Don’t miss an episode of our podcast, Personal Finance for Long-Term Investors. Available on all podcast players.

Here’s the latest episode:

Thanks to reader Lynn, who wrote in this week with some specifics about her household’s situation and an overarching question: When should we start taking Social Security?

I’ll provide background information below, and then we’ll discuss a few common “if –> then” heuristics to help you with your Social Security planning.

Background – The Pros and Cons of Taking Social Security Early

Social Security is a government program that provides financial support to individuals who are retired, disabled, or survivors of deceased workers, funded primarily through payroll taxes. It aims to ensure economic stability and security for eligible participants by offering benefits to mitigate income loss due to retirement, disability, or death.

Today, we’re talking about retirees.

American retirees each have an “eligible benefit” from Social Security, which is based on the following factors.

- They must be 62 years old or older

- They’ve worked and paid into Social Security for at least 10 years (measured quarterly, for a total of 40 or more quarterly credits)

- They could be eligible for additional credits based on their spouse’s work history, too.

- Your eligible benefit is determined by your highest 35 years of earnings, with each year’s earnings adjusted for inflation (aka “indexed”). The higher your overall earnings, the greater your Social Security benefit will be.

Quick Example: AIME and PIA

Here’s a quick example:

Bob worked the same job from age 22 to age 62. His salary in 1984 was $25,000, and he’s received a 4% raise every year since; he’s earning $120,000 now in 2024 (his final working year).

We’d use the Social Security indexing factors to adjust each of his prior years’ earnings by rates of inflation. We’d then pick the highest 35 years, find the average, and divide by 12 to get Bob’s average indexed monthly earnings, or AIME.

Bob’s AIME is $8717. Here’s the Google sheet with the math. Feel free to make a copy.

Note 1: because only a certain percentage of income is subject to Social Security taxes, only that portion of earnings is considered for AIME. In 2024, the FICA income limit is $168,800. Even if someone earned millions every year for their entire career, their AIME would only include that smaller portion of income that was taxed by FICA. That logic is why the maximum AIME in 2024 is ~$13,100.

Note 2: if you don’t work a full 35 years, you’ll have some “zeroes” in your AIME math. This isn’t ideal. But depending on the rest of your work history, these zeroes could have a major effect or a minor effect. The PIA section below will shed more light.

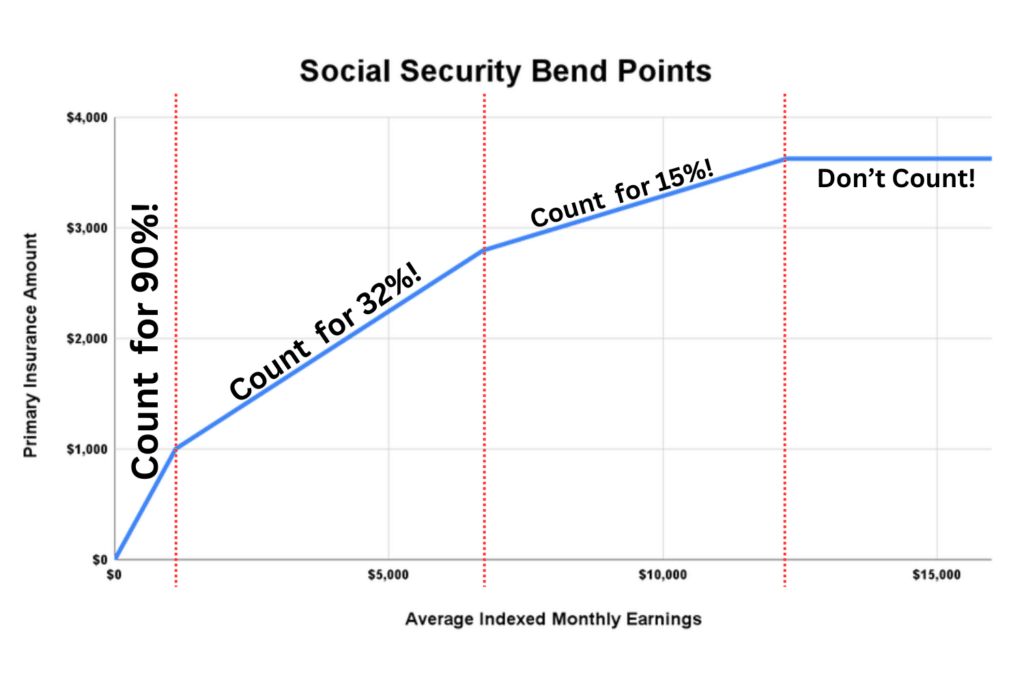

Next comes PIA, or the Primary Insurance Amounts, aka what you actually receive from Social Security if you retire at “full retirement age,” or FRA. PIA is the real deal. An individual’s Social Security benefits (or PIA) are based on specific percentages of that individual’s AIME. For 2024, the PIA math is:

- Take 90% of AIME below $1174

- Plus 32% of AIME between $1174 and $7078

- Plus 15% of AIME above $7078

If we run that math for Bob, whose AIME was $8717…

- 90% of his first $1174 = $1056.60

- plus 32% of ($7078 – $1174) = $1889.28

- plus 15% of ($8717 – $7078) = $245.85

For a grand total PIA of $3191.73 per month.

You see – not all your AIME dollars count the same! The first dollars matter a lot – they’re counted at 90%! The latter dollars are only counted at 15%. And since high-earners’ latter dollars aren’t factored into AIME at all, we can think of those dollars as being counted at 0%. This concept is dubbed the “Social Security bends” or “bend points” because of how it looks when graphed out.

If you have a “zero year” in your 35 years of earnings, your AIME will certainly decrease. But if you’re already in the 0% or 15% section of the PIA graph, it might have only a tiny effect on your PIA. It’ll have a huge effect if you’re in the 90% section.

Bob had his final ~$1700 of AIME in the 15% section of the PIA graph. I ran a quick test and turned his 35th year into a zero. His AIME dropped from $8717 to $8487 – a $230 drop. His PIA dropped from $3192 per month to $3157 – a $35 drop. $35, you might guess, is 15% of $230.

PIA is Bob’s benefit if collects at “full retirement age.” But what if he collects early?

What About the Age You Start Collecting?

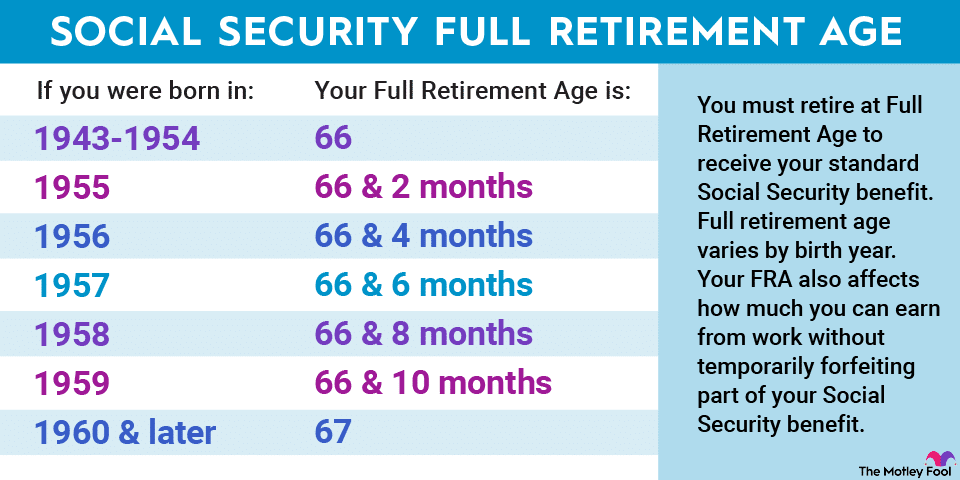

Social Security uses a concept called “full retirement age” (FRA) to determine how much of your eligible benefit you get to collect. Your personal FRA depends on the year you were born. The chart below shows the details:

FRA is either 66 or 67 years old for today’s new retirees. You can start collecting Social Security benefits before your FRA, but there’s a price to pay. Your benefits will be permanently reduced. But by postponing your benefits until after your FRA, your benefits will be permanently increased. The two charts below show both sides of that coin for both age 67 FRA retirees and age 66 FRA retirees.

Let’s do a quick decoder to make sure you understand how this all fits together.

If Bob was born in 1962 (and therefore is 62 years old today), he could start collecting Social Security right now. His FRA (based on his birth year) is 67, so we’ll consult the blue section of the table above. By collecting at age 62, Bob will only receive 70% of his full benefit. His PIA was $3192 per month; Bob would only collect 70% of that, or $2234 per month.

If Bob waits to collect, a few things will happen.

First, the AIME math could change to account for inflation and other factors. On net, this will increase Bob’s PIA. Note: your “Bend Points” do not change; they are set during the year you turn 62, and they will remain your Bend Points for life.

Second, Bob’s postponed filing age will increase his benefit amount, per the blue table above. If Bob waits until age 70, he’ll receive 124% of his PIA.

This begs a question: should Bob collect early to get those extra years of income, though at a discounted benefit? Or collect later, for fewer years, but at a much higher rate? When is the breakeven point?

The Breakeven Point for Collecting Social Security

When is the breakeven point for collecting Social Security? I looked at retirees with FRA = 67 years old. Here’s my Google sheet if you want to play around with it yourself.

With the bare eye, you can see the breakevens occur in the upper 70s. The joke in financial planning is, “Tell me when you’ll die, and I’ll tell you when to start collecting Social Security.” But the rough outline is:

- If you die before age 77, collecting as early as possible would have been best.

- If you die between ages 78-80, then all scenarios are roughly equal (all within ~6% of one another)

- If you die after age 80, then waiting until at least “full retirement age” of 67 has distinct advantages

- If you die after age 84, then waiting until the maximum collection age of 70 becomes optimal, and it only gets better the longer you live.

But there’s much more to consider than “how long will you live?”

So let’s get to the real meat of the article: what are some applicable thought processes, strategies, and if –> then scenarios to guide you and your family in Social Security decisions?

This is Hard to Get Right

As Annie Duke says (and I love to repeat), two things determine outcomes in our life:

- the quality of our decisions, and

- luck.

Or, put another way, there are things in your control and things out of your control.

Whatever decision you make regarding Social Security, you must accept that luck might strike, and your decision won’t have been the optimum one. It’s not because of the quality of your decisions. It’s because of luck. (This is “results-oriented thinking,” a bias worth breaking.)

You Want to Get This Right

This is close to a one-way gate.

Once you start collecting Social Security, you do have up to 12 months to 1) change your mind and 2) repay any benefits you’ve received so far. You get one of these “withdrawals” in your lifetime.

Once you delay collecting, though, you can’t go back in time and reclaim those missed benefits.

Ideally, you want to get this decision right.

Health, Illness, Family History, and Social Security

The most common questions surrounding Social Security revolve around your personal health and family history. We’ve determined that ages in the late 70s to early 80s are the “break even” point. You should ask: does anything in your personal or family history point you toward an early or late death?

If you’re healthy and all your relatives live to 100, it’s reasonable to assume you could have a similar fate. Postponing Social Security as long as possible (age 70) makes sense.

If you’re chronically ill, your relatives have all passed away early, etc., again, you can reasonably assume you could have a similar fate. Collecting Social Security as early as possible would make sense.

Granted, I’m not a doctor. One health phrase worth remembering is, “Genetics loads the gun, environment pulls the trigger.” In other words, you aren’t condemned to your family history. You have dials to control. Don’t forget that.

Do You Need It? It’s Longevity Insurance.

Do you need to take Social Security early? Will that extra income bridge the gap between cat food and a normal human diet? Because if you don’t need Social Security, why take it early?

Delaying your Social Security will act as “longevity insurance,” protecting against the risk that you will live to 90, 95, or beyond. The longer you wait, the higher your benefit will be, and the better your long-term outcomes will be.

Are You Still Planning to Work?

Are you planning to work while also collecting Social Security? Tread carefully! Your work income will actively eat away at your Social Security benefits.

Bob, for example, who is age 62, can only earn $22,320 in ordinary income before he hits trouble. For every $2.00 he earns above that limit, $1.00 will be deducted from his annual Social Security benefit. If Bob earns $125,000 (like he did last year) while also collecting Social Security at age 62, he effectively receives $0.00 in Social Security benefits while being permanently hamstrung by his choice to collect early. Ouch.

That specific income limit increases to $59,520 during the year someone reaches their FRA, and the penalty ratio “lessens” to 3-to-1. The penalty disappears altogether once the FRA has been reached.

There’s always a corner case, so making a concrete rule about working while collecting is hard. That said, it’s like going into credit card debt. You really want to avoid it if you can. You really want to avoid starting Social Security benefits before full retirement age if you plan on working.

Consider Spousal Benefits

Spousal benefits are one of the many rabbit holes in Social Security planning. There are many paths, they go deep, and it’s easy to get lost. Trust me, Alice.

The upshot for basic Social Security planning is that your decision to collect Social Security not only affects you, but could affect your current spouse, your ex-spouse, and/or your future spouse or future widow.

Remember Bob? His PIA is $3192 per month. Bob is married to Sharon. Her PIA is $1200 per month. Let’s say they both opt to start collecting at FRA, and thus collect exactly 100% of their PIA each.

Sharon also gets to collect a spousal benefit. If she applies for a spousal benefit when she hits her FRA, she is eligible for 50% of Bob’s PIA (or $1596 per month). She’ll collect her $1200 benefit and then an additional $396 per month.

But if Sharon had applied for the spousal benefit at age 62, she’d only be eligible for ~35% of Bob’s PIA, or $1117 per month. Since this number is lower than her own benefit of $1200, Sharon will get no extra spousal benefit.

Now, what if Bob dies?

- Notably, Sharon would step into Bob’s benefit, receiving the full $3192 per month!

- If Bob had started collecting at age 62, though, his benefit would have been $2234 per month. Sharon would step into that $2234 per month benefit when he died.

- If Bob had started collecting at age 70, his benefit would be $3958 per month. Sharon would step into that $3958 per month benefit when he died.

Bob’s decision doesn’t only affect his benefits. It also affects Sharon, assuming she outlives him.

Some rules of thumb when it comes to spousal benefits:

- The lesser-earning spouse can start collecting Social Security as early as possible, especially if they’ll become eligible for a larger spousal benefit at FRA (e.g. just like Sharon, who jumped from her own benefit up to the spousal benefit of $1596)

- The higher-earning spouse should delay Social Security to age 70 because their decision not only has a 100% chance of affecting their own benefit but also has a ~50% chance of affecting their spouse’s eventual benefit (if we assume the “who dies first?” question is a coin flip).

What About the Overall Financial Plan, and Sequence of Returns Risk?

How does Social Security fit into your total financial plan? Especially in the early years of retirement, where you’re most at risk for a sequence of returns disaster?

“Sequence of returns risk” refers to the potential that a poor-performing portfolio early in your retirement will cascade into long-term pain. If your assets are worth less early on, you’ll be forced to sell more of them than you anticipated. This leaves fewer assets in your portfolio to grow for the long run.

One way to mitigate this risk is to find alternate sources of retirement income. Social Security, perhaps?! If early Social Security is a vital part of your overall plan’s success, the failure risk introduced from delaying Social Security could be too great to bear.

Taxability Concerns

Social Security is taxable (for many retirees). It’s worth considering if your decision to collect Social Security will have taxation impacts and what your net-of-tax benefits are.

What Do Your Trusted Advisors Have to Say?

While every retirement is a unique adventure, these adventures often rhyme. Your trusted advisor(s) might have seen dozens or hundreds of successful retirements before, all of which rhyme with your plan.

Their counsel might sway you in an optimal direction.

“I’m Ready Uncle Sam!”

Are you ready for Social Security? It’s not an easy question to answer.

Hopefully, I’ve answered more questions today than created new ones. Still, don’t hesitate to reach out with any questions or concerns.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

So comprehensive an explanation….so well done!

Thank you! I’m glad you enjoyed it!

-Jesse

One thing that has always confused me about spousal benefits is a situation with a large age difference. My husband is 10 years older and I am the higher earner. Does it affect the consideration if he starts collecting a full decade before me?

Great question. This answer will show you the difference between the *Spousal* benefit and the *Survivor* benefit.

An important note to start: since you are the *high earner*, there’s a strong likelihood that you won’t be eligible for Spousal or Survivor benefits. Generally, those benefits only come into play to benefit the lower earning spouse.

In your scenario, your (potential) Spousal benefit would be based on the age when *you* applied for it. Your spouse’s age does not matter. The age at which your spouse started collecting Social Security does not matter. If your spouse *has not started collecting yet themselves,* then you cannot apply for the Spousal benefit yet.

The Survivor benefit works differently. Survivor benefits are partially based on the age at which *you* apply for them. They are also based on *when your deceased spouse starting collecting SS.* In this way, delaying SS will increase personal payments *and* will increase survivor benefits for your spouse, if you should die first.

It’s hard to give you personal Social Security advice without knowing your full financial picture. Feel free to shoot me an email… [email protected]

Awesome write-up! Thank you for being so in-depth in the mechanics of it. Do you happen to know about the site ssa.tools? It’s what I use to estimate my PIA based on changes in my career. I’ve found it incredibly useful when helping relatives understand their future social security benefits.

Hello! Thanks for the kinds words. I did end up on SSA.tools during my research for the article, but I didn’t actually play around with it much (time was short!). But I’m going to go take a look at it now from your recommendation. Thanks!

I actually ran the Social Security calculation last year to determine what my benefits would be at age 70. The calculator is easy to use since I just had to enter 40 numbers for my earnings by year. However, I didn’t understand the calculation until reading this post. (BTW, the Social Security report does a nice job detailing each step in the calculation.)

I didn’t know that the calculation used ‘Taxed Social Security Earnings’

I didn’t know that the calculation indexed the ‘Taxed Social Security Earnings’ for prior years before determining the 35 highest years.

I didn’t know that the calculation used bend points from the year you turned 62 (i.e., not 2024 bend points)

I didn’t know that the calculation applied COLA percentages for subsequent years (age 62-69) and then applied the 1.32% increase to come up with the age 70 monthly benefit.

It’s certainly complex! I’m glad my article cleared up a lot of that for you.

Jesse

I’ve been helping my mother-in-law figure out her social security benefits (she’ll be 65 next year and wants to retire), and this was so helpful! She is divorced but was married long enough that she would quality for spousal benefits. However, I didn’t realize that it was an option to apply for BOTH as a way to potentially increase her social security income when she hits FRA. She plans to take her benefit at age 65 instead of waiting for FRA. It’s been almost impossible to get answers from the social security office on what amount she would qualify for based on her ex-husbands income.

Hi Bethany, I hope all is well. Thank you for leaving a comment on my blog article about Social Security benefits.

You mentioned one thing in your response that I felt compelled to reach out to you about.

If your MIL begins collecting SS at age 65, then I believe that would negatively affect any benefit she might be eligible to collect from her ex-husband’s work record.

She would have to wait until her full retirement age (likely 67) in order to not be negatively affected in this way.

Does that make sense?

Some other food for thought…all these pre-requisites are necessary:

Their marriage lasted at least 10 years

She is currently unmarried

She collects at 62 or older (but, again, penalized if before her FRA)

Her ex-husband is entitled to his Social Security benefits (even if not collecting yet)

The benefit she’d receive based on her own work record is less than what you’d get as a divorced spouse

That last one is worth paying attention to!

Depending on your mother-in-law’s own work record, her benefit might be more significant than the divorcee benefit – which is 50% of whatever the ex-husband’s benefit is.

I know this is a lot of info. Please let me know if you have any more questions.

All the best,

Jesse

Another highly useful article! Thanks. As an optimizer, I like the idea of knowing the rough break-even points:

– SS Investment break-even point is the late 60’s

– The death gamble is the late 70’s

– Investment opportunity cost is the late 80’s

Knowing this information helps me to know how to consider SS.

I’m going to forget all of the above and postpone taking SS inorder to be able to do some larger up-front Roth conversions; The tax savings seem better than SS optimization, and holding off on SS improves longevity plan.

Thanks Dave!