Don’t miss an episode of our podcast, Personal Finance for Long-Term Investors. Available on all podcast players.

Here’s the latest episode:

I’ve been having a nice email dialogue with listener Bethany about her parents’ retirement situation, and she asked me:

Why do you typically recommend the higher Social Security spouse delay until 70? Is this just to ensure the longevity of their portfolio?

Great question!

Why do some financial planners suggest that in a married couple, the spouse with the greater Social Security benefit delay collecting until age 70, while the spouse with the lesser Social Security benefit starts collecting at age 62?

Here’s the simple reason the higher-earning spouse should (at least consider) delaying Social Security until age 70.

Mom, Dad, and the Bigger Benefit

An example will help. Let’s think about two people, MOM and DAD.

Mom has a smaller Social Security benefit.

Dad has a bigger Social Security benefit. Let’s just say Dad’s benefit is twice as large as Mom’s.

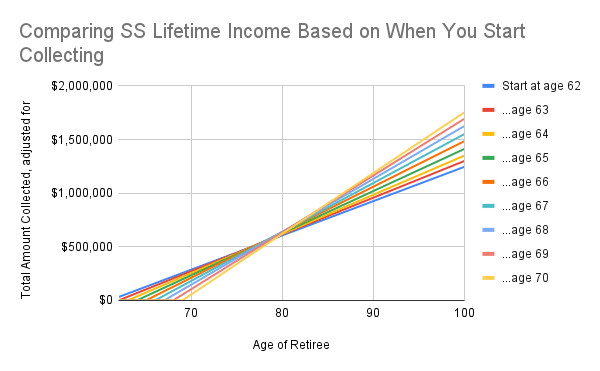

For both of them, no matter their benefit size, their “break-even” age is around age 80. This article shows you how that works:

For the sake of easy numbers, we’ll just say their breakeven age is 80 years old. That means, if we only consider their own individual benefit**, they must live past age 80 (their breakeven age) to reap the benefits of delaying Social Security. If they die before age 80, they would (in hindsight) have preferred collecting Social Security at an earlier age.

**This is a crucial qualifier that we will later have to amend.

But should we only consider their own individual benefits? No!

When one spouse passes away, the surviving spouse may be eligible to inherit the deceased spouse’s Social Security benefit, receiving the higher of the two benefits going forward.

In other words: there are essential scenarios where Mom will receive Dad’s larger Social Security benefit. Namely, if Dad dies first. In other words:

- Mom’s smaller benefit will cease to exist upon the first spouse’s death. Always.

- Dad’s larger benefit will continue to live until the second spouses’s death. Always.

There are (4) possible scenarios…

1 – Mom and Dad both die before age 80

2 – Mom dies before 80, Dad dies after 80

3 – Dad dies before 80, Mom dies after 80

4 – Both die after age 80.

In three of those four scenarios, at least one spouse lives beyond age 80. In 75% of scenarios, having Dad delay his Social Security until age 70 ended up being the right decision for the family.

“I Read Each and Every One”

That’s what someone wrote in this ⭐⭐⭐⭐⭐ podcast review…

My free weekly newsletter helps busy professionals and retirees avoid costly mistakes and grow lasting wealth through retirement.

Join 4000+ subscribers, 100% free.

Sign up here:

Why *SHOULDN’T* You Pursue This Strategy?

Now, I’m assuming that all four of our “death scenarios” are equally likely; that the odds are 25% for each. Clearly, real life doesn’t work that way. Every individual will have a unique and hard-to-predict mortality.

That’s why I like to ask questions about health history, etc. If both Mom and Dad are relatively unhealthy, and both have long family histories of early death, then I could certainly see the rationale for both spouses collecting early.

Health and health history are the top reasons why a couple might NOT pursue this type of claiming strategy.

Also, perhaps there are more questions to ask about Social Security claiming in general. Kitces.com recently released a terrific thought piece on various factors and risks for Social Security, the conclusion of which is…

…is that most traditional Social Security research biases too far toward claiming Social Security at later ages, and not enough toward early ages. A few of the arguments in the article make a lot of sense to me. Though I do disagree with the main argument (comparing Social Security “returns” to that of a 60/40 portfolio).

Why else might a couple NOT pursue today’s strategy, where the lesser benefiting spouse collects early, and the greater benefiting spouse delays until 70?

Immediate cash flow needs. Some couples simply need the income now for living expenses. In those cases, the theoretical lifetime-maximizing strategy takes a backseat to financial reality.

Age gap between spouses. If the lower-earning spouse is much younger, the survivor benefit may not come into play for decades. In that scenario, maximizing the higher benefit is less urgent, and taking benefits earlier might make more sense.

Tax considerations. Social Security interacts with other income streams. This is important to consider.

Confidence in other retirement resources. If the couple already has substantial pensions, savings, or guaranteed income streams, the Social Security survivor benefit may not be as critical. They might prefer to collect earlier and enjoy the income while they’re younger and healthier.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

Hi! Great post.

I’ve recently had an additional question about social security benefits. Hoping you can help.

I recently reviewed my social security statement (I don’t think I had actually seen it for years) and found out I only have 37 out of 40 needed credits to be fully insured to receive SS benefits when I am of age. I am 47 now. I work in education in CA and haven’t put into SS in 15 or so years. (I had employment outside of education prior). I didn’t plan to work outside of education before I retired…but now, I’m thinking I need to go work at Starbucks or similar for 3/4 of a year to earn those last 3 credits needed??? (That would be so strange for me). And is that true?

The SS statement stated that the longer you wait to do the credits, the amount needed for credit rises. So it seems that I need to handle this sooner than later, correct?

Secondly, my husband is a sole proprietor with his own business in the construction field. He doesn’t have any employees because he wants to keep it small. Would it be a plausible option for me to get a busines license for myself and do contract work for him like I typically help with anyway (helping some with billing, sending out invoices, etc), and gain those SS credits that way?

Any guidance regarding this is helpful and appreciated. Thank you!

Hello and thanks!

In 2025, if you’re paying into FICA, you earn 1 credit for every $1,640 of earned income, up to 4 credits per year. So if you earn $6,560 or more in 2025, you get the full 4 credits.

This means you don’t need to work a full year at Starbucks or anywhere else—you just need enough income to reach the threshold for 4 credits. For instance, if your hourly wage is $20, you only need roughly 82 hours of work per credit (20 × 82 ≈ $1,640), totaling about 328 hours (around 8–9 weeks full-time) for all 4 credits—not the whole year.

Yes, that “$1640 per credit” number rises over time, but likely doesn’t / won’t outpace inflation.

Since you’re so close to the 40 credits, I do think it’ll be worth pursuing. The juice will be worth the squeeze of ~10 weeks of work.

Re: your idea of getting a business license…I’m not sure I follow.

Ultimately, if your plan involves working for your husband’s business, I would do two things.

First, speak to your / the business’s accountant about the most effective way for your household to pursue this idea. I phrase it that way because there will be one set of effects on the business, and a second set of effects on the family tax return. It’s important to understand both.

And second, I would lean toward taking the path of least resistance. Setting up your own business in order to be a 1099 contractor for your husband sounds more complex than simply being a spousal employee.

It may be a non-issue depending on spousal benefit amount and timing of spouse filing for benefits.

Thank for this article – it reinforces part of my SS planning. My wife and I are 60 and 59 and enjoying retirement. We’re both healthy and have regular health screenings. We’ve both had one parent live beyond 90. My SS benefits will be a good bit more than my wife’s, but less than double. We don’t have a great need for extra income because we both have pensions and other income sources. So, It’s pretty clear to me that I should wait until age 70 to begin collecting SS. My dilemma is determining the optimal age for my wife to begin collecting SS in order to maximize total combined benefits over our lifetimes. Please include any insight you have on this in future publications about SS.

Hi NJP – a great question that certainly involves some of the other puzzle pieces in your financial plan.

One helpful thought about ALL financial planning – no matter what choice(s) you make today, some of those choices will (in the long run) be WRONG. You might not know it for years or decades, but eventually you’ll look back and wish you made different decisions.

The question, therefore, is which degrees of “wrong” can your financial plan handle AND can you live with (i.e. sleep well at night).

If your wife takes SS right now, you might look when you’re both age 90 and say, “Hmmm…wish we delayed.”

If your wife delays SS to 67 or 70, and then ONE of you passes before ~80/82, you might say, “Hmmm…wish we didn’t delay.”

OR!!! What actually happens a lot more than people think, is that your retirement will be successful and happy either way, and you’ll look back some day and say, “Even if our SS choice was “wrong” in retrospect, it didn’t really hurt our ability to live a great life, so we don’t really care.”

Good article Jesse, as per usual. I think most people would benefit from looking at social security through multiple lenses.

The 2 most common I hear: I am taking MY money at 62 because who knows how long the government can keep paying (for those of you who are curious, the US government has an 80+ year record of paying…but to each their own beliefs). Then I hear, I will take it at 62 because who knows how long I will live, which is VERY fair if you have reason to believe you will have a below-average life expectancy. You know way better than I would about your family health history.

Unless you interact or are part of the FIRE community, or have a good planner (wink wink, call Jesse if you do not), SO FEW married American’s ever consider having one spouse wait until age 70. The average life expectancy of ONE spouse of a couple who are both 60 is OVER 90. WELL above the 80 breakeven age to make waiting until 70 worth it. It’s a good idea for the higher earning spouse to wait, more often than not (as long as you can pay your bills until the higher earning spouse his age 70).

Also, at MOST, only 85% of Social Security income is taxed at the federal level. While a 15% break in federal income tax isn’t massive, its not nothing either.

Next, it’s guaranteed income AKA risk-free. Many people like to compare the ROI of SS to the stock market….that is inaccurate. The market has risks and SHOULD return more. Its best comparison would be 10-30 government bonds. 10 year T-Notes are getting what…4-4.5% NOT INCLUDING inflation. But SS can grow 6-8% PLUS your future COLA adjustments grow as well!

Now here is a concept to consider….in a world where you have a large guaranteed SS check…could you have a more aggressive risk profile and sleep well? Meaning….you could wait to take SS at 70 and then do a 75/25 investment mix….or take less SS at 62 and do a 65/35 or 60/40 mix. I’d prefer the first one….a bigger SS check each month covers more necessities, has a slightly lower tax bill, and lets me afford to take on more risk and still sleep well at night.

Lastly, more SS means you could potentially leave more to your heirs.

Could the US government reduce future social security….they SURE could…predicting that is even trickier than timing stock markets through. Maybe they WILL one day…but are you timing that prediction correctly is what you should ask yourself. Next…if they were to cut SS, what would happen to markets? They could likely take a bigger loss than the reduction in social security payments as many could lose faith in US markets.

There are reasons to not wait until 70…most include health-related issues and trying to time future policies of the largest and one of the more complex governments in the world. For me…my higher-earning wife will wait to collect lol.

If you take Social Security at age 62, you are permanently locking yourself into a lower percentage of potential benefits. So even if one spouse waits until full social security age or later to collect, the other spouse would receive maximum 32.5% of the other spouse’s benefit, rather than the 50% they could receive at full social security age (typically 67).

Hi Benjamin – do not confuse the SPOUSAL benefit with the SURVIVOR benefit. Your comment applies to the Spousal benefit, which doesn’t end up applying to most American couples due to the way the math works out. My article and logic is about the Survivor benefit, which applies to the vast majority of American couples.

I’m leaning toward delaying my social security until 70 b/c my wife is healthy and has a great family history. My only hesitation is to take social security at 62 to reduce the withdrawal pressure on our stock portfolio. I can and have certainly can beat a 12% yearly average gain in the market but of course that does come with risk but waiting also comes with risk. I put a view scenarios into Grok to calculate and it seemed to always point to delaying until 70.

Hi Eric – if you’re confident you can beat a 12% annual gain, then more power to you. I think that’s the part of your Comment to start with.

Beyond that, though, I do think you might find this article interesting…

https://bestinterest.blog/why-cant-i-take-social-security-early-and-invest-it/

Only a max of 85% of Social Security Benefits are taxed. Since this is a kind of tax advantaged income, how does this part play in the calculation of delaying social security benefits to age 70 when your expected marginal tax rate is 22% in retirement?

Hi Raghu – yes, up to 85% of Social Security is taxable.

The specific tax rate, though, might be 22% for you, 12% for someone else, 32% for someone with large IRA withdrawals, etc. etc.

Sounds like you’re asking about a specific interaction between Social Security and taxes. My recommendation to you would be to create a complete financial plan and then toggle the hypothetical Social Security age.

Excellent article! Great advice, well laid out, presenting both sides of the argument. Dang, you’re good at this (and, thanks for the tip not to Google “Sugar Daddy”!)

Fritz!! Haha thank you much, sir. Always gotta be careful what we’re googling these days 🙂

Jesse, I already am planning to work til 70, and am the higher wage earner. My wife is 2 years younger. My wife stayed at home with our kids, but worked enough to qualify for SS benefits, but her benefits are about 1/4 of my PIA.

My understanding is that spousal benefits are reduced if she starts collecting her own SS before her full retirement prior to switching to spousal benefits. If she starts collecting at 65, she will get 42% of my PIA; 46.2% at age 66, and 50% if she waits til age 67. Am I understanding that correctly? I am using this to calculate what makes sense for when she should start taking SS. We are both in great shape, with parents who lived into the 90s.

When I run the numbers, the best outcome is to wait for her to collect till age 67. The break even point is somewhere around age 73-74. I think this is the case because her own primary benefit is much smaller than mine.

Thanks for all your work! I really enjoy your podcasts!

Hi Ray,

Yes, what you’re saying all makes sense to me.

Based on your wife’s much smaller PIA, it is wise for you to consider the SPOUSAL benefit. I found some data (which seems plausible) stating that out of the ~74 million Americans receiving some form of Social Security, about 1.9 million are doing so via the SPOUSAL benefit. In other words – you and your wife are in the relatively small corner case. Good for you for recognizing that!

It does not surprise me that the optimization calculators recommend her to wait until “maximum SPOUSAL age” – or 67 – before collecting. That makes sense to me.

Thanks for the kind words!

Jesse