A note from a dedicated reader inspired today’s article. It’s a question about the stock market and investing at all-time highs. It reads:

Hey Jesse. So, back in March 2020 you said that you were going to keep on investing despite the major crash. Fair enough, good call!

Note: here and here are the two articles that likely inspired this comment

But now that the market has recovered and is in an obvious bubble (right?), are you still dumping money into the market?

Thanks for the note, and great questions. You might have heard “buy low, sell high.” That’s how you make money when investing. So, if the prices are at all-time highs, you aren’t exactly “buying low,” right?

I’m going to address this question in three different ways.

- General ideas about investing

- Back-testing historical data

- Identifying and timing a bubble

Long story short: yes, I am still “dumping” money into the stock market despite all-time highs. But no, I’m not 100% that I’m right.

General Ideas About Investing at All-Time Highs

We all know that that investing markets ebb and flow. They go up and down. But, importantly, the stock market has historically gone up more than it has gone down.

Why does this matter? I’m implementing an investing plan that is going to take decades to fulfill. Over those decades, I have faith that the average—the trend—will present itself. That average goes up. I’m not betting on individual days, weeks, or months. I’m betting on decades.

It feels bad to invest right before the market crashes. I wouldn’t enjoy that. But I’m not worried about the value of my investments one month from now. I’m worried about where they’ll be in 20+ years.

Allowing short-term emotions—e.g. fear of an impending crash—to cloud long-term, math-based thinking is the nadir of result-oriented thinking. Don’t do it.

Don’t believe me? Here’s a fun idea. Google the term “should I invest at all-time highs?”

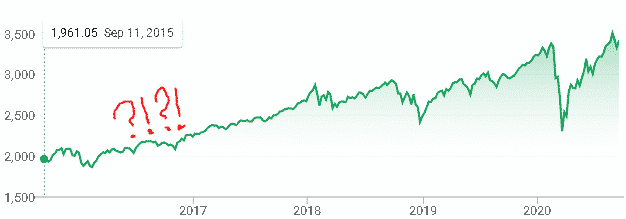

When I do that, I see articles written in 2016, 2017, 2018…you get it. People have been asking this question for quite a while. All-time highs have happened before, and they beg the question of whether it’s smart to invest. Here’s the S&P 500 data from 2016 to today.

So should you have invested in 2016? In 2017? In 2018? While those markets were at or near all-time highs, the resounding answer is YES! Investing in those all-time high markets was a smart thing to do.

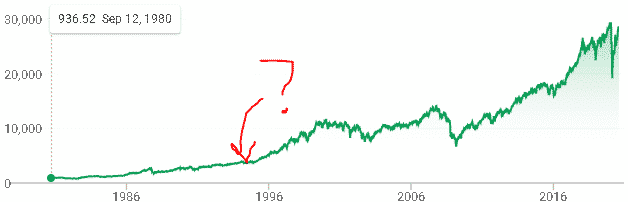

Let’s go further back. Here’s the Dow Jones going back to the early 1980s. Was investing at all-time highs back then a good idea?

I’ve cherry-picked some data, but the results would be convincing no matter what historic window I chose. Investing at all-time highs is still a smart thing to do if you have a long-term plan.

Investing at all-time highs isn’t that hard when you have a long outlook.

But let’s look at some hard data and see how the numbers fall out.

Historical Backtest for Investing at All-Time Highs

There’s a well-written article at Of Dollars and Data that models what I’m about to do: Even God Couldn’t Beat Dollar-Cost Averaging.

But if you don’t have the time to crunch all that data, I’m going to describe the results of a simple investing back-test below.

First, I looked at a dollar-cost averager. This is someone who contributes a steady investment at a steady frequency, regardless of whether the market is at an all-time high or not. This is how I invest! And it might be how you invest via your 401(k). The example I’m going to use is someone who invests $100 every week.

Then I looked at an “all-time high avoider.” This is someone who refuses to buy stocks at all-time highs, saving their cash for a time when the stock market dips. They’ll take $100 each week and make a decision: if the market is at an all-time high, they’ll save the money for later. If the market isn’t at an all-time high, they’ll invest all their saved money.

The article from Of Dollars and Data goes one step further if you’re interested. It presents an omniscient investor who has perfect timing, only investing at the lowest points between two market highs. This person, author Nick Maggiulli comments, invests like God would—they have perfect knowledge of prior and future market values. If they realize that the market will be lower in the future, they save their money for that point in time.

What are the results?

The dollar-cost averager outperformed the all-time high avoider in 82% of all possible 30-year investing periods between 1928 and today. And the dollar-cost averager outperformed “God” in ~70% of the scenarios that Maggiulli analyzed.

How can the dollar-cost averager beat God, since God knows if there will be a better buying opportunity in the future?

Simple answer: dividends and compounding returns. Unless you have impeccable—perhaps supernatural—timing, leaving your money on the sidelines is a poor choice.

Investing at all-time highs is where smart money plays.

Enjoying this article? Subscribe below to get new articles emailed straight to your inbox

Identifying and Timing a Bubble – The Hard Part About Not Investing at All-Time Highs

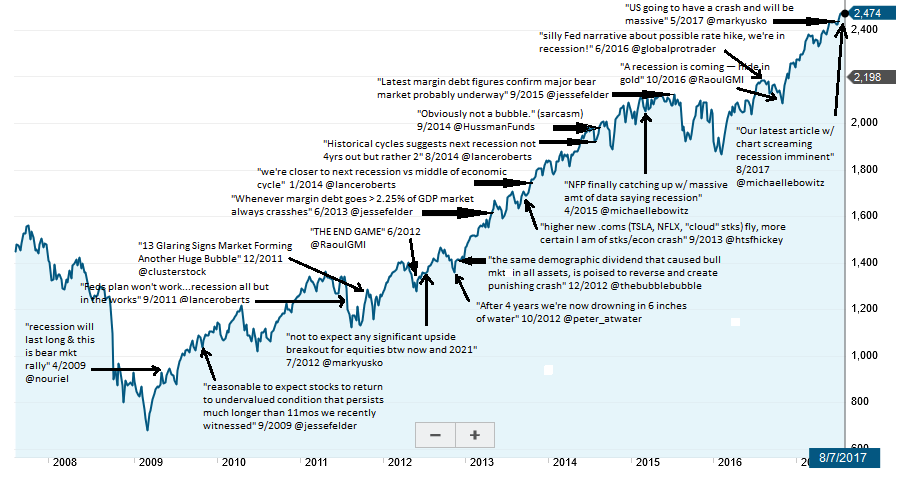

One of my favorite pieces of finance jargon is the “permabear.” It’s a portmanteau of permanent and bear, as in “this person is always claiming that the market is overvalued and that a bubble is coming.”

Being a permabear has one huge benefit. When a bubble bursts—and they always do, eventually—the permabear feels righteous justification. See?! I called it!

The Best Interest reader Craig Gingerich jokingly knows bears who have “predicted 16 of the last 3 recessions.”

Suffice to say, it’s common to look at the financial tea leaves and see portents of calamity. But it’s a lot harder to be correct, and be correct right now. Timing the market is hard.

Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.

Peter Lynch

Predicting market recessions falls somewhere between the Farmers’ Almanac weather forecast and foreseeing the end of the world. It takes neither skill nor accuracy but instead requires a general sense of pattern recognition.

Note: The Farmers’ Almanac thinks that next April will be rainy. Smart prediction, guys. And I, too, think the world will end—at least at some point in the next few billions of years.

I have neither the skill nor the inclination to identify a market bubble or to predict when it’ll burst. And if someone convinces you they do have that skill, you have two options. They might be skilled. Or they are interested in your bank account. Use Occam’s Razor.

Just remember: some permabears were screaming “SELL!” in late March 2020. I’ve always heard “buy low, sell high.” But maybe selling your portfolio at the absolute market bottom is the new secret technique?

“But…just look at the market”

I get it. I hear you. And I feel it, too. It feels like something funny is going on. Investing at all-time highs right now feels…wrong.

The stock market is 12% higher than it was a year ago. It’s higher than it was before the COVID crash. How is this possible? How can we be in a better place mid-pandemic than before the pandemic?

One explanation: the U.S. Federal Reserve has dropped its interest rates to, essentially, zero. Lower interest rates make it easier to borrow money, and borrowing money is what keeps businesses alive. It’s economic life support.

Of course, a side effect of cheap interest rates is that some investors will dump their cheap money into the stock market. The increasing demand for stocks will push the price higher. So, despite no increase (and perhaps even a decrease) in the intrinsic value of the underlying publicly traded companies, the stock market rises.

Is that a bubble? Quite possibly. But I’m not smart enough to be sure.

The CAPE ratio—also called the Shiller P/E ratio—is another sign of a possible bubble. CAPE stands for cyclically-adjusted price-to-earnings. It measures a stock’s price against that company’s earnings over the previous 10-years (i.e. it’s adjusted for multiple business cycles).

Earnings help measure a company’s true value. When the CAPE is high, it’s because a stock’s price is much greater than its earnings. In other words, the price is too high compared to the company’s true value.

Buying when the CAPE is high is like paying $60K for a Honda Civic. It doesn’t mean that a Civic is a bad car. It’s just that you shouldn’t pay $60,000 for it. Some say that investing at all-time highs is like buying that overpriced car.

Nobody is saying that Apple is a bad company, but its current CAPE is 52. Try to find a CAPE of 52 on the chart above. You won’t find it.

So does it make sense to buy total market index funds when the total market is at a CAPE of 31? That’s pretty high and comparable to historical pre-bubble periods. Is a high CAPE representative of solid fundamentals? Probably not, but I’m not sure.

My Shoeshine Story – Investing at All-Time Highs 2020s Edition

There’s an apocryphal tale of New York City shoeshines giving stock-picking advice to their customers. Those customers happened to be stockbrokers. Those stockbrokers took the advice as a sign of an oncoming financial apocalypse.

The thought process was: if the market was so popular that shoe shines were giving advice, then the market was overbought. Even dumb people thought they could make money. Smart money, therefore, should sell into the wild demand.

I recently heard a co-worker talking about his 12-year old son. The son uses Robin Hood—a smartphone app that offers free stock trading to its users. Access to the stock market has never been easier.

According to his dad, the kid bought $100 worth of Advanced Micro Devices (ticker = AMD). When asked what AMD produces, the kid said, “I don’t know. I just know they’re up 60%!”

This, an expert might opine, is not indicative of market fundamentals.

But then I thought some more. How is this different from how I invest?

“What does your index fund hold, Jesse?”

Well…a lot of companies I’ve never heard of. I just know it averages ~10% gains every year!

My answer is eerily similar to the kid’s answer! Especially so when investing at all-time highs.

I’d like to believe that I buy index funds based on fundamentals. And I believe that fundamentals are justified by historical precedent. But what if the entire market’s fundamentals are out of whack?

I’m buying a little bit of every stock. But what if every stock is F’d up?

Closing Thoughts

Have you ever seen an index zealot transmogrify into a permabear?

Not yet. Not today.

I do understand why some warn of a bubble. I see the same omens. But I don’t have the certainty or the confidence to act on omens. It’s like John Bogle said in the face of market volatility:

Don’t do something. Just stand there.

John Bogle

Markets go up and down. The U.S. stock market might crash tomorrow, next week, or next year. Amidst it all, my plan is to keep on investing. Steady amounts, steady frequency. I’ve got 20+ years to wait.

History says investing at all-time highs is still a smart thing. Current events seem crazy, but crazy has happened before. Stay the course, friends.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

Jesse,

I happened to have written about just this topic very recently. It’s wild how that even as we target specific indexes in order to reach specific investment targets with underlying expectations, we manage to muck it up all too often. That’s because of our decisions (talking about market timing for example, or diversification mistakes). That’s our behavior gap that we create within our investing decisions. Our own expense ratio.

What I found interesting about the data in my own analysis was that even perfect market timing didn’t really beat dollar-cost averaging by very much, and perhaps most interestly, simply investing immediately any sums of money you have available for investment winds up beating out dollar-cost averaging most of the time. That of course ignores the inherit risk to dumping a lump sum in and then having a crash the next day, but statistically immediate investing wins out by just a tiny bit.

Timing the market in the worst possible way (buying at the high of each year over a 20 year period) didn’t really hold folks back all that much. Time in the market!

Hey again Chris. Haha that’s funny. I’ve added your article onto my reading list!

I don’t know if you had a chance to read my “Viral Stock Market Strategies” post that I linked to above? It covers some of the same DCA vs. lump sum ideas that you mention. Back in February and March, I saw some Twitter ppl saying, “Market’s down 5%–buy, buy, buy!!”

And I thought, “Have you been keeping your money in cash all these years waiting for 5% drops?!”

I’m a big “DCA and chill” guy. As you already know, it means you’ll buy every bottom. It also means you’ll buy right before the bubble bursts. Thems the breaks!! It’ll suck once in a while. You’ll see your most recent 401(k) contribution lose 40% of its value immediately.

But DCA into indexing has the best historical Cramer Ratio out there (investment gains divided by investor’s emotional stress). That’s some Best Interest thinking!!

“Cramer Ratio out there (investment gains divided by investor’s emotional stress)”

Ultimately, that’s what really matters!

Yep, read through your Viral Strategies post, too. Some great analysis around here. 🙂

And yea, I don’t really understand folks who might make an argument that is along the lines of: “but what about if you waited for the market to drop 10% and then made your investments?”.

Like, okay, maybe in a specific circumstance that is indeed better. But what if it only drops 9%? Or if it drops 10% and then another 30%? What do you do then?

To your point the emotional (and mental) weight of all those decision points riding around your head is pretty taxing!

Cheers!

Right on. The whole “what if it drops X%” argument needs to be back-tested against historical markets. That back-test has to come first. If it passes the back-test, then maybe a discussion can ensue. The problem is that none of those “drop X%” algorithms ever pass a back-test.

Why? Because the market always trends *UP* over time.

Waiting for an X% drop will always mean that an investor is missing out on the average upward trend.

So why bother go through the mental exertion and still end up with a losing strategy?

I’m just preaching to the choir here, Chris! All the best.

Great article Jesse

I’ve been DCA in real estate, go to retire from it. The only problem now is that I was in one asset class, hotels. Since last year I have added Apartments and Assisted Living…so, lessons learned due to the pandemic is, invest in different asset classes.

I still need to keep up with the stock market investing ideas, so I can help my daughters.

Hey Pete, that’s really interesting. I’m not much of a real estate investor, and only have a cursory knowledge of it. How do you, personally, purchase your investments? Are they through REITs? Or something other means?

Hello Jesse, sorry for the delayed response…

In 2007 a hotel syndicate was created by a friend’s’ son and 2 other partners, who I started to invest $50K in some of their deals.

I started making more from the passive income than mine and my wife’s income, so we both retired in 2017.

In 2018, with a suggestion from a friend I got licensed to sell these types of products, that was one of the best decisions I made after retirement, it exposed me to other real estate asset classes, which I never knew existed. So, as I get to know the sponsors, I’m now investing in Apartments and Senior Housing and continuing to research other asset classes. In most of these deals, I look for passive income and a growth component. Most of these deals also provides depreciation and long-term capital gain.

If you need additional info, please email me and maybe we can set up a call.

Pete

Thank you for such a crisp explanation. This comes only with a clear thought process, and lots of hard work and preparations. It’s a good indication as to how one should go ahead with his investment for any term.

DCA’er checking in here.

Thanks for putting this post together – it concisely explains mathematically why DCA is a really great way to go mathematically.

For me personally, I find that DCA also lets me have mental reprieve of not having to decide when to invest, and when not to. Likewise, I feel like DCA is a good fit for me because I’m not very good at timing the market. And besides, the market creates all-time highs quite frequently, so using all-time highs as a sell signal isn’t necessarily an accurate way to go.

Great article!

“Markets go up and down. The U.S. stock market might crash tomorrow, next week, or next year. Amidst it all, my plan is to keep on investing. Steady amounts, steady frequency. I’ve got 20+ years to wait.”

In response, what if you have a lump sum of $500K to invest but you are 62 years old and cannot afford a 5+ year recovery horizon from a 30%-40%+ drop? Asking for a friend. 😉

Hi Andrew, many thanks!

As for your friend’s question…

I would first ask your friend, “when in his future will he be SPENDING money from that $500K lump sum??”

The answer to THAT question ought to inform if stocks are an appropriate investment asset or not 🙂

Thank you for your response!

Let’s assume “my friend” would start spending money from the investment in 3-5 years.

Andrew, makes sense. I would send you down the asset/liability matching pathway, at least to start.

It sounds like you don’t need the money for the first 3, 4, 5 years.

But perhaps in years 6, 7, 8 you DO need the money.

As with years 9, 10, 12, 15, etc.

The “problem” is that stocks might not be appropriate for Year 6.

But they are very appropriate for Year 15.

And it might be “in between” in Year 10.

https://bestinterest.blog/asset-liability-matching-aligns-your-money-to-your-future/