Bear markets make you question, “Should I wait for the bottom?”

In fact, reader Paulson recently wrote in to ask:

Jesse – I’m not tempted to sell anything in my 401k or Roth IRA. But I don’t know why I should continue buying at this point with the market doing what it’s doing. It’s not going up anytime soon. Can I contribute money to those accounts as cash and then wait to invest once the market hits its bottom?

It’s a great question. You can try, Paulson, but I don’t think you should.

Today’s article explains why timing the market:

- barely affects your future portfolio

- is really hard to execute, and

- makes your life demonstrably worse along the way.

The Story of Three Investors

We’re going to use three identical investors to tell this story: normal Nick, good-timing Gerry, and bad-timing Bill.

All three investors started their investing in 1985, when they were 22 years old. They’re now 59 and approaching retirement. Some other facts:

- All three use the S&P 500 for their stock investments

- All three invested $200/month in 1985 and have increased contributions by 5% per year until today. They now invest $1216/month.

- All three invest via dollar-cost averaging – they buy high, buy low, and buy in-between.

…except for one time.

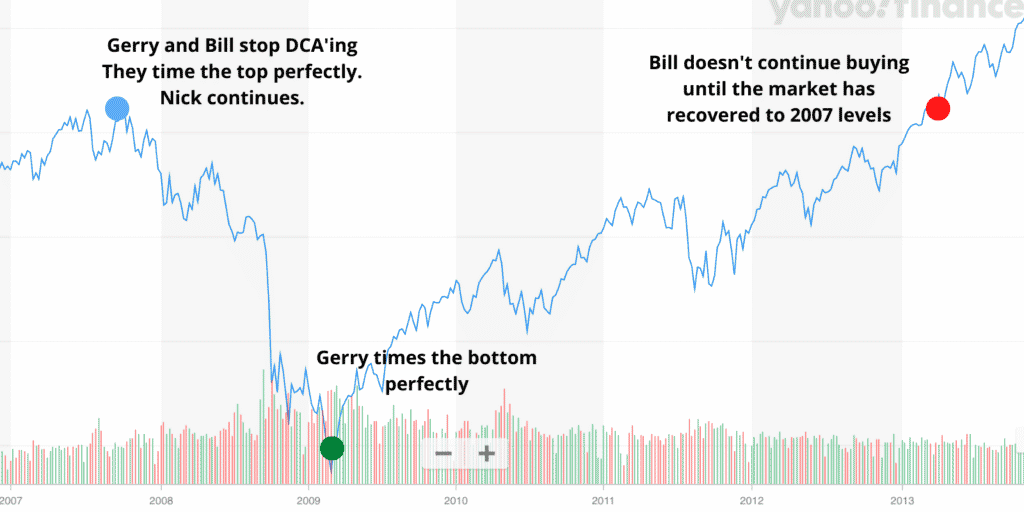

The Great Financial Crisis threw a small wrench into their plans. Nick stayed the course, but Bill and Gerry got greedy.

Good-timing Gerry managed to time the market perfectly. He stopped investing at the market top in 2007 and saved his cash. He then perfectly timed the market bottom in March 2009 and deployed his cash. He timed the market to perfection twice.

Bad-timing Bill also timed the market top with Gerry. But when the true bottom hit in March 2009, Bill was convinced there was more room to drop. As the market recovered, Bill waited. He thought a new bottom would eventually come. So he didn’t deploy his cash until 2013 when the market price had fully recovered to 2007 levels and his wise wife screamed at him to get back into the market.

Normal Nick plodded along the entire time, continuing his boring DCA buys as planned. Up, down, and in-between. Nick just keeps buying.

How Big a Difference Did Market Timing Make?

Now it’s 2022. How different are Nick’s, Gerry’s, and Bill’s portfolios?

Gerry’s is best. After all, he perfectly timed the market twice. He has $1.46 million.

Bill’s is worst, since he missed buying opportunities for ~5 years. He now has $1.38 million.

And Nick is right in the middle at $1.42 million.

The perfect market timing around 2008 got Gerry a 3% edge over normal Nick.

Bill messed up big time, yet Gerry only has a 6% edge over him.

Over the long run, Gerry’s perfect market timing isn’t that important.

Selling Out is a Bigger Deal Though…

Notably, Bill and Gerry did not sell their old investments. All they did was choose to no longer buy new investments.

If they had sold old investments and re-bought later, our conclusion would be much different.

Bill would have lost another ~20% of his total portfolio as of today (despite perfectly timing the initial market top!)

And Gerry’s portfolio would be ~50% higher (because he was perfect twice).

Perfect once, down 20%. Perfect twice, up 50%. Do you feel lucky?!

I like where normal Nick is at. He didn’t worry at all about timing the market. Zero skill, zero luck, zero stress. He just kept on buying. And he’s in a great place.

Not Worth the Squeeze

This is a scenario where the juice simply isn’t worth the squeeze.

The squeeze, again, is double perfection. You have to be right twice. If you manage to be right the first time (ceasing buys before the market bottom), you will likely be plagued by bad-timing Bill’s issue:

When the market is at peak pessimism, do you have the skill/knowledge/balls of steel to deploy your money?

Or are you a dumb market-timer like the rest of us?

And the juice? It’s a 3% boost on your final portfolio. Or maybe this time will be different. Maybe you’ll get a 4% or 5% or 6% boost.

While your money is out of the market, sitting on the sidelines, what will you be thinking? Are you going to be relaxed, with ice in your veins?

Or are you going to be a nervous wreck, worried about when to get back in the market?

Not only can this “squeeze” cost you money, but its psychological cost is unavoidable.

A MagnifyMoney poll (take it with a grain of salt) showed that:

- 10% of investors cry from the regret of selling their investments too early

- 66% regret making portfolio choices based on emotion – like the pessimism we’re surrounded by right now

Gerry gained 3%, sure, but he also gained some white hair. He was out of the market for 18 months. We’re only 6 months off all-time highs right now.

Are you willing to wait for another 6, 12, 18, 24 months? Or more?

Here’s more info on the basic timing of bear markets

I’m not. Who knows how long it’ll take us to return to all-time highs.

I don’t want to test my skill with timing the market. I don’t want to test my blood pressure by staying out of the market.

I’d rather go for a run and play with my dogs.

Wouldn’t you?

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!