The 2010s were not an anomalous time of stock market exuberance. In fact, they were normal. Decades like the 2010s will happen again.

I started working full-time in June 2012. The S&P 500 is up 141% before dividend reinvestment since then. I feel regret. I was saving a bit, but I didn’t focus on maximizing my opportunities until a few years later.

My simple financial goals weren’t in order. What did I miss?!

Just a normal decade. That’s all.

Do not predict, do not fear

Since the 2010s were good for investors (we’ll talk hard numbers below), and 2019 was very good (in the 87th percentile of 1-year S&P 500 returns), a lot of people are wondering, “When is this music going to stop?”

It only feels natural—what goes up must come down. But I encourage you to neither predict nor fear a coming recession. Timing the market is a loser’s game.

Buy-and-hold (through thick and thin) is a much easier and more reliable method. To quote financial planning author Frank Armstrong:

Buy and hold is a very dull strategy. It lacks pizzazz and doesn’t inspire much admiration at cocktail parties. It has only one little advantage: It works, very profitably and very consistently.

Sure, it’s more fun to think about selling at the perfect time. But it’s so much harder done than said. If anything, consider the bright side of a recession. For what appears to be no reason, stocks are now on sale for 30% less than than 6 months ago!

There are likely to be multiple bull (growing) and bear (receding) markets over the next couple decades. They’re inevitable. If you try to time them and fail, then you’ll be buying high, selling low, and missing opportunities for growth.

Instead, just go with the flow. Invest consistently and let the rising tide raise your ship.

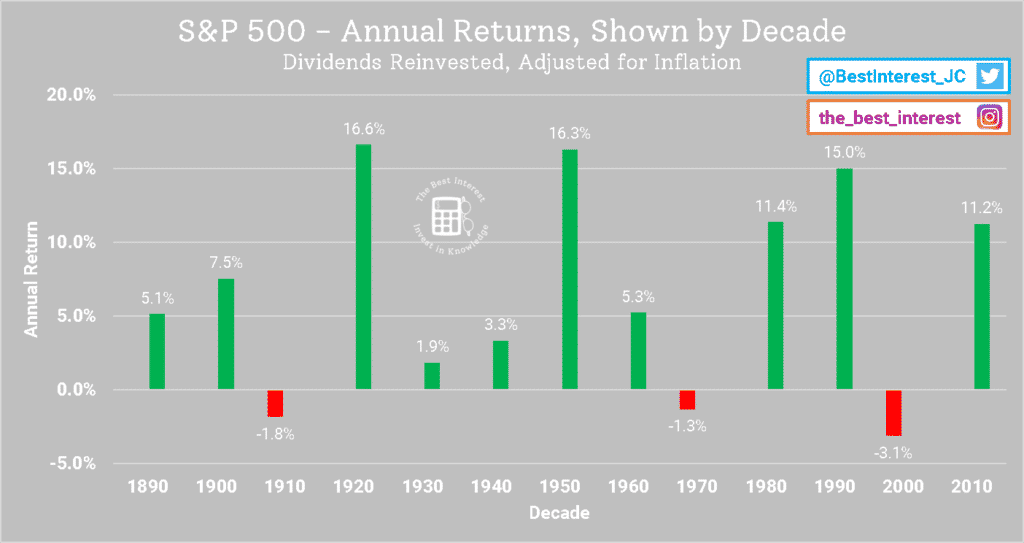

Comparing the 2010s to history

Below is a simple table showing the decade-by-decade growth in the S&P 500 since 1930. I’ve included data sets that show values with and without dividend reinvestment.

Note: all data was sourced from Robert Shiller. Thank you, Mr. Shiller, for posting this data publicly.

| Decade | S&P 500 change over decade | …including dividend reinvestment** and inflation |

| 2020s | …TBD | …TBD |

| 2010s | +187.5% | +190.3% |

| 2000s | (-22.1%) | (-27.2%) |

| 1990s | +320.2% | +304.8% |

| 1980s | +214.3% | +193.7% |

| 1970s | +19.4% | (-12.5%) |

| 1960s | +57.0% | +66.8% |

| 1950s | +249.9% | +352.9% |

| 1940s | +34.5% | +38.7% |

| 1930s | (-43.0%) | +20.3% |

**Note: dividends are a “share of the profit” that companies give their investors. Owning a stock means you literally own part of the company–and so you should get a portion of the profits. Many investors choose to reinvest their dividends by buying additional stock, rather than taking the dividend in cash. In the long run, reinvesting dividends makes a big difference, as it acts as a form of compounding growth.

What are some quick takeaways from this data?

- Out of nine decades, seven saw net growth…

- …while two saw shrinkage

- The 1970s (“Stagflation”) and 2000s (Dot Com bubble and the Great Recession of 2008)

- The 1930s had the Great Depression. But due to deflation and dividends, the real returns for the decade were actually positive

- There’s a 74% average decade-over-decade increase before dividends and inflation are considered

- That’s ~5.7% per year

- There’s a 87% average decade-over-decade increase after dividends and inflation are considered

- That’s ~6.4% per year

- The 2010s–while good–only come in 4th place out of 9 decades

Sure, the 2010s were good

There’s no denying that being invested during the 2010s was a good thing. A dollar invested in an S&P 500 index fund in January 2010 would be worth about three dollars today.

Before dividends and inflation, the year-over-year growth in the 2010s was 11.6%. After dividends were reinvested, that growth rate increases to 13.2%. As you might remember from these five simple personal finance charts, an 11.6% annual increase means you can double your money about every 6.5 years. A 13.2% increase doubles your money every 5.5 years. Over a 30-year career, that’d be great!

Unfortunately, it’s tough to maintain this kind of growth for an entire career. So, what could we expect instead?

As I mentioned above, the average annual return since 1930 has been 9.73% per year. While that’s not as good as the 2010s, it’s not too shabby!

So compared to the average, the 2010s were a good time to have your money in the market. Out of all 10-year periods in the history of the S&P 500 (not just cut-and-dry decades…I’m also including “random” 10-year periods, e.g. Apr. ’65 to Mar. ’75), the 2010s are in the 74th percentile in terms of growth.

That’s wonderful. But I don’t want you to think that you’ll never get this kind of opportunity again.

If we’re to learn anything from the past, it’s that the markets will continue to grow over the long-term. After all, 26% of all 10-year periods were better than the 2010s. It’s good math to assume the 2010s will happen again.

The market might ebb and flow in the short-term. A recession could hit today, tomorrow, or a year from now. But eventually, the markets will recover and ultimately grow.

Enjoying this article? Subscribe below to get new articles emailed straight to your inbox

Case Study: The 30-year old worker

In March 2020, I will hit the big 3-0. Yes, I’m frightened. No, I do not plan on entering a fugue state.

For the sake of this article, 30 gives us a nice round number to work with. While many of my FIRE-loving friends might be shooting for retirement by age 40, I’m going to look at something a bit further out in the future. Let’s say I want to work until 55, or for 25 more years.

What do all of the 25-year periods in the S&P 500 look like? How do they compare to the 10-year growth of the 2010s?

As wild as it might seem, about 12% of historical 25-year periods were better than the annual returns of the 2010s. That is, the 2010s will happen again and could last for 2.5 times as long! That’d be pretty nice.

In that kind of environment, the money I have invested today would increase by more than 2200% over those 25 years. And when you consider that I would continue adding more investment principal over those 25 years, it adds up very quickly. Maybe I could retire by 40…

But looking at an 88th percentile market is probably too optimistic for our retirement plan. A pragmatic bet is to look at the median–or 50th percentile–return, which comes out to 9.04% annually. In that kind of market, today’s investments would grow by 870% over 25 years. That’s still pretty good!

And if we want to cover all our bases, let’s be a bit pessimistic… what does the 10th percentile look like? 6.36% annual return over 25 years, or 467% growth.

While 4.7x growth seems paltry compared to the 2010s, it’s really not too bad. I’ll continue to store extra money away as I approach retirement. It’s 5x worse than the 88th percentile scenario, but I can still make a successful retirement plan around this pessimistic type of situation as long as I invest my money.

The future is a mystery

Neither I, nor you, nor the many experts on Wall Street can predict the future exactly.

I’m not sure when the 2010s will happen again, but I’m pretty confident about if they’ll happen again. While I’m sure the market will drop at some point, it’s hard to make money unless you can pinpoint both the time to sell and the time to buy back in. Do you feel lucky enough for that?

If not, simply realize that a wave is coming. There will be a crest, a trough, some splashes…and then more waves. Those future waves mean the 2010s will happen again. The low-risk, low-stress method is to neither predict its timing or its height. Just ride it out. It’s in your best interest.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

-Jesse Cramer

Pingback: Viral Stock Market Strategies - The Best Interest - Stay the course!