“You cannot beat the market!” …you hear this warning all the time. “The market” refers to the S&P 500 index, the Dow Jones index, a “total stock market” index fund, or something similar. In other words, these people say, “You cannot outperform a diversified pool of stocks.”

But as we peel back the onion on this guidance, we face two logical conundrums.

- First, there’s an averaging problem. The market’s return is an average of many stocks. You can’t have every individual stock losing to an average of those stocks. The logic doesn’t work.

- Second, if my stock-picking strategy loses to the market (as people might suggest), then my anti–strategy should beat the market. If one person is losing, just do the opposite of them. Voila. If I lose, you’ll win. Thus, at least one of us has “beaten the market.”

That was quick. It’s clearly not true to say “you can’t beat the market.” It’s an incomplete statement. It needs more details, more backup. And it leaves people misinformed. We’re going to fix that today.

Yes, you can beat the market.

But you need to understand how, when, and why. Answering such questions today will lead us to the following conclusion:

The question isn’t whether you can beat the market. You can. The question is “Why bother trying?”

Myth: “Nobody Can Beat the Market”

This myth is silly. Thousands of people beat the market every day, every month, every year. Some investors have beaten the market for decades.

Anyone who says, “Nobody can beat the market,” is misinformed.

But…

Truth #1: It’s hard…

Consistently beating the market is hard. We’ll cover that more below.

Consistently beating the market after fees is extra hard!

If fees aren’t involved, beating the market is possible. Not easy. Certainly not guaranteed. But possible.

But when someone else is managing your money for you, they’ll charge you a fee. That fee eats your profits. And since those profits have been eaten, beating the market becomes harder!

Golf gets harder if you begin your round with a few strokes already on your scorecard. It’s still possible to shoot under par. But harder.

The math of fees and investing and beating the market is that simple.

Truth #2: It’s Not 50/50…

You might think at this point:

“So without fees, 50% of stockpickers would beat the market and 50% lose to the market.”

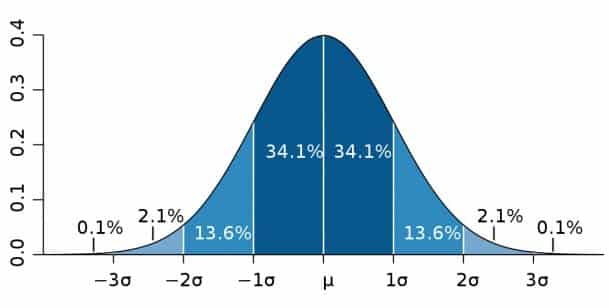

That’s a logical conclusion, assuming that stocks’ performances follow a normal distribution, a.k.a. a bell curve.

But stocks’ performances do not follow a normal distribution! This is an interesting and exciting fact.

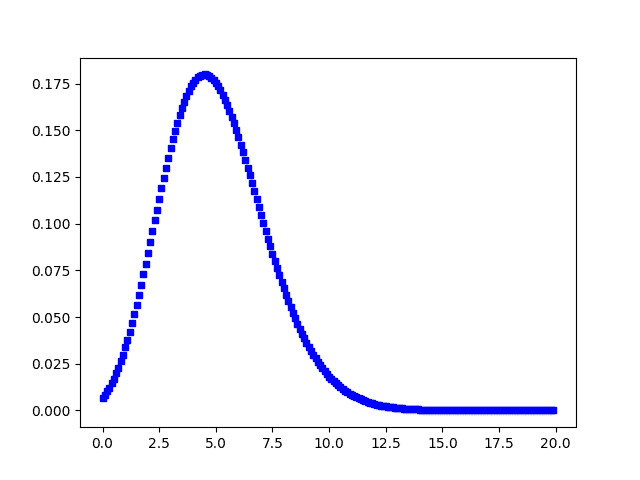

Instead, stocks’ performances more closely follow a “long tail” distribution.

Most individual stocks perform worse than average, but a small number of high-performers beat the average. As you can see in the image below, there’s a fat cluster of low results. There’s also a “long tail” of high results.

Let’s break down some stats. Huge shout-out to Meb Faber for his research findings.

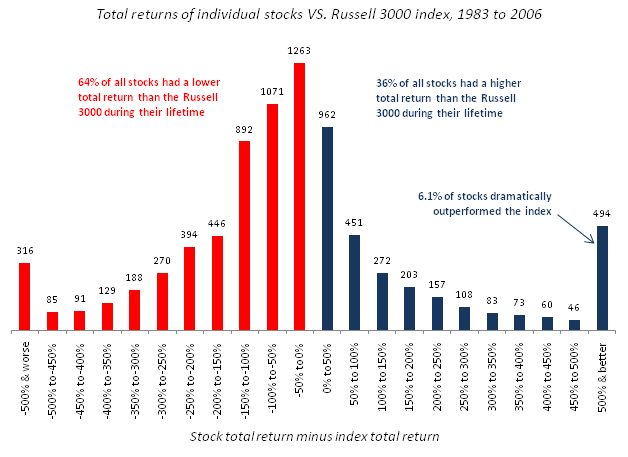

The following data covers the years 1983-2006, and was published in 2008. The research tracks 8,000 individual stocks over that time (all of which were at one point in the Russell 3000 index). A few intriguing findings:

- 39% of stocks lost money over that 24-year period. Yikes.

- 19% of stocks lost more than 75% of their value. Big yikes!

- 64% of stocks underperformed the index a.k.a. got beat by the market

- 36% of stocks outperformed the index a.k.a. they beat the market

- 18% of stocks outperformed the index by 100% or more

- 6% of stocks outperformed the index by 500% or more

Here’s a graphic visualization of that distribution (again, thanks Meb Faber):

A few other cool stats from the study:

- The mean average annual stock return over this period was -1.06% per year.

- The bottom 75% of stocks had a cumulative total return of 0%. The remaining best 25% of stocks accounted for all of the return in this period.

Ok – what’s this have to do with beating the market?

What Meb Faber’s Research Says About Beating the Market

This research tells us that “beating the market” is not a 50/50 proposition.

Over this researched time period, a single stock had only a 36% chance of beating the market.

There are many bad-to-mediocre stocks. There are few good-to-great stocks.

Go have fun with this Google Sheet. I created a fake market of 100 stocks to mimic Faber’s research. You can play around and build a “portfolio” to try to beat the market.

Pick a few stocks? You’re likely to miss out on the big winners and lose to the market.

Pick many stocks? You’ll simply mimic the average return, neither beating nor losing to the market. You’ve created your own index fund.

That is why it’s hard to beat the market.

The Luck vs. Skill Problem

The Google Sheet above is also instructive because your picks are pure luck.

You’re simply picking random numbers. Sometimes your numbers will cause you to win. Most of the time, you’ll lose. This is reminiscent of the “monkeys throwing darts” parables.

The real stock market, though, is a mixture of luck and skill. And it’s notoriously difficult to discern between the two.

Skill is repeatable. Luck is not.

If you invest with an active stock-picker you’ll face some scary questions…

- Have they recently beaten the market? If not, why would you invest with them?

- Assuming they have beaten the market, are they skilled? Or just lucky?

- Do you have the knowledge and skill to accurately assess Question 2?

The stock market is a notoriously efficient market. True, repeatable skill is hard to come by.

**Note: inefficient markets are different, and can more easily be beaten. Some money managers provide real, repeatable “alpha” for their investors by proving their skill in inefficient markets.

And any such skill is likely to be found in those who work the hardest.

In other words, the 80-hour weeks of a Wall Street pro are more skilled than the 20 minutes you spend watching my Uncle Jim Cramer.

Are you sure you want to play that game?

Wouldn’t an average return (e.g. from an index fund) be simpler, easier, and more guaranteed?

The Truth: Can You Beat the Market?

Saying “nobody can beat the market” is like saying “nobody is taller than average.” It’s dumb.

But you’ll notice that my tone has changed over this article.

Yes, you can beat the market. It’s a logical necessity. But it’s also complicated.

- It happens less than 50% of the time. That’s what Meb Faber’s individual stock results show us.

- It’s hard to repeat. Sometimes, it’s just luck. That’s what many active management studies have shown us.

- Your investing fees reduce your liklihood of beating the market. That’s basic math.

- Even when you do beat the market, was it skillful? Or just lucky?

- If you’re a DIY active investor, is your time commitment worthwhile?

- Are you smart enough (and unbiased enough) to answer these questions?

These complications all point in the same direction. Namely: why bother trying to beat the market?

It’s not that you can’t beat the market.

It’s just not worth trying.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

I wasn’t sure where you were going after reading the title. I was assuming references to Berkshire Hathaway stock or some venture capital…. Great explanation and I like the ending. Keeping it simple, low fee, making average returns with index investing has been working for me.

Thanks a lot, Tech! I’m glad you stuck with me until the end haha! 🙂

IMPOSSIBLE LONG TERM to beat the mkts

name a few who have done it over 40yrs

Thanks for the note. But if nobody beats the average, then there’s an issue with the statistics 🙂

”The market” doesn’t mean the average return of investors, it’s the average yield of SP500 ….

Hello, Anonymous. You’re right. I’m right, too. Because you and I are saying the same thing – nice! Happy reading!

If you’re good enough to beat the market over 40 years, then really you’ve probably made enough money to get out of the market well before 40 years is up and put your money somewhere safer.

So, either way you won’t find any who have stayed in that long.

Yeah, that’s a reasonable stance, Jeremy. Thanks for writing in!

You don’t always need to pick the best stocks though. A few really good ones over years of investing will be enough to bear the market.

That’s technically correct, Div Power. “Really good” stocks tend to be high enough performers that being overweight in them will have a significant positive effect on your total portfolio. The problem, alas, is identifying that small percentage of “really good” stocks.

Jesse

Well said. Beating the market can be done. However, it is a difficult task and unless you are willing to lose repeatedly, it is a pointless endeavor.

Cheers Olaf! Yep, I agree with you!

Trying to beat the market is not worth it if you restrict yourself to blind trial and error stock picking. But here are some other ideas that are more reliable:

https://earlyretirementnow.com/2020/12/09/how-to-beat-the-stock-market/

Thanks for sharing, ERN. Will read through your ideas tomorrow!