Nobel Prize-winning economist Paul Samuelson famously quipped,

“When the facts change, I change my mind. What do you do, sir?”

Paul Samuelson

My thoughts on investing have shifted over the years. New ideas consistently challenge me and force me to question my assumptions. That’s good, right?!

Perhaps my biggest shift, especially over the ~3-year arc of writing this blog, involves my understanding of skill in investing.

My first investing books were The Bogleheads Guide to Investing and A Random Walk Down Wall Street. Both books are phenomenal. Both made a lasting impact. But as I’ve recently realized, both have limitations.

The underlying premise of both books is that skill in investing is a myth. True skill would be repeatable and replicable. Instead, these books argue that any “skill” in investing is usually random and always fleeting.

It’s just like the “skill” of flipping a coin. In a room of 1000 coin-flippers, someone is going to win 10 times in a row. Are they skilled? Of course not. It’s just the law of large numbers at work. Even after 10 consecutive winning coin flips, the 11th will still be a 50/50 chance. There’s no skill in the streak.

These books argue that the stock market is similar. It moves in random, unpredictable ways. Successfully picking stocks, therefore, is impossible to repeat over time.

The books conclude that the only logical way to invest is via passive index funds that diversify across the entire market.

I adopted this premise hook, line, and sinker. You can’t beat the market. Period. #TeamIndexFund

(For what it’s worth, a significant portion of my net worth remains in those low-cost, passive index funds).

Enter Uncle Warren

But then I started listening to Warren Buffett—considered by most to be the most successful investor of all time.

Buffett didn’t make his fortune via index funds. He picked individual stocks and bought individual businesses. Stocks, after all, are nothing more than shares of a business. And some businesses, according to Buffett, are better run, make better products, have wider “moats” protecting them from their competition, have stronger brands, etc.

And those businesses make better investments.

Hmm. That makes a lot of sense. And it’s not random.

Similarly, Buffett (and his business partner, Charlie Munger) dislike diversification in their portfolio. Just listen to them here!

And while the daily swings of the stock market might be too random to predict, the long-term trends of Buffett’s stock picks are, according to him, very logical. When you zoom out over long enough timespans, it’s anything but random.

In the short run, the market is a voting machine but in the long run it is a weighing machine.

– Ben Graham

In other words, Warren Buffett’s methodology is the complete opposite of what I believed. And his long-term results have trounced the market average.

After hundreds of hours (literally) of listening to Buffett’s shareholder meetings, his logic sank in. My mind accepted a new set of facts and my opinions slowly shifted.

Streaks and Skills

Let me briefly change subjects: let’s talk baseball. If skill is measurable in any arena, surely it’s measurable on the baseball diamond.

Baseball is a zero-sum game (pitchers and hitters have opposite incentives) where outcomes are easy to observe (hits, runs, strikes, balls, errors, etc). Skill, therefore, can be accurately measured through statistics.

Hitting skill is measured as a ratio of hits per at-bat (“batting average”). And baseball fans also measure “hitting streaks,” or consecutive games in which a player has at least one hit.

In a true game of skill, the longest hitting streaks should belong to the most skilled hitters. But does that bear out for baseball?

There have been 56 individual hitting streaks of 30+ games in Major League Baseball (MLB) history. Coincidentally, the longest of those streaks is 56 games (Joe Dimaggio in 1941).

Looking at those 56 streaks, the streakers’ career batting average is 0.304 (304 hits per 1000 at-bats). In contrast, the average batting average in all MLB history is only 0.262.

Only one of the 56 streakers had a career batting average worse than 0.262. The other 55 were above-average hitters.

Did all great hitters have lengthy hitting streaks? No.

Did all the long streakers have great career averages? Most, but not all.

But in general, the streakers had significantly better batting averages than the average MLB player. Their short-term success (a single streak) is positively correlated to their long-term success (their career batting average).

Not only is skill easily measured in baseball, but short-term streaks have a positive correlation to skill.

Is This An Investing Analogy?!

It’s dangerous to use batting averages and hitting streaks as an analogy for investing success.

Baseball data is:

- Readily available

- Easier to measure and agree upon

- Extremely discrete (individual pitches, at-bats, innings, games, etc.)

Data from investing is chaotic. Fund managers come and go. Not all “measuring sticks” are equivalent. The real world is anything but discrete. The list goes on.

Perhaps most importantly, we know that investing markets exhibit a reversion to the mean. Put another way: it’s easy to have a hot investing streak in a bull market. It’s easier yet to fool yourself into thinking it’s skill.

The bubble of baseball is not an ideal metaphor for the real world.

Nevertheless, we can ask this important question:

If investing skill is non-existent—and success, therefore, is random—just how “lucky” have the top investors been? Without skill, Warren Buffett must be the luckiest guy on Earth. Just how improbable has his lifelong luck been?

Let the Probabilities Speak

Some of you are cursing me right now. How dare Jesse challenge the Shrine of Index Funds?! BLASPHEMER! I hear you. But let me drop some math on you, and you be the judge.

Warren Buffett’s Berkshire Hathaway has outperformed the S&P 500 in 38 of the past 57 years—exactly two-thirds of the time.

Let’s assume the ultimate pro-indexing stance: Buffett’s success was all luck. Stock picking is a random enterprise, like a coin-flip. And sometimes you’ll get 38 heads out of 57 flips.

But we know that picking stocks isn’t actually 50/50. We’ve discussed on The Best Interest that only ~36% of stocks beat the index over time. We can round up to 40% to make the math easier. Stock-picking is a 40/60 flip.

If that’s the case, then Buffett’s performance over the past 57 years had a 1 in 24,000 chance of occurring.

Not impossible. But highly improbable.

Is this proof-positive for my argument? Is there skill in investing?

I can’t say for sure.

The problem with probabilities is that it’s hard (if not impossible) to know anything for certain. We can only measure confidence levels. And I’m 99.9% confident that Buffett’s career cannot be explained by luck.

An exciting question, then, is to ask: how much skill would be needed to make Buffett’s results more realistic?

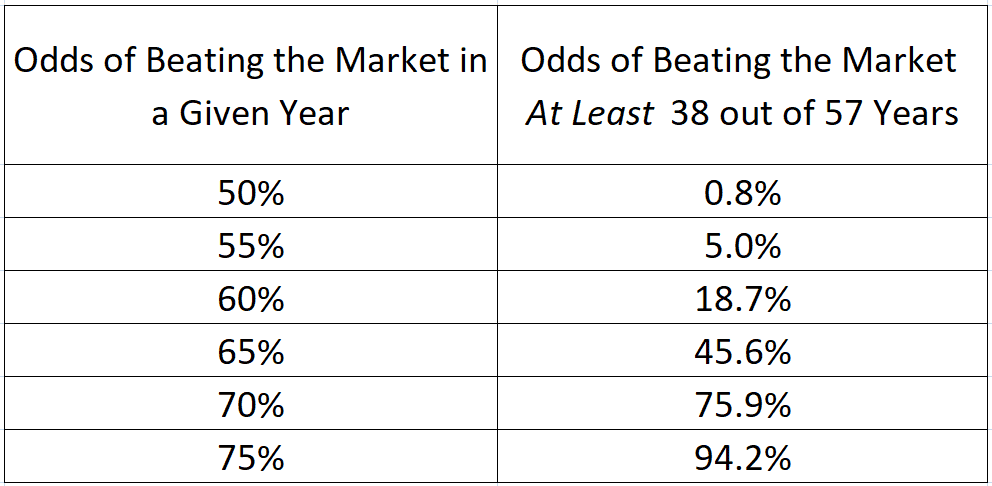

Whereas the zero-skill investor beats the market 40% of the time, what if a “skilled” investor could beat the market 50% of the time? In that case, Buffett’s career performance had a 1-in-122 chance of occurring.

We can do the same math—which pairs combinatorics and probability—for a few different stock-picking probabilities.

We can’t guarantee Buffett’s skill. But his results are most confidently explained by a 65% rate of beating the market. That’s a serious advantage over the 40% average.

A smart investor would bet that yes, there is skill in stock-market investing.

Again, this is all probability, statistics, and confidence levels. Nothing is guaranteed. There are no 0% or 100% scenarios here.

But there are reasonable outcomes. And there are long-shots.

The absence of skill in Warren Buffett’s career is a long shot.

What To Make of This?

Is it time to sell your index funds and start picking stocks?

No!

Major League Baseball is an ironically good metaphor here. You shouldn’t abandon your office career to play pro baseball. Similarly, you shouldn’t abandon a passive indexing strategy to pick stocks.

Stock market skill is hard to attain and maintain, challenging to recognize, and psychologically painful to execute. Most “stock pickers” I’ve interacted with don’t even know how to read a stock chart. They are truly out of their depth.

But for a small minority, true investing skill does exist. It’s far from impossible. Today’s simple thought experiments bear that out.

And since investing skill is real, it means there are real lessons to be learned from skilled practitioners.

Now that I’ve convinced you investing skill is real, I suggest you read this.

The question isn’t whether someone can beat the market. They can. The question is if it’s worth trying!

I have learned from the following investors, and encourage you to do the same:

- Warren Buffett

- Charlie Munger

- Howard Marks

- Jack Bogle

- Ray Dalio

- Bill Ackman

- Peter Lynch

- Seth Klarman

- Mohnish Pabrai

- Ed Thorp

- Michael Mauboussin

You’ll notice, as I have, similar through-lines between the way each thinks. There are patterns in their success. It’s not random. It’s organized. They all use similar decision-making frameworks. These frameworks are effective in investing and in all of life!

These investors have helped me grow, write, and see the world through a clearer lens.

Also—I wrote this article because I think it’s the truth. I’ve grown frustrated at the indexing zealots who openly admit, “Sure, skill might exist in investing, but admitting so publically might hurt individual investors.”

Just tell the truth. Tell it openly and clearly and to the best of your ability. Trust in others’ intelligence.

When the facts changed, I changed my mind.

What do you do?

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

Another great post.

Is there a reason Jack Bogle’s name was missing in your list?

Thanks a bunch, Tech!

Yes, there was a reason.

Author error! 🙂 it’s been amended. I’m a big Bogle fan!