Imagine I made you this offer:

I want to sell you a piece of The Best Interest. It’s $100 per share.

I also guarantee it will be worth $110 tomorrow. Yes, an instant 10% profit in just one day. The guarantee is part of my magical powers. It’s my hypothetical, after all. It’s truly zero risk.

Hopefully we all agree my offer would instantly sell out. Every $100 share would sell because the idea of a risk-free, 1-day return of 10% is too good to pass up. As Warren Buffett would say, “I’m selling a dollar for 90 cents.”

That’s demand. As in “supply and demand.” The outrageous demand for $100 shares would catch my eye. Demand demands higher prices. Would people buy them for $101? Or more? The answer is: “Of course.”

So I’d raise the price to $101, then $102, etc. At each stop, the demand for guaranteed 1-day returns (9%, 8%, or even lower) would still be high. Rinse and repeat, the demand justifies higher and higher prices. But eventually, we’d hit an equilibrium where the size of the 1-day guaranteed return would be on par with other options in the investment universe. The demand would level off, as would the appropriate price.

For example, the overnight U.S. Treasury rate is 5.33% as of this writing (that’s an annualized rate), which equates to a 0.014% return per day. If my shares of The Best Interest are guaranteed to sell for $110 tomorrow AND the guarantee (a.k.a. the risk) is on par with that of U.S. Treasury notes, then we should discount my shares down 0.014% to about $109.98 today.

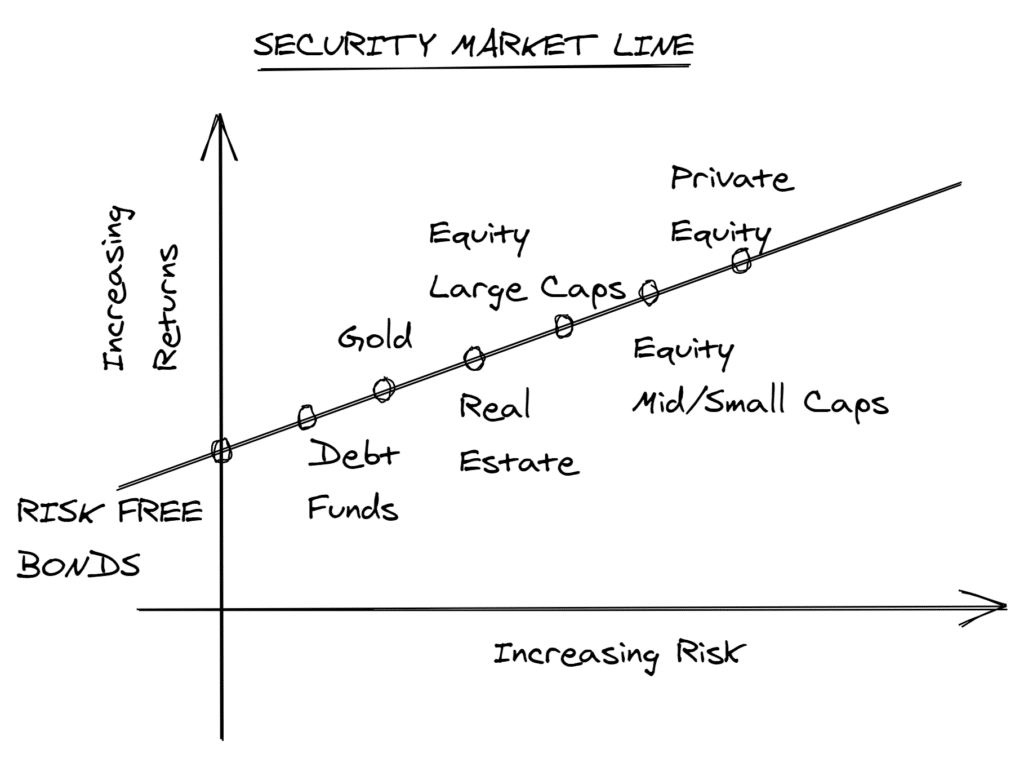

The more guaranteed an investment’s return, the closer that return will resemble the US Treasury’s risk-free rate. The less guaranteed a return, the more we, as investors, need to demand a larger reward.

That’s a fundamental tenet of investing. The logic works in reverse, too: the larger the reward we seek, the less guaranteed any return will be.

US Treasury notes are the baseline. The return is guaranteed over a short timeline, with the full faith and credit of the US government. It’s considered the closest thing to a guarantee in the investment universe. Therefore, US Treasury note returns are lower than any risk-bearing asset.

When we move up the risk spectrum to stocks, we expect a larger return. But must accept more volatility and the realistic probablitity that our investment will lose money, especially over short timelines.

If stocks were as guaranteed as bonds, stocks would have the same return as bonds. We don’t want that! We want more returns. The only way we’ll get there is by stomaching more risk. That’s the risk premium.

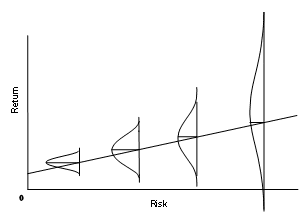

To visualize this idea, we need to overlay the following two graphs on top of one another. More risk equates to more expected return, but also to a significantly wider range of potential outcomes, including negative outcomes.

When novice investors say, “I want high returns, but only if it’s low risk,” they ask for the impossible.

If such an investment existed—just like my initial offering of shares of The Best Interest, a guaranteed 10% overnight—hungry investors would devour it. Their demand would spike the investment’s price. That higher price would squeeze away the expected return until the investment’s risk/reward profile reached equilibrium with the rest of the investable universe.

Anyone who, for example, guarantees the returns of stocks is fundamentally mistaken. This includes J.L. Collins 🙂

We can speak in probabilities and suggest that, over long timelines, stocks will probably have strong returns. But that’s not a guarantee. There’s risk involved. And that very risk is the only reason why stocks’ probable strong returns exist in the first place! Whoa! Circular!

Risk and reward. Demand and price. These ideas are intrinsically linked, and every intelligent investor needs to understand that.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!