Don’t miss an episode of our podcast, Personal Finance for Long-Term Investors. Available on all podcast players.

Here’s the latest episode:

Friend of the blog DT wrote in and said:

In regards to your recent “When to Take Social Security” article, you left something out. You can take Social Security early (say, age 62), then invest that money, and your investment will end up better than if you had waited on Social Security until age 67 or age 70.

Interesting! But does the math work? Let’s dive in. Should you take Social Security early and invest it?

What Kind of “Returns” Do You Get For Waiting on Social Security?

Let’s start by looking at Social Security. What kind of “return on investment” do you receive by delaying your Social Security decision?

There’s no easy way to do this today without a spreadsheet, so we will use this Google Sheet to show you some math. (I keep the original file pristine so all readers see the same numbers, but you can go to File –> Make a Copy to create your own copy of the file to play around with.)

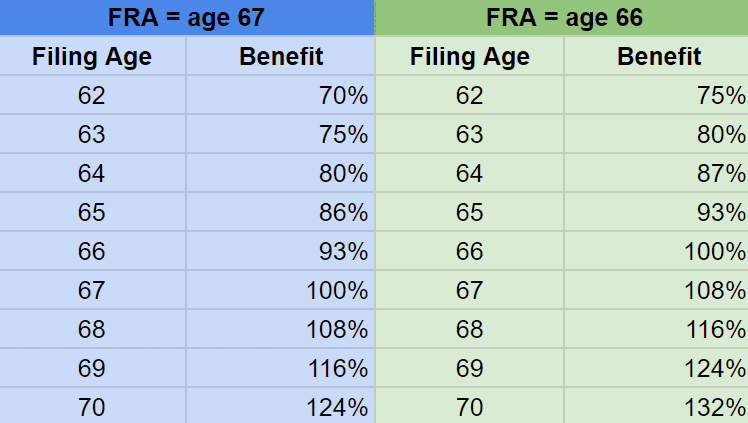

For starters, we need to understand how retirees’ benefits change as they age. Depending on their birth year, today’s retirees reach their “Full Retirement Age” (FRA) at 66 or 67 years old. Depending on the age at which they apply for Social Security, they’ll receive a certain percentage of their full benefits, described in the table below.

To make the math easy, we will assume our retiree’s Primary Insurance Amount (PIA)…aka the amount you receive if you wait until FRA…is $1000 per month. So “100%” on the table above equals $1000 per month.

The longer our retiree waits, the higher their monthly payments will be. But what does that look like as an “investment?” And how does inflation factor in?

What About Inflation?

The Social Security Administration adjusts everybody’s Social Security payments yearly to account for inflation. This “cost of living adjustment” is often shortened to “COLA.”

The average COLA adjustment since 1975 has been 3.66%. We need to include that in our spreadsheet, too.

Baseline Analysis – No Investments Yet

Let’s start with a baseline analysis. We’ll examine a series of retirees who collect their Social Security monthly and immediately spend it. They make no investments with their Social Security cash flow, which we could conceptualize as hiding those dollars underneath their mattresses.

We’ll compare results by examining the total dollar amounts collected over time. This will be our baseline analysis. You can follow along on the spreadsheet tab labeled “No Investment Return (Yet) – Nominal Dollars Only”

The results: in this scenario, early collection only makes sense for a retiree who dies before age 74. This result should make sense. We know that delaying Social Security makes more and more sense the longer someone lives.

Let’s now add in investment returns.

Analysis 1: Investing in a 4.7% Savings Account

Let’s consider a retiree who takes all of their Social Security income and deposits it into a savings account bearing 4.7% annual interest.

Why 4.7%? That’s the average overnight Federal Funds rate since 1960, and modern-day high-yield savings accounts tend to offer interest rates closely correlated to the Fed Funds rate.

Note: if your personal pile of cash (e.g. emergency fund) isn’t in a high-yield savings account, you should ask yourself why that is…

The results: if you pass away at age 77 or earlier, collecting Social Security earlier makes sense. Otherwise, waiting until FRA or later likely makes sense. This is no different than “traditional” Social Security advice.

Analysis 2: Investing in a “Standard” 60/40 Portfolio

What if our retirees put their money in a tried-and-true 60/40 portfolio? This asset mix – 60% stocks, 40% bonds – is the “bread and butter” of retirement portfolios. (Here’s a great primer on the expected returns of stocks, bonds, and a 60/40 portfolio)

From 1950 until today, a diversified 60/40 portfolio has returned an average of 9.3% per year. Let’s use that 9.3% annual return in our spreadsheet. Does collecting Social Security at age 62 make sense?

The results: Whoa! As shown on the “A2” tab of the spreadsheet, collecting as early as possible makes sense for anyone who would pass away before age 88.

We know, on average, most 62-year-olds are going to pass away well before age 88. Therefore, the smart, probabilistic thing to do is collect Social Security as early as possible and invest it in something like a 60/40 portfolio (or something with greater returns).

What a result!

But wait…

Because I’ve only shown you half the story. And that’s a major problem.

Big Problem: What’s the Risk?

If we zoom out on reader DT’s idea as originally stated, we should confidently conclude: OF COURSE, it makes sense! With sufficiently high investment returns, you should always invest as early as possible.

Even if the benefit of delaying Social Security was 20% per year, but I had an investment that paid me 40% per year, I’d rather start collecting as soon as possible and get the money invested. Given sufficiently high returns, you always want to start compound growth ASAP.

But we must return to a foundational pillar of investing and an oft-repeated maxim of The Best Interest: Risk and return are intrinsically connected. Returns are not “free.” Instead, they are compensation for taking on investment risk.

Whenever an investor compares returns alone, without also comparing the risks involved, they conduct an incomplete analysis. DT’s original question only considers return. It doesn’t consider risk.

Note: this is reason for the concept of “risk-adjusted returns.” To compare only the returns of two investments is not an apples-to-apples comparison.

What Comparison Makes Sense?

To make a sensible comparison, we need to “level the playing field” in terms of risk.

The benefits of delaying Social Security are guaranteed by the U.S. government. That’s very low risk. What kind of investment risk should we compare that to?

I see two viable options.

First, why does Warren Buffett invest all of Berkshire Hathaway’s extra cash into U.S. Treasuries, instead of an S&P 500 index fund? Doesn’t he know the S&P 500 has much better long-term returns?!

Answer: U.S. Treasuries are as risk-free as anything in the investing universe, backed by the full faith and credit of the U.S. government. As long as Uncle Sam pays debts, U.S. treasuries are risk-free. The S&P 500 is far from risk-free, and Buffett knows it. He wants his cash to be safe and ready for deployment at a moment’s notice. The S&P 500 cannot fulfill that need.

The first logical comparison today, then, is to use a true “risk-free” rate as our investment return. A high-yield bank account (FDIC insured) or short-term U.S. Treasury is appropriate. Conveniently, we already did that in Analysis #1, where our conclusion is no different than traditional Social Security advice: the “break even” point occurs in the late 70s.

The second option is to show the downsides of Analysis #2. That is, to show how 9.3% per year from a 60/40 portfolio is far from a guarantee. More specifically, I’d like to show how the downside risk of a 60/40 portfolio could turn our result on its head. What happens if we suffer bad market timing during our early Social Security period?

Looking at historical returns, a 60/40 portfolio has had 10-year periods with returns below 2% per year. What if we started our Social Security timeline with that kind of low return, and then made up for it at the end of the analysis? That’s what I show on our spreadsheet on the A3 tab.

The results? The 60/40 “solution” clearly comes with large risks! In this scenario, our “early Social Security hack” only worked out if our retiree died before age 75. That’s not a good outcome. Doubly so if Social Security is a safety net or backstop in your financial plan.

What About the Spousal Factor?

Great question. Spousal benefits are a huge part of Social Security analysis and must be considered in depth.

I discussed them in-depth in this article: “When Should I Take Social Security?”

To Apply or Not Apply

If your Social Security is “play money” in your financial plan, and you’re ok with risking a loss, I can see the merit and appeal of DT’s proposal. You can apply for Social Security early, invest it (reasonably), and the odds are in your favor that you’ll end up in a good spot.

But it’s no guarantee.

And the entire point of the Social Security system is to provide a guaranteed benefit to retirees. If Social Security plays even a minor role in your financial plan, I would strongly discourage putting that money at investment risk to eke out extra returns.

When we make a level comparison by using a risk-free rate, like in Analysis #1, we see there is no net benefit to taking Social Security early to invest it.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

You need to address the spousal factor. When you die, your SS benefits stop….and your spouse gets nothing of your benefits further.

Hey Anon – thanks for writing in. A couple rebuttals for ya:

1) My article here goes in-depth on spousal benefits: https://bestinterest.blog/when-should-i-take-social-security/

2) You wrote: “your spouse gets nothing of your benefits further” — this is not a factual statement. Survivor benefits apply in many (but certainly not all) scenarios. Every retiree/couple needs to evaluate their own optimal solution to Spousal and Survivor benefits.

Hi, Jesse. I’ve done a similar analysis but also taking into account different starting portfolio amounts, non-static/adjusted rates of return and COLA. What I found is if your portfolio withdraw rate is =< 4%, it generally takes until age 90 or so to have your "take at 70" portfolio to overtake your "take at 62" portfolio. This tends to hold true even if you do use static rates of return and COLA/inflation amounts too. And while we all would like to think we'll live to enjoy that money at 90, we're not going to – for me, at 90 it's not going to matter. My analysis also took into account 85% of SS income being taxable too.

My conclusion is taking SS at 62 protects you from sequence-of-return risks early in retirement and in general gives you more money that you do not have to withdraw from your portfolio provided your withdraw rate is less than 4%.

Hey hey – thanks for writing in. Sounds intriguing. Can you share your work (spreadsheet link?) Thanks!

This is exactly what I discovers too. Basically, you have to spend your portfolio to delay until to 70 to claim. That’s a lot of money still invested over your retirement years, and your net worth is the in winner. If not concerned about net worth, then delay till 70z

This is exactly what I discovers too. Basically, you have to spend your portfolio to delay until to 70 to claim. That’s a lot of money still invested over your retirement years, and your net worth is the winner. If not concerned about net worth, then delay till 70 and go for spending money.

I’m glad, Scott. Thanks for writing in.

Missing here is the affects on your taxes, and Roth conversion strategy and getting ACA credits if you’re going to retire before 65, NII tax and Irmaa .. more complex than you think.

Hi Paul, thanks for writing in. You’re absolutely correct. But hear out my logic 🙂

Ultimately, every single retirement planning analysis is a function of ALL the different puzzle pieces.

Want to discuss asset allocation? Well, you need to think about taxes, Roth conversions, ACA credit, NII tax, Social Security, IRMAA, and much more.

Want to discuss the ACA? Well, you need to think about taxes, Roth conversions, asset allocation, NII tax, Social Security, IRMAA, and much more.

*EVERY* retirement topic involves all the others. The more you read and listen to my work, the more you’ll see how that’s one of my pillars.

As such, it would make for somewhat boring / repetitive articles and podcast episodes if EVERY SINGLE ONE repeated those same mantras over and over again.

In other words – what you’ve written is a given. You’re absolutely right. Taking Social Security involves taxes, Roth conversions, ACA credits, etc etc etc.

I am not sure I get this scenario. If you take the SS early and invest the money in a 60/40 portfolio, what money are you living on? If you say that you are living on your investments and don’t need the SS so you are investing it, you are selling your investments to live on and replacing the investments with SS money. Its just moving money from one place to another. A zero outcome arbitrage. Doesn’t make sense to me

Hi Josh – yeah, I know what you’re asking but you’re not quite getting it right.

See if this example helps

Our couple needs $100,000 per year to live on.

If they collect SS at age 62, it will provide them $25,000 per year.

If they delay to age 70, it will provide them $50,000 per year.

So, if they delay Social Security to later, then during the early years, the FULL $100,000 to fund their lifestyle must come from their portfolio.

They are draining their portfolio faster in exchange for a larger future SS benefit.

If they take SS earlier, they “only” need $75,000 per year from the portfolio.

They are leaving more money invested in their portfolio, in exchange for a small SS benefit.

That is the simple trade-off examined here.

“Taking SS early and investing the money” really means “leaving more money in your portfolio than you otherwise would.”