Don’t miss an episode of our podcast, Personal Finance for Long-Term Investors. Available on all podcast players.

Here’s the latest episode:

Paul wrote in and said:

I’m years away from RMDs, but all the bad stuff that comes with them makes me worry….

Forced to withdrawal more than I need, withdrawal rates that start too high and just keep going up, trigging higher taxation of Social Security, increasing IRMAA Medicare rates, no more stretch provision for heirs.

But a particular fear is self-inflicted sequence of returns damage. I re-balance in May. As part of that, I figure that’s when I’ll take my RMD.

Let’s say my IRA balance was $1M as of 12/31. However, the market dropped 30% in February and it has not recovered.

I’m forced to calculate my RMD against a balance that doesn’t even exist anymore. My balance is down to 700k. Conceivably, this could happen many times over 20+ years. The RMD might force me to withdraw 5% or 6%, when (if I were in control) a guardrail approach might only suggest 2% for that year.

Basically, when there’s a hole in the boat, best to not make it any bigger.

I find this scenario very troubling.

Paul outlines a fascinating and possibly scary concern.

Do required minimum distributions (RMDs) have a destructive synergy with the sequence of returns risk? Can this combo “sink your boat?”

Let’s dive in. I’ll add some color and explanation to Paul’s question, walk you through my thoughts, and ultimately leave you with a solid plan of how to mitigate (or even avoid) these bad outcomes in your retirement.

Basics – RMDs, Sequence Risk, and Other Concerns

First, I would like to provide some background on Paul’s question so that you can fully understand what he’s asking.

Required minimum distributions, or RMDs, are mandatory withdrawals you must take each year from certain tax-deferred retirement accounts (like traditional IRAs and 401(k)s) starting at age 73, age 75, or possibly other ages pending future legislation. The RMD amount is based on your account balance and remaining life expectancy. Just like other withdrawals from tax-deferred accounts, RMDs are taxed as ordinary income.

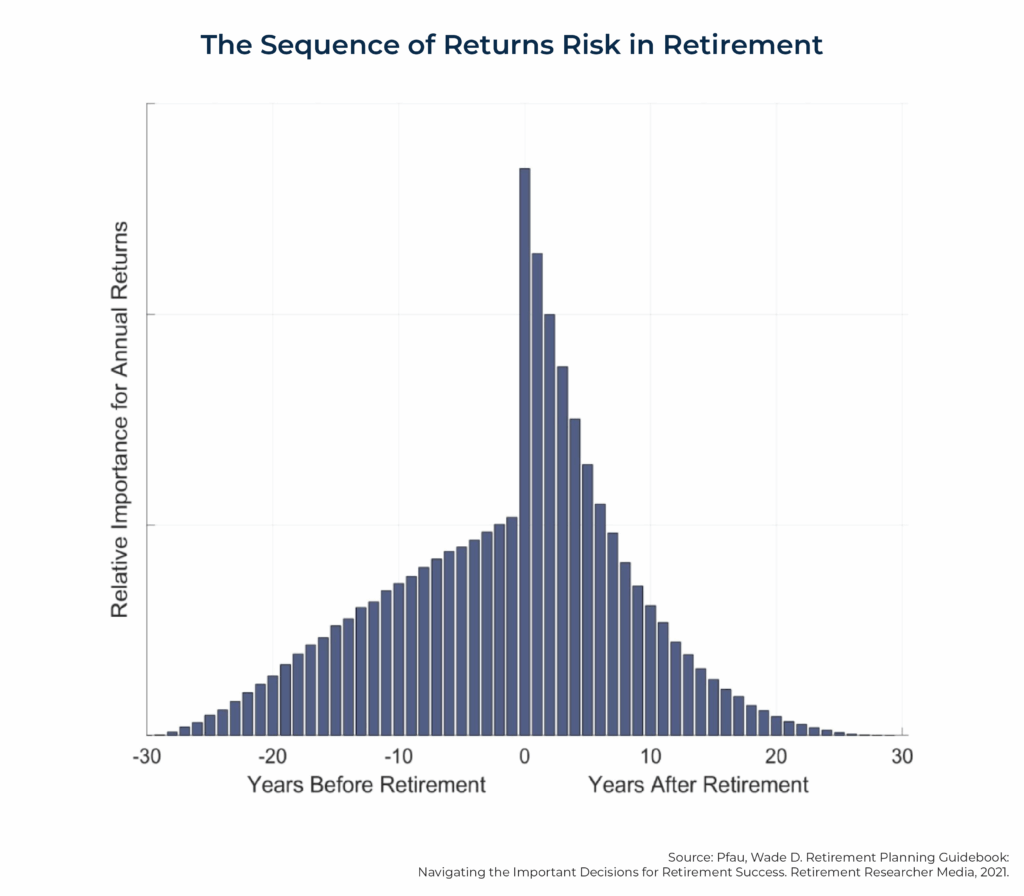

The sequence of return risk states the following: not only does the magnitude of investment returns matter, but the sequence of those returns matters as well. Specifically, a particularly poor series of investment returns during the early years of retirement can permanently damage and derail a long-term retirement plan.

To learn more about the sequence of return risk, tune into Episode 87 of Personal Finance for Long-Term Investors:

Paul, who asked the question, outlines a couple of other concerns too. I’ll explain them below, but won’t dive much deeper.

- Higher taxation of Social Security**. Depending on your total income, only a portion of your Social Security income is actually taxable. Granted, these income brackets are relatively low. For example, a married couple earning $44,000 (or more) is in the highest of these brackets, and 85% of their Social Security is taxable****.

- IRMAA surcharges. IRMAA (Income-Related Monthly Adjustment Amount) is a Medicare premium surcharge imposed on higher-income beneficiaries in addition to their standard Medicare Part B and Part D premiums. The amount of IRMAA is determined based on an individual’s modified adjusted gross income (MAGI) and can result in higher healthcare costs for those with higher incomes.

- No more “stretch provision” for heirs. In short, the rules for withdrawing inherited IRA moneys used to be very beneficial for heirs, allowing them to keep large amounts of money growing tax-deferred for decades. Now, however, the 10-year rule mandates inherited IRAs are emptied in 10 years. No more “stretching” the withdrawals for decades.

**I’m still digesting the July 2025 tax bill (Big / Beautiful), and it does have a specific deduction for people 65+ on Social Security. I will return / addend /edit this once I’ve learned more.

****Note – “85% taxable” is much different than “taxed at an 85% rate.” Instead, it means that 15% of SS income is tax-free, while the other 85% is taxed at one of the Federal income tax rates (10%, 12%, 22%, etc.).

For both the Social Security and IRMAA concerns, RMDs can be negative. RMDs can lead to higher Social Security taxability and result in higher tax rates on that Social Security income, as well as higher IRMAA surcharges. All are possible.

But this is where forethought in your financial plan can pay huge dividends. It won’t always be possible to avoid extra taxes and surcharges, but a prudent plan thinks about these questions ahead of time.

I want to focus the remainder of this article on Paul’s primary concern: can RMDs combine with sequence of returns risk to torpedo your retirement, all completely out of your control?!

RMDs + Sequence Risk: Terrible? Or Merely Worth Being Aware Of?

You should be aware of how RMDs and sequence risk can negatively interact. But with proper planning, you can turn this “perfect storm” into a passing rain shower.

Sequence of Returns Exists With or Without RMDs

The sequence of returns risk is omnipresent for stock market investors, whether they are taking RMDs or not. Three principal ingredients can turn the sequence of returns risk into a real danger:

- Your withdrawal rate,

- The returns from the market,

- And where you are in your retirement/withdrawal timeline (earlier is worse for you)

It’s a bit like a fiery explosion. It requires fuel, oxygen, and a spark. If you’re missing one of those key components, you won’t get an explosion.

To that end, RMDs only matter if they increase your overall withdrawal rate. For some retirees, RMDs will do just that. But for other retirees, RMDs might not increase their withdrawal rate at all. Instead, RMDs will simply shift which account(s) they are taking most of their withdrawals from.

Sequence Risk Usually Dissipates by RMD Age

The two investors in the chart below have the same returns, but in a different sequence. They make the same withdrawal amounts each year. But look at the difference in their final portfolio value!

It’s $105,944 vs. $35,889. That’s a 300% difference over only 15 years!

Even though the “blue” investor experienced a bad sequence of returns in years 11 through 15, it barely affects them.

The “green” investor, who suffered those same returns in Years 1 through 5, got decimated.

The lesson is clear: the sequence of returns risk has much greater impact during the early years of retirement. The underlying math is simple. During the early years of poor returns, each withdrawal (in this case, a fixed $5,000 withdrawal) requires us to sell a larger number of shares, leaving behind fewer shares to participate in any future market recovery.

But will this matter by the time our RMDs start?

Based on current legislation, RMDs will start at:

- Age 73, if you’re born between 1951 and 1959

- Age 75, if you’re born in 1960 or later

- And yes, this might change in the future

Depending on where you look, the average retirement age in the U.S. falls between age 62 and age 65. Meaning RMDs won’t kick in until ~10 years into retirement.

Most of the sequence of returns risk will have dissipated by that point.

Asset Allocation Helps (Everyone)

Whether you’ve hit RMD age or not, proper asset allocation plays a pivotal role in mitigating the sequence of returns risk.

Short-term needs –> low-risk assets.

It’s one of the most frequent Bibles I thump here.

Roth Conversions (Can Be) a Massive Help

I’ve written at length about Roth conversions, and I highly recommend you read these two articles if you’re unfamiliar with the topic:

Roth conversions can play a significant role in mitigating the risk of RMDs combining with sequence of returns.

Why?

Because every dollar you convert to Roth becomes one less dollar that will be subject to future RMDs. The key is that you must start many years before your RMD age hits.

Even if your Roth conversion yields zero tax benefit, you can still choose to move those dollars away from the RMD crosshairs.

Roth conversions can also be an excellent tool for planning around IRMAA surcharges.

Taking RMDs All at Once?!

In the original question, Paul mentions his plan to take RMDs in May, as that’s when he performs his annual rebalancing.

This is a choice, not a rule. And this choice magnifies Paul’s risk.

I recommend that you consider spacing out your IRA withdrawals. Perhaps monthly, or quarterly.

Think of it as dollar-cost averaging out of your account. I’ve heard this referred to as “diversifying through time,” and it’s a perfect description. By diversifying across time, we decrease our exposure to sudden market events.

Imagine, for example, if you were forced to withdraw a large sum in April 2025, after the tariff announcement?! Not good.

…Or RMD in Early January

If the risk of RMDs plus the sequence of returns is really sticking in your craw, just take your RMD as early as possible.

Your RMD is calculated based on your IRA value(s) on December 31 of the prior year.

Let’s not even give the market a chance to crash! Just take the RMD right away in January.

Stay Invested

There’s no reason why you can’t take your RMD, withhold the taxes, and then take the remainder and immediately reinvest that money (say, in a taxable account).

The sequence of returns risks really applies to situations where you withdraw money forever and spend it, depleting your investable assets by 4 or 5 or 6% in the middle of a down market.

However, with RMDs, yes, you might have to withdraw 4 or 5 or 6% from your Traditional tax-deferred assets, but that 4 or 5 or 6% doesn’t just disappear. You need to set aside perhaps ~20-30% of the RMD to pay federal and state taxes, but the remainder can be reinvested.

Conclusion

In conclusion, it is good for Paul to think this far ahead. 99% of retirees would NOT have the foresight to do so.

That said, I think if you apply some of the tactics and strategies I’ve outlined above, the true impact of RMDs + Sequence Risk will be more negligible than you think.

What are your thoughts?

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

Good thoughts Jesse on ways to mitigate this risk.

One thing not mentioned here is the main weapon that we have against sequence risk – proper asset allocation. Just like any other planned withdrawal, if the money is coming out soon, and you need to spend it, it shouldn’t be invested in equities. The RMD’s for at least the next 3-5 years should be in cash and bonds. Then you have no equity selling during this downturn.

If this money is invested for your heirs because you don’t need it. Then just reinvest it as you mentioned.

Thanks for writing in, Aaron!

I have taxable and IRA accounts at schwab

when I do my rmd I transfer securities from by IRA to my taxable account

I just need cash to pay the taxes

the cash accumulates through the year from dividens and interest

I do not have to sell securities to meet my rmd

been taking my rmd for 5 years

Hi John – yessir, you take your RMDs “in kind.”

“Staying invested” is a terrific way to avoid the risks discussed in the article.

I believe it’s mathematically equivalent to selling the shares, taking the cash, then using that cash to re-buy in your taxable account.

Jesse,

Conversion to Roth is not the best answer in some cases. I am 79 and am not willing to risk being around for 5 more years to make the Roth viable. Rather, I withdraw some amount over the RMD (in good years) and put it into a brokerage account with a money market fund and broad ETF. I pay taxes, but I would on Roth convesions anyhow. This method allows me to control my tax rate and have funds available if needed, though unlikely save for desired big purchases. Living on SS and RMDs is comforatble and withdrawing a little more than RMD povides some cushion for unexpected expenses or fun!

Joe B.

Hi Joe – I could have been more clear in the article, but Roth conversions only help here for people *before* their RMD age.

The point is to execute Roth conversions during your early retirement, lower income years. Not only will the Roth conversion create a positive tax arbitrage for this person, but it will also reduce their future exposure to any “RMD + Sequence of Returns” type risk.

Once you’re in the middle of RMDs, Roth conversions don’t effectively do much for you.

I have created some guardrails for avoiding Sequence of Return Risk. If I am risk averse, I keep 12 years of net expenses in fixed income investments. If I am a risk taker, I keep 4 years of net expenses in fixed income investments. The fixed income allocation is the safety ballast which I draw upon when having to take withdraws from my tax deferred accounts when my equity allocation is down. This has served me well.

Hey Doug –

That’s it! You’ve certainly created a great buffer against sequence risk. As you know, nothing in the financial planning world is free and everything has a tradeoff. Your porfolio might lag behind some other “high risk” portfolios in the long run, but you’re sheltered yourself against many of the volatilites they’ll be exposed to.

I’m new to reading your blog, so I haven’t read anything you’ve written except for the initial articles you sent me in your “Welcome” package.

But as a long time investor and Tax Practitioner, I have to say, respectfully, that I found some parts of your response to Paul’s question problematic, not especially helpful, and a bit disappointing.

For example, taking more frequent distributions can expose a IRA Owner taking RMDs to MORE sequence risk if market returns are poor, i.e., ‘Dollar Lost Averaging’ instead of Dollar Cost Averaging.

Also, saying that “Sequence risk usually dissipates by RMD age” is flat wrong, IMO. At age 73, or even 75, there’s still plenty of damage that can be done to a retirement horizon that still has 15 to 25 years yet to play out. Moreover, the years prior to your IRA RBD add additional potential to be exposed to SORR for someone who retires between 65 or 67, or even as late as age 70.

Lastly, Doug’s idea to use Fixed Income assets, which can and probably should include Cash and Short-term Bonds that offer buffer protection from SORR while also providing for several years of spending needs is an excellent approach, IMO. As Paul says, the number of years of expenses one dedicates to Fixed Income assets depends on his/her Risk Tolerance and Strategic Asset Allocation. For you to say (I’m paraphrasing): “Well, that’s true but your Investment Portfolio’s returns might lag behind some other ‘higher risk’ portfolios” doesn’t adequately recognize, IMO, that Paul was making clear with the explanation to his question that one of his most important Strategic Investment Objectives when he retires is likely to be Preservation of Capital. If so, there’s obviously going to be some tradeoff on long-term investment returns, as you rightfully pointed out, meaning that Growth of Capital (i.e., Capital Appreciation) might need to be his Secondary or even Tertiary Strategic Investment Objective if Paul adopts the Buffer Assets methodology suggested by Doug to get him through and beyond the years immediately preceding his retirement and his first several years of RMDs.

Depending on his Risk Tolerance and investment experience, Paul might consider allowing for a Rising Equity Glide Path as Michael Kitces and Wade Pfau have researched. If long-term stock market returns are favorable, the Rising Equity Glide Path could provide some additional long-term growth in his Investment Portfolio in the later years of his retirement. But the Rising Equity Glide Path approach is still subject to being impacted by a large market drawdown, so keeping some cash (or periodically taking stock market gains and moving them into cash to fund his RMDs as he grows older) is still a prudent and viable option. An old saying goes something like this: “No one ever went broke by taking their gains!” To the heart of Paul’s question, it’s the losses that can do you in.

This is just my two cents worth. I apologize for the lengthy response. I won’t make a habit of it, and no offense is intended by anything I’ve written.

Managing Sequence Risk is a tricky proposition that’s quite important when an investor is decumulating the nest egg they worked so hard and long to built.

Hi Ritch – thanks for writing in.

All good, all good. I don’t take offense to anything you’ve written. Please extend the same grace to me below 🙂

Re: “dollar lost averaging” – being exposed to *more* sequence risk there is a simple misunderstanding of the underlying market data and math. Averaging over time, by definition, reduces market timing risk. This applies whether averaging in or averaging out. If you can show me backtested data stating otherwise, I’m all ears.

Re: “sequence risk usually dissipating by RMD age is flat wrong.” Again – the historical data here actually shows that you’re wrong. Why? Because if you’ve retired at, say, age 65 (like you’ve suggested), and you’ve made it through to age 73 without yet suffering SORR, then (by definition) you’ve had reasonable market returns over those first 8 years of retirement! And therefore, by definition, you’ve circumvented the highest risk years for SORR! Which means most of SORR is dissipated.

It’s *SEQUENCE* of returns risk. Just because you have some bad returns at age 73, 74, 75…that doesn’t mean that your SEQUENCE of returns was bad during your early years of retirement.

SORR & RMDs matters most for the retiree who begins retirement immediately prior to RMD age, or even during RMD age. It matters most to the retiree who pulls the trigger at 72.

If you retire at age 65, abide by the 4%-ish rule, and make it to age 73 without suffering SORR, then your portfolio has likely GROWN significantly over those previous 8 years. Again – this means most of SORR is gone.

Good info. I retired in 2023, so in terms of the market I’m faring pretty well so far. My RMD’s don’t begin until I’m 75 in 2035, but I just created my RMD worksheet with AI, and realizing in what appears to be a tax torpedo I’m facing in 10 years. Anyway, your newsletter just popped up in my email this morning, so you have a new follower.

That’s awesome! Thanks Vince.