s…it’s investing.

Ok. They have no idea. Just like many other Robin Hood investors.

They are canaries in the coal mine. They are shoe shines handing out stock picks. The markets are clearly frothy.

But I want to focus on a different problem.

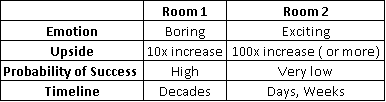

Behind Door Number 1…

You’re presented with two doors.

The first leads to a room of long-term investing. That room contains your 401(k), some index funds, a set-and-forget cadence. It’s a boring room. But it promises—with fairly high certainty—to turn today’s $100 into $1000 over the course of 30 years.

The second door leads to a gambling hall. Flashing lights and hollers of success. “Big money!” This room contains Robin Hood options trading and cryptocurrency. It’s an exciting room! It makes no promises other than a possibility of turning today’s $100 into tomorrow’s $10,000.

How do you convince someone to enter Room 1 over Room 2?

- Room 1 appeals to safety.

- Room 1 appeals to probability-minded people. A 90% chance of a 10-fold increase is significantly better on average than a 1% chance of a 100-fold increase.

- Room 1 appeals to those already in good positions. If I can guarantee my long-term success, that’s good enough.

To quote William Bernstein:

The purpose of investing is not to simply optimize returns and make yourself rich. The purpose is not to die poor.

William Bernstein

A guarantee of not dying poor is good enough—no need to chase near-term, high-risk bets.

But who chooses to go into Room 2?

- Room 2 appeals to risk-seekers. We know humans can be poor at assessing risk.

- Room 2 also appeals when long-term thinking is difficult. Humans are good at thinking about this week, this month, this year. We’re bad at thinking 10+ years ahead.

- Finally, Room 2 appeals to people who feel that Room 1 simply can’t get them unstuck. People in bad financial shape and no hope for progress. People without sufficient income to make Room 1 successful.

Enjoying this article? Subscribe below to get new articles emailed straight to your inbox

$20/Hour – Room 1 or Room 2?

Let’s imagine a wage worker. They make $20 per hour, $40,000 per year. After taxes and living expenses, what do they have leftover?

Let’s say $50 per week. $800 in wages less $150 in taxes and $600 in expenses. $50 leftover.

Next, let’s imagine this worker is “perfectly indexed.” They utilize a Room 1 index fund buy-and-hold strategy.

If this worker saves $50 per week from age 22 to age 62 and invests in an S&P index fund (with historical, inflation-adjusted average returns of 7% per year), they’ll end up with $575,000 at retirement.

Using the 4% rule, a $575,000 nest egg translates to $23,000 of retirement income per year or about $2000 per month. A simple Social Security estimate tacks on another $1000 per month.

$3000 per month is safe to retire on in many regions of the U.S. Not extravagant, but comfortable. That’s good enough. That’s the prize for 40-years of diligent, smart investing.

What if 30 Years, Not 40 Years?

But what if our worker starts savings at 32 instead of 22? It shortens their investment timeline from 40 years to 30 years.

This second, less-perfect worker will end up with a nest egg of $275,000, which will pay them roughly $900 per month in retirement. Even adding another $1000 for Social Security, this is not enough to retire on in most of the U.S.

30 years of investing in Room 1 did not lead this second worker to the promised land. They cannot retire at age 62.

Back to Age 32

Since Room 1 failed us, let’s backtrack to age 32 again.

We know where Room 1 leads this 32-year old. It leads to the “smart” choice, the “safe” choice…but the choice that fails to achieve an “on-time” retirement. It leads to 30 years of solid investing, guaranteed returns (hey…it’s my hypothetical), but ultimately to a lack of funding at retirement. All the right moves, except for the results.

So doesn’t it make sense that a worker would say, “Screw it, let’s pick Room 2. Maybe my $50 will become $5000 in a week, and then I can make progress in my financial life.”

It’s simple game theory. You play to your outs. If Room 1 fails no matter what, then you take your chances on Room 2, even if it’s a long shot.

This is the same trap set by lotto tickets. We all know lotto tickets are losing propositions. Then who actually buys lotto tickets?

A 2018 Bankrate survey (note: take surveys at face value) found that people who earn less than $30,000 per year spend, on average, $412 per year on lotto tickets. People who earn $75,000 or more per year spend, on average, $105 per year on lotto tickets.

Why would poor people choose to “waste” money on lotto tickets? Money that ought to be more precious to them?

It’s because lotto tickets present a sliver of hope.

Low-earners avoid Room 1 for the reasons we’ve already discussed. They don’t have the amount of money to make Room 1 successful—they’ll die poor despite any Room 1 benefits. Room 1 is a guaranteed loss.

Why not YOLO into Room 2? They are playing to their outs.

High-earners put their money into Room 1 opportunities. They know Room 1 will guarantee their long-term success, and they know Room 2 is a trap. Room 1 guarantees they “won’t die poor.”

The same can’t be said for low-income earners.

Lotto Tickets and WallStreetBets

The same “lottery mindset” is happening with the WallStreetBets (WSB) phenomenon (e.g., the GameStop short squeeze).

It’s like Charlie and the Chocolate Factory. People waste money on long-shot bets believing they’ll be Charlie Bucket and find a Golden Ticket (we’re all our own protagonists, after all).

Yes, I know many WSBers are white-collar tech bros with too much money for their own good. “This $40K is burning a hole in my pocket…might as well buy GameStop calls.” I’m not discounting that cohort.

But when those $40K-turned-$4 million stories are brought to light, the subsequent headlines trigger the same Room 2 instincts as the lottery. It’s seen as a sliver of hope, a way out.

There are real anecdotes from my experience where lower-middle-class workers are scrounging for extra money to pour into exotic WallStreetBets investments. When pressed for details, they are clueless about the underlying mechanisms.

What’s a put? What’s a call? What’s a stock? What’s a dividend? They have no answers, but their ignorance is irrelevant to them. They are “unsophisticated,” but they don’t care. The mechanisms of the investments are peripheral at best.

The material fact is that the outcome of a successful options trade is the same as a winning lotto ticket. That’s all the matters.

That chance to win big presents a sliver of hope that these people do not see in boring Room 1.

Haven’t I Seen This Movie?

This story possesses shades of J.D. Vance’s book/movie Hillbilly Elegy.

One way our upper class can promote upward mobility, then, is not only by pushing wise public policies but by opening their hearts and minds to the newcomers who don’t quite belong.

J.D. Vance

Index funds have democratized investing like nothing else. Any Average Joe or Jane can, for almost no cost and with no prior knowledge, intelligently invest their capital in the best companies in the world. Index funds opened that door.

But there continues to be a barrier to entry in financial education and investing education. It barricades newcomers into thinking that these topics are too complex for them to understand or employ.

Breaking that barrier is my driving force.

But there’s a second barrier that I’ve already described: pure lack of income.

Break The Mold? Help the Old?

Is it a problem that people feel hopeless about Room 1? The question quickly gets political. Room 1 exists to enable retirement. That’s why 401(k)s were created. So the answer boils down to, “do low-income workers deserve to retire?”

As Morgan Housel points out in The Psychology of Money, retirement is a fairly new concept. Most people 150 years ago didn’t have any plans on retiring. You worked until you died.

But after the Industrial Revolution, the combination of 1) growing societal wealth, 2) longer lifespans, and 3) the disinterest in having old, slow people work on the assembly line led to a push towards retiring old workers.

Yes, it’s callous to think that way (factories retiring workers like rusty machines vs. humans consciously choosing to retire). But it’s the truth. Regardless of the origin, retirement is now a norm.

Social Security was created to help integrate this norm. But as we calculated above, Social Security clearly isn’t enough to retire on. How do we close that “gap” to a safe retirement? There’s a balance to strike.

If I opine that “all people deserve to retire,” some of you will respond:

“There’s no way I’m going to support retirement for someone who screwed off for 25 years while I was busting my ass. They made their bed, now they gotta sleep in it.”

I get it! I’ve written before about the moral questions and unintended consequences surrounding free handouts.

But if I suggest the opposite—e.g. that retirement is “a privilege, not a right”—then how do we address the mounting elderly poverty problems in the U.S.?

- 21% of married Social Security recipients and 43% of single recipients aged 65+ depend on Social Security for 90% or more of their income.

- “These older adults struggle with rising housing and health care bills, inadequate nutrition, lack of access to transportation, diminished savings, and job loss.”

- Source

We have to choose. Where do we want to steer this ship? We’re about to face a wave of retiring baby boomers. We, as a society, get to choose how we help them (or not).

Personally, I do think it’s a problem that many workers either 1) don’t understand the benefit of Room 1, or 2) didn’t learn about Room 1 early enough in their lives, or that 3) they do understand the benefits of Room 1 but don’t have the funds to take advantage.

Two solutions seem obvious:

- Better financial education. That’s why I write on the Best Interest. And why I have plans in the works to bring that message to more people who need to hear it. We need to financially educate more people and need to do so earlier.

- “Reinvigorate the middle class,” i.e., balance wage distributions. This is how Room 1 becomes a feasible path for Average Joe. He’s got to earn more money for his efforts.

A two-pronged attack. Education and earnings. We need to teach people that there’s a way out of their “learned helplessness” while simultaneously making said improvement easier to secure on their own.

Psychologists call it “learned helplessness” when a person believes, as I did during my youth, that the choices I made had no effect on the outcomes in my life.

J.D. Vance

There’s a “pay now or pay later” trade-off. Do we support better financial education now? Do we support higher wages now? Or do we kick the can down the road, only solving the growing problem of impoverished old people when it’s too abhorant to stare at any longer?

Some of you might rightly be thinking, “Isn’t it too late to educate Baby Boomers to ‘save themselves?'”

Probably. We might have missed our chance at preventative medicine there. We’ll have to rely on more expensive reactive medicine instead. The next 20 years will be a litmus test on our society’s humanity.

How a society treats its most vulnerable – whether children, the infirm or the elderly – is always the measure of its humanity.

Matthew Rycroft

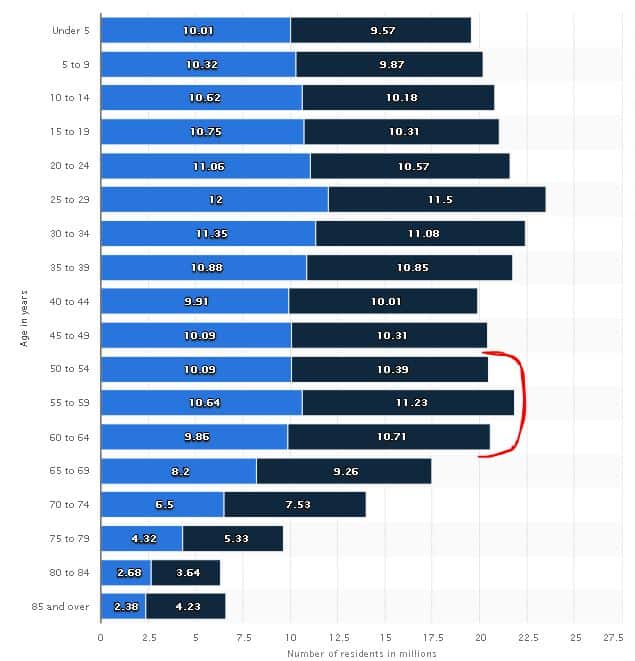

But for the next generation, the opportunity to for “preventative medicine” is there. If you scroll back to the demographic plot, there’s a huge cohort less than 30 years old. Who has their best interest (!!!) in mind?

Best Interest co-founder Ben Franklin once wrote:

An ounce of prevention is worth a pound of cure

Ben Franklin

Education provides solutions to past mistakes. It prevents people from missing the boat on their Room 1 opportunity. It enlightens people on the risk of WallStreetBets and the losing proposition of the lottery.

That’s why “investing in knowledge pays the best interest.”

“We are the Dreamer of Dreams!”

Perhaps it’s just a pipe dream, but I think education is a cost-effective way towards a better future.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

Great thoughts, it is ironic that the people who could afford to play with door 2 are the ones who avoid it while the ones who cannot afford to lose money are the ones most attracted to it. I have never found casinos fun, never bought a lottery ticket because I’m a math guy, an engineer like you. A negative sum game just doesn’t feel fun to me because I know I can’t beat it in the long run. Speculation feels just the same to me. Boring investments, on the other hand, are wonderful! And as a Boomer I’ve gotten to watch a 401K grow to over seven figures and other boring investments do the same thing because I have decades of experience at not touching them except to rebalance. I wasn’t as smart an investor as you are when I was your age but I knew just enough to do extremely well over time. And that came from being educated from several different sources. Keep up the good work!

Hey Steve, thanks again for writing in 🙂

It is an odd irony, isn’t it?

My lucky casino story. At a friend’s bachelor party, most guys went and played blackjack. Myself and TJ (the same one from this story) signed up for a casino card and got $15 in credit. We vowed to not put down any money ourselves.

We went off and played $1 slots until we ran out of money (or won so much that we’d walk away with a story)

TJ won $70. I was down to 4$ and then won more than $250 in one pull.

We both walked away with great stories and lucky profits.

But back to your point, I’m right there with ya on boring investments. Boring is ok with me 🙂

Good to hear from you again, talk soon.

-Jesse

Another great blog post. Education for the win!

Additional point for the “Room 2” even if you win with the 100 times your money if you keep making bets you could lose it as quickly as you gained it. I been a victim of being greedy and not pull my winnings off the gambling table. With individual picking of stock you got to be right twice. What to buy and when to sell?

Hey Tech! Thanks a bunch, really appreciate the kind words.

That’s totally true. Early success in Room 2 can be a curse in itself, tricking people to believing that they have true skill. Just like you said…it’s true in the real casino and also true in the casino of short-term investing.

This is an interesting topic that I have thought about. Financial Literacy is something that needs to be taught to school. It is something that currently needs to be spread around to our generation and the next. I have ran into many friends that are in the early 40s who have not started investing for their retirement. It is a point where they just don’t know, may be not care at this point, and are not worrying about it. So How do you help the poor? How do you help the middle class that may end up in retirement poor? These are the questions that I have been recently asking myself.

I am trying to do my best to educate through writing. I want to thank you for doing the same.

Hey Steve, I 100% agree with you. I’m glad you’re thinking about these ideas too.

Hope all is well in Taipei 🙂