After last week’s newsletter, reader-of-the-blog Nick wrote in:

Congrats on the new house! Would definitely be interested in seeing an interest rate thought process article. I feel like I lucked out when I did and if I had been a year later, I’d probably still be renting somewhere.

Nick

Here you go, Nick!

Interest Rates Up, Housing Prices…Up Too?

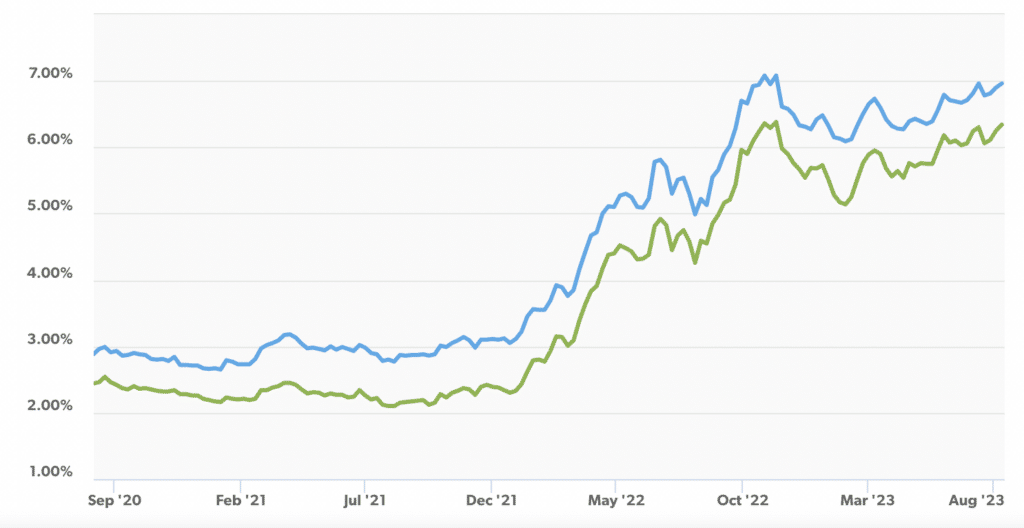

Over the past 18 months, mortgage rates have shot up from 2.25% and 3.00% (for 15- and 30-year mortgages, respectively) to 6.25% and 7.00%.

And while home prices have slightly decreased in recent months, the national average is still far higher than it was three years ago.

The upshot is a double-gut-punch to housing affordability. A $320,000 30-year mortgage at 3.00% costs $1349 per month. That same home would now require a $400,000 mortgage at 7.00%, costing $2661 per month. Literally twice as much!

So, why did my wife and I buy a new house with a 6.5% mortgage right now? Isn’t that, you know, a terrible personal finance move?

A House is a Home – Not an Investment

First, and most importantly: your house is a dwelling meant to meet your family’s needs; it’s not an investment!

A stock index fund is an investment. So is a Treasury bond. A home, however, is a lifestyle choice. Same as the clothes you wear or the car you buy. Sure, it’s a huge lifestyle choice, and the cost of a home cannot be understated. But it’s not an investment.

Don’t get me wrong. I would love for our home to appreciate in value. I plan on caring for it deeply because it’s a huge outlay of money. But that doesn’t make it an investment.

An investment returns cashflows to you, like a bond’s interest payments or a stock’s dividend payments. What cashflow does your primary home produce?

Let’s look at total cost. I’m talking mortgage interest, taxes, insurance, maintenance, everything. The real, inflation-adjusted return on residential real estate over the past 100 years is 0.5% per year! Yuck! Stocks are 6.9% per year and bonds are 2.3% per year.

A house feels more like a hard-to-upkeep asset. Not an investment.

So What Did I Think About Instead?

If a home isn’t an investment, then what did I think about for this buying decision? How did I accept a 6.5% interest rate when it was 3.0% just a few years ago.

- We loved the house. That’s first and foremost. It’s a terrific house and the former owners went many extra miles to take care of it and track their maintenance record over time. That’s huge! I felt confident I was buying a great house.

- Faced with the math in front of us (sale price, interest rate) there are two questions you could ask:

- Will this deal get better in the future?

- Is this deal affordable for us today?

- To me, the first question is irrelevant. This particular house won’t be available in the future (unless we’re oddly lucky). So instead, only the second question matters. If the answer is yes, then move ahead with the decision-making process.

- Life does not wait for interest rates. Kelly and I reached a point in life where we needed to graduate from the starter home. If I had a guarantee that rates would drop in 2024, we might have waited. But we don’t have that guarantee!!! And if they do drop, we can refinance the loan to our benefit.

- There are fewer buyers right now. The 6.5% rates have forced many buyers to search lower in the market, if not forcing them out of the market altogether. That sucks. But, selfishly, it worked in our favor.

- The crazy housing market also affected the sale of our old house. It more-than-doubled in value in just 5 years! That eases my pain as a buyer, for sure.

- Our salaries are growing. If we can afford the fixed mortgage payment today, I feel confident it’ll only get easier to afford in the future. That’s the benefit of fixed-payment loans!

Moving In…

Life doesn’t always wait for you, and you can’t always wait either.

Some investors started their 401(k) savings in the late 90s…then immediately got crushed by the Dot Com bubble and the Great Financial Crisis. Ouch. But looking back on it today, investing those initial dollars was still a smart move.

I think our housing purchase will work out much better than those investors’ poor timing, but the example is worth considering.

What if this house never appreciates one dollar, and we can never refinance?

Even in that bad scenario, we still have a home we can afford while hitting our other financial goals. The home meets my family’s needs. My 401(k) and Roth IRA are still well funded. I don’t need my home to be an investment, too.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

Interesting writeup, just curious if you and your wife calculated what the cost to rent a comparable place in your area was? Or were you dead set on owning (or maybe 531 exchanging)? I feel like it’s not a great investment decision to choose buying over renting (or even thinking about it) just because you can afford it…

Hey Mike – great question. yeah, I used a rent vs. buy calculator to help with the decision. There aren’t too many comparable 4+ BR homes for rent locally, but I catch your drift. At current prices in Rochester, and importantly for our projected timeline in this home, buying was the right decision.

In our case, 531 exchange is a non-factor because there were no taxable gains to worry about.

You’re right. The simple fact of “I can afford it” is not a prudent investing thought process. We had many more thoughts than that one alone haha. But again…**this is not an investment!** That’s my point 🙂