Highlights and Takeaways

- The average millennial is 35 years old, earns $54,000 per year, and has a net worth (including any home equity) of around $130,000

- 45% of millennials have student loan debt, with an average balance of $40,600

- 52% of millennials are homeowners, with a majority of those home purchases occurring over the past 5 years

- 55% of millennials have children, with a total U.S. birthrate in 2021 of 1.66 children per woman (it takes 2.00 children per woman for the population to replace itself, so we might be in trouble there…)

- There are simple steps you can take to become better-than-average financially, including focusing on increased income, measuring your monthly cashflows, using tax-advantages investing vehicles, and more.

The Stats

I’m a Millennial. Many of you reading this are too. Millennials – also called Gen Y – are people born between 1981 and 1996. The average millennial is currently 35 years old.

Let’s walk through some vital financial statistics for American millennials. Then we’ll talk about how we can improve our own financial life to become above average.

Using income data and net worth data from the website DQYDJ, we can see that the average 35-year-old earns $55,000 per year and has a net worth (including home equity) of $130,000.

If we add in data from this Business Insider article, we also learn:

- Just under half of American millennials have student loan debt. Roughly 45% of millennials have loans, with an average remaining balance of $40,600.

- I’m sure this data skews younger. The oldest millennials are 42 years old, while the youngest are 27. Not only have college costs continued to rise in the past 20 years (affecting younger Millennials more than older), but there’s also the plain fact that older millennials have had more time to pay their loans off.

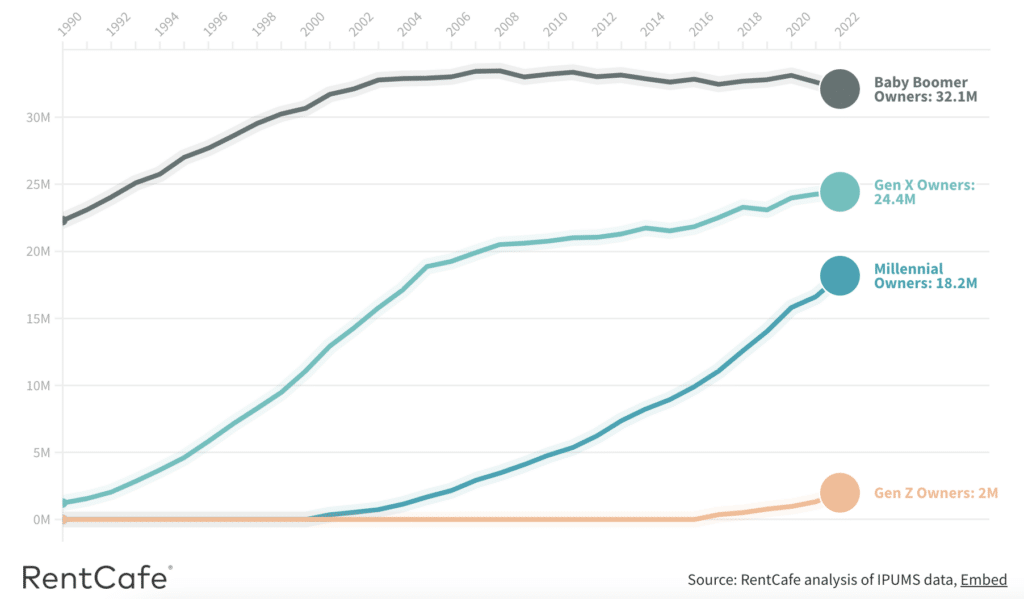

- According to a RentCafe study, 52% of millennials own a home.

- 18.2 million Millennials now own, or share ownership in, a home, vs. 17.2 million millennial renters (note: this data looks at the 110 largest American metro areas, thus does not include all millennials)

- Again, this data likely has an age skew. The chart below shows how millennial homeownership first increased in the early 2000s – when the youngest millennials were still in elementary school. The oldest millennials have had a long time to buy.

- That said, 7.1 million millennials became homeowners in the past 5 years (including yours truly). More and more younger millennials are looking to purchase homes.

- An important caveat…home ownership might be the so-called “American Dream,” but it’s not mathematically optimal for all people, nor a great investment in general. I’m a huge proponent that your primary home is “a home first, an investment second.” You need a place to raise a family. You don’t need a 7% real return on investment.

- According to an older (2019) Pew Research study, fewer millennials are starting families than previous generations. Pew found that 55% of millennial women had had a live birth, compared to 62% of Gen X women and 64% of Baby Boomer women in the same age range.

- What does this have to do with personal finance?

- First, kids are expensive. Having kids is financially challenging. And not having kids can be a symptom of an already-challenging financial life e.g. “I’m not having kids because I couldn’t afford to give them a good life,” or, “My goddamn student loans were so high we delayed having kids by 5 years.”

- Second, birthrates drive economies. Children grow into adults – who work, consume, and oil the economic machine. Personal finance is tied to that economy.

How to Be a Better-Than-Average Millennial…At Least Financially

What can you do to rise above the average?

First, adopt a stoic mindset. If you’re “worse” than average, you’re not a bad person. And whatever happened in the past – those events that brought you to this moment – is immutable. You can’t change it. All you can do is forge on and blaze a better trail ahead.

So let’s blaze that trail.

Salary and net worth are easy-to-measure metrics, so let’s start there.

Improving Your Salary

One of the worst pieces of financial advice I see all too often is, “Did you consider increasing your income?” …as if there are raises hiding in your office cabinets if only you’d look for them!

The better advice, instead, is encouragement that you can increase your income. You just need the right approaches and tactics. What are some examples?

- Talk to your manager. Is there a path for increased pay in your role or at your company? Ask them: what does that path look like? Get them to agree that if you follow the path, a pay raise will follow.

- More education. Maybe there isn’t a positive path at your current job. It’s a dead end. You need to find ways to get on a better path, and further education is highly effective. BUT! You need start with the end in mind. Get a degree or certification that will truly further your career and your income. Computer science? Yes. Underwater basketweaving? Not so much.

- Look outside your current role, too. One of the fastest ways to higher pay is by switching jobs. Or using a potential job switch to negotiate a raise.

- Side hustles can work. But choose carefully. I know too many Uber drivers who, if they ran the numbers, would realize their side hustle barely pays them minimum wage.

Increasing Your Net Worth

Salary is a one-trick pony. All it measures is incoming cashflow in. Net worth is far more comprehensive, as it’s a function of:

- inbound cashflow

- outbound cashflow

- changes in asset values (e.g. investment growth)

There are many ways to increase your net worth, most of which are within your control today (unlike increasing your salary, which might take years to successfully execute).

- Learn from the #1 lesson I’ve found from the various financial experts I’ve interviewed on my podcast:

- Measure your cashflow – a.k.a. budgeting. You can’t manage what you don’t measure. The only way you’ll ever decrease your spending is if you measure your spending. You need a budget – it can be detailed, or simple. But you can’t not have a budget.

- Follow the financial order of operations. Learn how to prioritize your financial to-do list.

- Put in more “work” to combat financial disorder. You’ll need to read this article for context.

- Remove the negatives. Personal finance is a “negative art.” Increasing your net worth is more about avoiding mistakes than taking huge steps forward.

- Bucket your money, then put it to work. Determine the timeline for the various expenditures in your life, then invest the money you don’t need in the short term.

- Take advantage of tax advantages and “free money,” like 401(k) or Roth IRA accounts.

Housing and Kids

How can you be “better-than-average” in terms of housing and children?

If you’re thinking, “Homeowner plus 3 kids is better than renter with zero kids,” I think you’re doing it wrong. Instead, consider the financial (and more importantly, non-financial) acumen that goes into making those decisions.

For example, I think rent vs. buy calculators – like this one from Nerdwallet – are fantastic tools. If the math points you toward renting, then rent. There’s no race to be a homeowner, nor do I think homeownership is intrinsically good. “Better than average” doesn’t apply here.

But I think it’s more important to look yourself in the mirror and be honest with answers like:

- How many years do I plan on living here?

- Do I love this house? This neighborhood? This school district?

- If this home never appreciates in value, am I ok with that?

- Or the alternative: Since rent doesn’t build equity, am I ok “throwing my money away” in exchange for flexibility and less responsibility?

Children are even more personal and less financial. The only major financial question, in my opinion, is: do we have the financial means to provide for this child? Every other important question is personal.

Again, there’s no such thing as “better than average.” Instead, I see child-rearing in a binary way: are you giving your children a good home? Or not?

If you are, then you’re doing it right. Whether you have 10 kids or 1, you need to give them a good home. What’s a “good home” vs. a “bad home?” Everyone’s opinion will differ. But you know it when you see it.

Millennials are getting their financial life in order. It’s a wonderful thing. And through smart, patient personal finance decisions, you can carry on to become a “better-than-average” financial millennial. Investing in knowledge is a great place to start.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!