Lawrence recently wrote in:

Dear Jesse,

My wife is 70 and I’m about to turn 70, and we’ve been retired for 8 years, and even with the tough market in 2022, our portfolio is up 40% from when we retired – from ~$3M to $4.2M. But I can’t bring myself to spend more…we spend exactly what we want. But I’m now wondering – what if we die with these millions, instead of putting them to some sort of good use?

Ask any retiree or any financial planner who works with retirees. Most retirees struggle to change from “saver” to “spender.” They’ve built decades of strong saving habits. Years of frugality, budgeting, and “buy and hold” investing. You can’t flip that switch overnight.

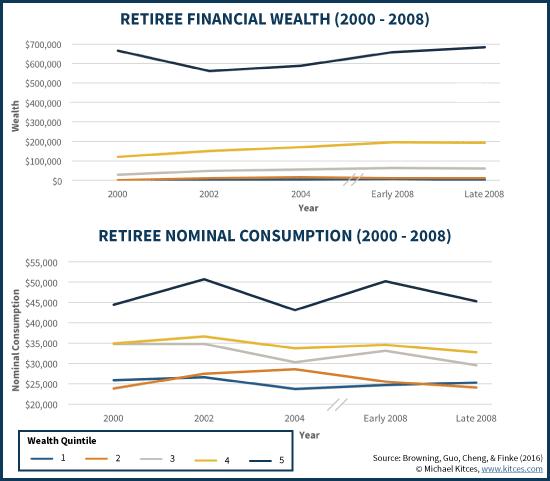

As a real example, check out the chart below. It shows retiree savings going up (surprisingly!) during the 2000s.

- My expectation was that 2000-2008 was a terrible time for retiree portfolios, considering it was the “Lost Decade” in the stock market

- But the reality is that retirees tightened their bootstraps and reduced spending during rough times, ending the 2000s with better portfolios than they started. That’s crazy!

- (Also worth noting – the bottom two quartiles (or lower 40%) of retirees have zero assets. The 3rd quartile has <$100K in assets. That’s scary and a bit sad! Save early, save often, and stay the course.)

Why is this the case? Why do portfolios tend to grow in retirement? Because most of the time, “standard” retirees and retirement planners vastly over-save.

The 4% rule, for example, was created to avoid retirement failure. Running out of money is bad. But here’s an absolutely crazy stat: the 4% rule is more likely to quintuple (or 5x) your retirement portfolio than it is to deplete it.

PS: Here’s a straightforward financial independence and 4% rule calculator where you can input your own data.

The required conservatism to avoid retirement failure is vital in ~5% of test cases. If you saved less, (e.g. a 5% rule, where you retired with 20x your annual spending needs), you’re more likely to fail. For better or worse, retirement planners’ first rule of thumb is the 4% rule.

Outside of the 5% failure cases, however, the 4% rule’s conservatism is overkill. Vast overkill. The kind of overkill that quintuples your money between retirement and death, and makes you realize you should have retired 5-10 years earlier.

Because that’s what we’re talking about here. Lawrence – who has lived off retirement funds for 8 years and seen his nest egg grow from $3 million to $4.2 million – probably could have retired a few years earlier. But it’s too late for that. It’s time he can’t get back.

Further reading:

Now, let’s address Lawrence’s excellent question: What if he dies with these millions, instead of putting them to good use?

- First and foremost: go work with a fiduciary CFP financial planner and (most likely) an estate attorney. You should discuss your options and preferences for this money while you live and after you pass away. How do you want your assets to positively change the world? Who is most important to you? These are the types of questions to ask and answer. Options might include: inheritances, charitable giving, ongoing endowments or trusts (e.g. “The Best Interest Scholarship”), etc.

- Don’t let society force you into spending on yourself. But if you derive joy from helping others, I’m sure there are philanthropic uses for your money while you live.

- If you have children, grandchildren, etc., remember Warren Buffett’s thoughts: leave them “enough money so that they would feel they could do anything, but not so much that they could do nothing.”

- And finally – run The McDonalds Test on your favorite things. Trust me.

One of the principle duties – albeit a “subjective” and hard-to-measure duty – of financial professionals is to imbue confidence in their clients to spend money! It’s called cashflow planning.

You should spend money. You should enjoy the fruit of your labors. Trust the math, trust the portfolio, and enjoy your life.

If you do that and still have lots of money left over, you need to determine – while you’re alive and mentally spry – what you want to do with it. Work with a CFP. Work with an estate attorney.

If you’re going to die with millions, make sure you’re putting them to good use.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!