Reader-of-the-blog Jim writes in:

I’ve max’d out my Roth IRA every year since 2020 by putting in the full $6000 at the beginning of January. I just buy VTSAX* with it all.

As I write this email, those shares of VTSAX are at $18,100. I’ve gained $100 over three years. I would have been better off sticking the money in a bank account gaining 1% per year.

Tell me I didn’t make a big investing mistake?!

-Jim

*Note – VTSAX is Vanguard’s Total Stock Market Index Fund. It’s an efficient, low-cost, diversified method of getting exposure to the entire stock market.

Thanks Jim. Great question. You’re not the only one asking this in 2022. So let’s get into some answers.

Would you rather listen to this? I discuss this article in Episode 40 of Personal Finance for Long-Term Investors (formerly The Best Interest Podcast), below.

Results-Oriented Thinking

First, we need to know more about Jim. Based on his age, his goals, his timelines, his income...based on his personal finance circumstances…was this the correct investment approach?

I know Jim is young-ish, so I’m inclined to say that 100% stocks was, at least, reasonable for him.

But we shouldn’t say:

- If the investment goes up, it was smart.

- If the investment goes down, it was dumb.

That’s results-oriented thinking. It’s one of the hallmarks of irrational investing. I rail against it here on The Best Interest.

Further reading on results-oriented thinking:

If Jim is 25, then he has 34 years before he can withdraw the profits from his Roth IRA investments. Based on that, 100% VTSAX is perfectly reasonable.

But a 3-year timeline is too short for worry, celebration, or any other emotion. If you recall, stock market money should have an 8+ year timeline associated with it.

So those are points #1 and #2 – Jim, you can’t judge this investment based solely on performance, especially after such a short timeline.

We know that US stocks have, on average, returned ~7% per year (accounting for dividends and inflation). Jim’s portfolio has underperformed that average (more on this below). But as students of the stock market, we also know that stocks are volatile, rarely nailing the 7% average in a given year.

Total Return?

Next: Jim is overlooking dividends.

As we’ve discussed on The Best Interest, stocks are businesses. Stockholders are business owners. When those businesses profit, stockholders can receive a share of profits via dividends. And Jim should have been receiving those dividends.

Jim is only looking at the price appreciation of his investment. But total investment return combines both price appreciation and dividends/income.

Sure enough, he’s received $557 in dividend payments over the past 2.5+ years. Not huge, but not bad! That cash, Jim, is probably sitting in your Roth IRA account. Invest it!

When we account for these dividends, we can calculate Jim’s internal rate of return (IRR) as 2.3% per year.

It’s not terrific. But it’s better than Jim had assumed. Dividends matter.

Long-Term Investing Fundamentals

Since Jim is investing in his Roth IRA, we know retirement is one of his savings goals. That’s a long-term goal and requires a long-term mindset. Remember – “when in doubt, zoom out.”

Long-term investing involves many investments over many years. This is called dollar-cost averaging.

My personal example of dollar-cost averaging is that I’ve invested $500 into my Roth IRA every month for the past 5+ years. Whether the market was up, down, or sideways, I still invested the same $500.

Why?

- First, it’s logistically easy to automate.

- Second, it’s psychologically easy.

- And third, it will work well enough for me to hit my financial goals over the next three decades. I don’t need to perfectly time the market. DCA is good enough.

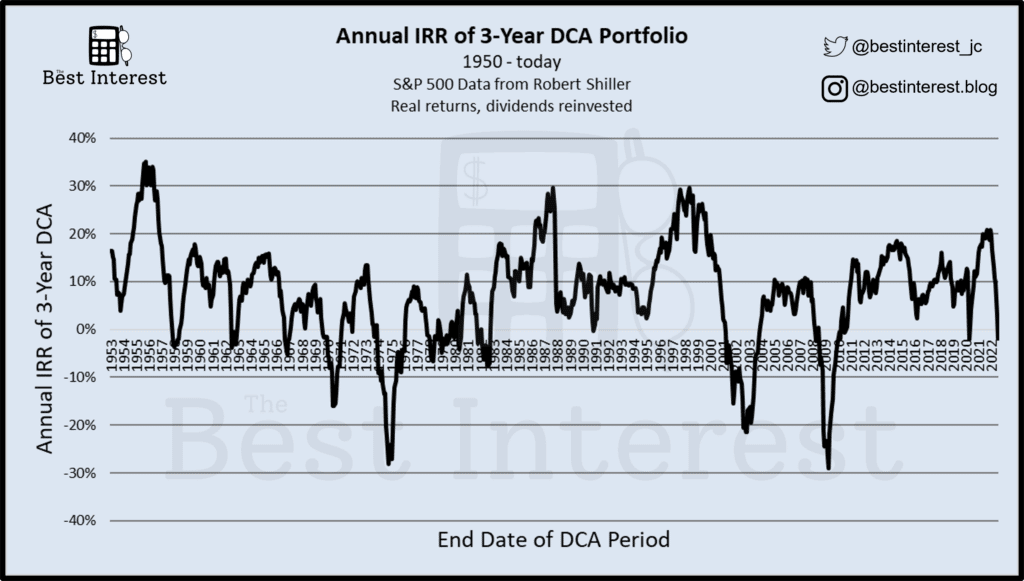

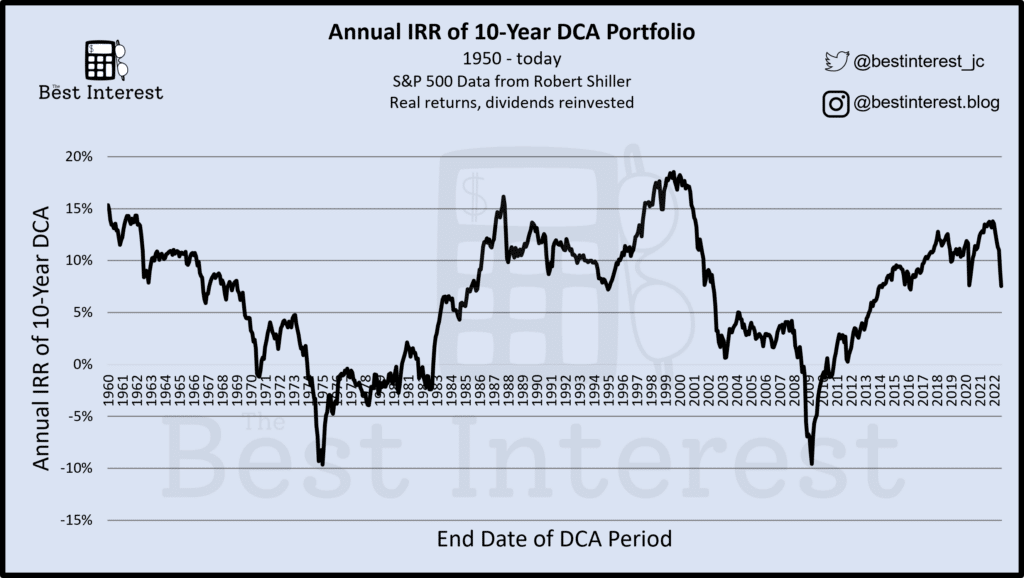

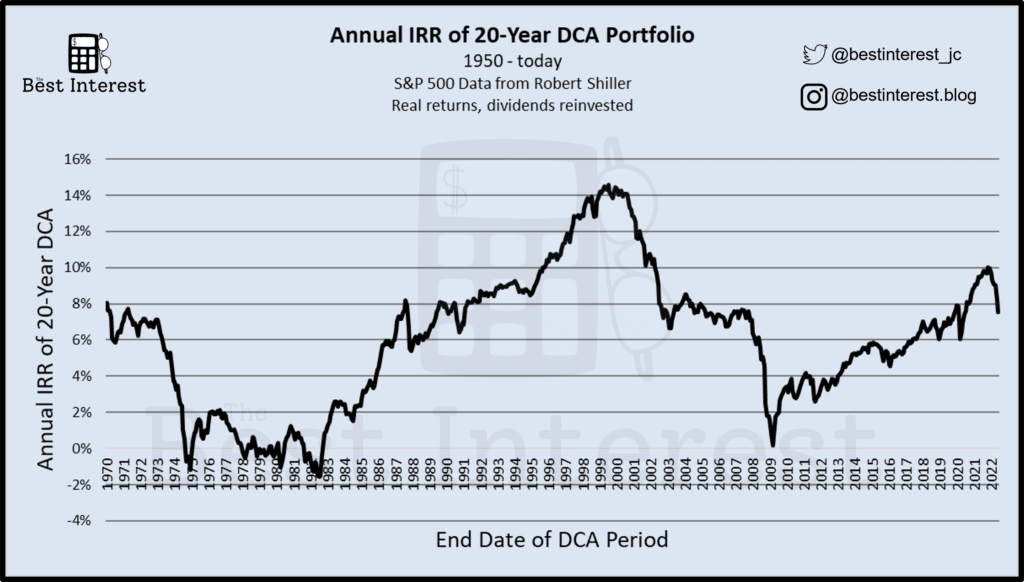

History tells us, though, that dollar-cost averaging (like all stock investing) doesn’t work perfectly over short time periods. Below are three charts, looking at internal rates of return (IRR) over various DCA periods. Shorter periods, quite clearly, have regularly suffered negative returns.

Even longer periods have suffered periods of negative return or no return.

But importantly, time tends to narrow the range of expected outcomes. That’s the important point here. Jim’s three-year period has a wide range of expected outcomes, within which +2.3% per year is quite reasonable.

Bigger Fish

A couple weeks ago, I wrote about the hedonic treadmill. We always want more, more, more. In terms of our desire, there will always be a bigger fish.

The same goes for investments.

There will always be a better investment. There is one stock that will have the best performance today. There is one stock that will have the best performance this month. There is one asset class that will have the best performance this year. Etc, etc.

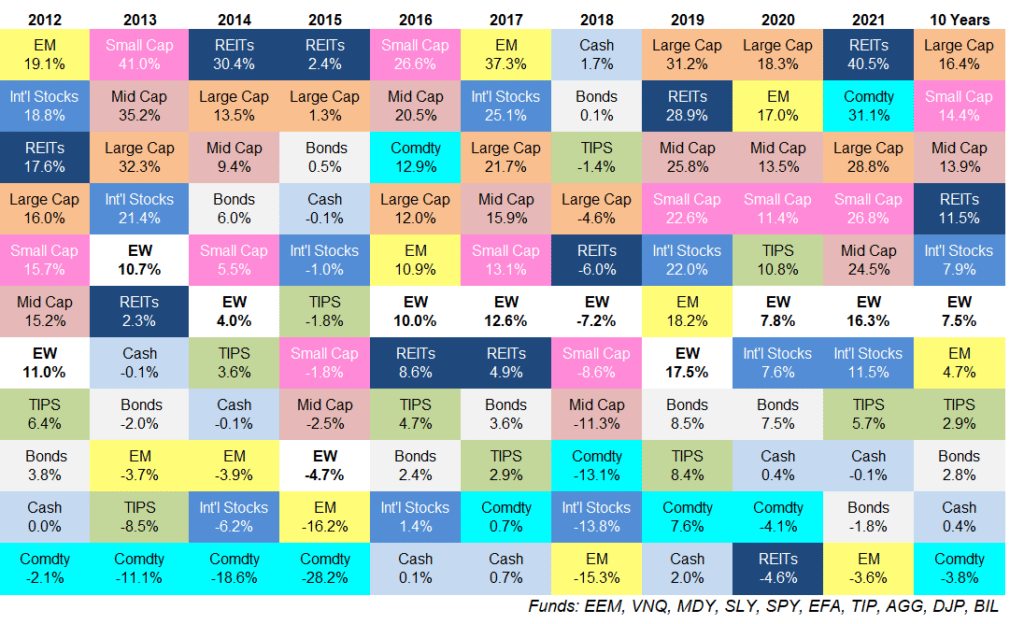

And the “best thing” changes over time. The quilt chart above shows how various asset classes ebb and flow yearly.

It’s not your job to find the best investment every day. You only need to build a portfolio that meets your goals, preferably with the least risk possible. “Good enough” is, quite literally, good enough.

By the time Jim is 59, will today’s investing decisions help him meet his goals with the least risk possible? That’s the question I’m asking, and I think that’s what Jim should be asking.

From my vantage point, there is nothing wrong with investing $18K in the stock market with a 30+ year timeline attached.

Jim – thanks for the question. I hope this helped.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!