As the 2010s closed, many young and new investors were in for a shock. Even cautious and conservative investors – e.g. those diversifying, utilizing index funds, not chasing the hot stock, etc. – had seen 15%+ annualized returns from their stock portfolios toward the end of the decade.

Investing is easy!

Pile away some money, compound at 20% for a few years, then head to the beach. Mojito, please!

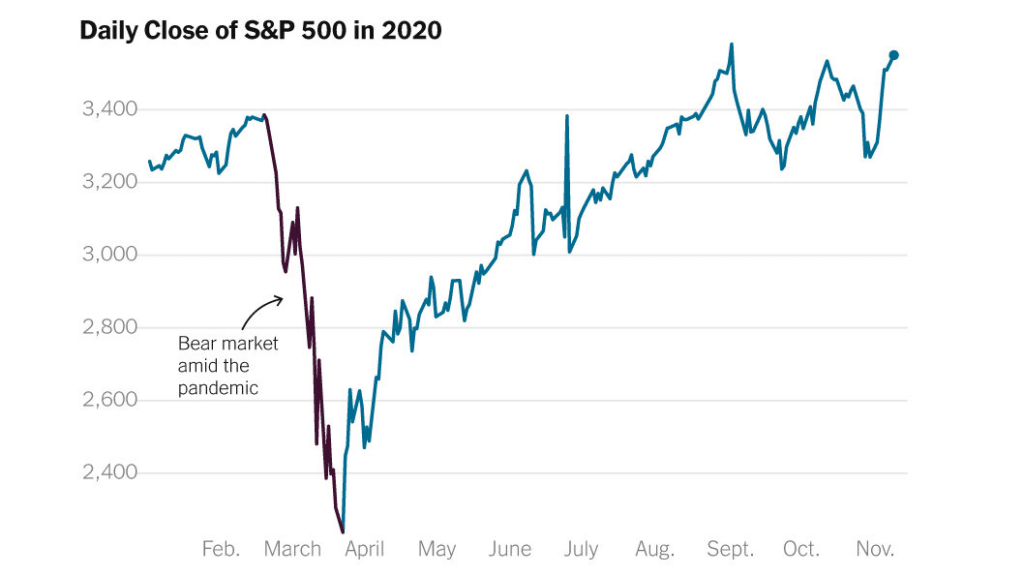

Then 2020 brought a shock…but only for a few months. In fact, 2020 probably taught more of the wrong lesson. Sure, pandemics hurt…but just wait for the historic and massive recovery!

2022 taught the real lesson. Investing – especially stock investing – has perils, too.

Still, the good outweighs the bad. The up years outweigh the down years, and stock market investing has, historically, been a net positive…if you wait long enough.

But how long do you have to wait? Let’s look at a “normal” investor who does the following:

- They invest the same amount every month, like you might in 401(k) or to your IRA. They dollar-cost average.

- They invest in a broad-based, low-cost index fund. I’ll be using the S&P 500 historical data (from Robert Shiller**) as a proxy for a U.S. stock market index fund.

- They don’t sell. They just keep buying, through thick and thin.

**All data is this article assumes dividends are reinvested, and shows real, or inflation-adjusted, returns

Is 3 years long enough to ensure positive returns? Not even close. A quarter of the time, you lose money over 3 years. In fact, you have a 1-in-10 chance of losing 20% or more. That’s far from a good outcome.

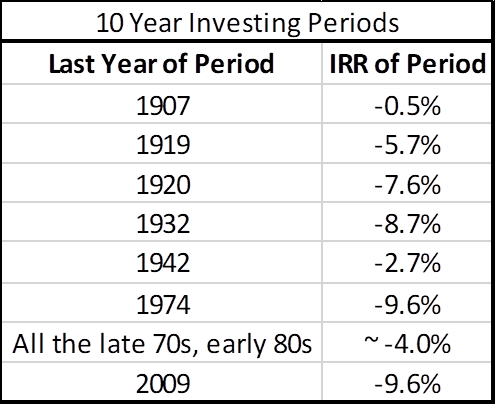

What about 10 years? About 88% of the time, yes…but not 100% of the time. There have been distinct periods in stock market history were 10 years of consistent dollar-cost averaging lost you money.

Below is a table showing the last year of such periods, along with the annual internal rate of return (IRR) of those periods. IRR is the proper way to account for the various investing periods that dollar-cost averaging creates (120 months, 119 months, etc). You shouldn’t just look at beginning and ending. You need to account for everything in between.

You could have invested every month from March 1999 to March 2009, and the final result is as if every one of your dollars suffered a 9.6% annual loss from the moment you invested it.

Ewwwww! Compare that filth against the magic of the 2010s. It’s a completely different story! Someone who invested the same way from November 2011 to November 2021 would have a +13.8% annual IRR.

(-9.6%) and +13.8% annual returns are both within reason for 10-year stock market investing timelines. But the two investors who suffer these opposite fates would feel as if they’ve lived different lives. I want you to be aware of both possibilities.

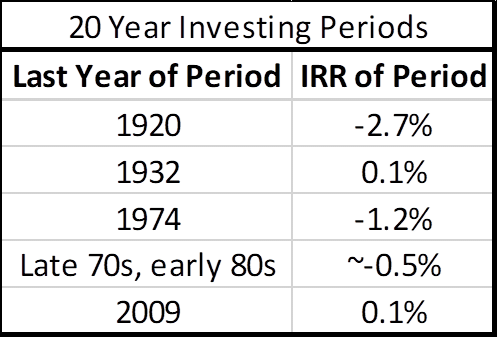

If we zoom out to 20 year timelines, the results change. Negative periods are still possible, but far more unlikely. Only 5% of 20 year periods had negative IRRs, all concentrated around the end dates in the table below.

Yes – someone could have invested diligently from March 1989 to March 2009, and their real annualized return was just 0.1% per year. That’s not a fun outcome. But it is an unlikely one.

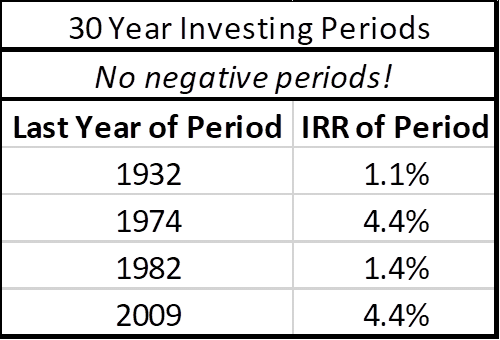

If we zoom out further to 30 year periods, there are no periods of negative IRR.

There are still bad periods, no doubt. But at least we’re seeing real, positive annualized returns. We’re getting some reward for taking these risks.

Let’s pause the bad news. Because the median of these 30-year returns is 6.6% annually. That’s amazing. That’s the reason we invest in the first place. We are making a bet that the median will apply to us, and we’ll see 6.6% annual real returns in our own portfolios.

But only if we wait long enough.

The upshot from this data is that stock investing is not a short-term exercise. There are far too many bad outcomes occurring over 3-, 5-, and even 10-year periods. Short-term money should not be invested in stocks. Something like U.S treasury bonds or money markets makes far more sense.

But if you have the time, patience, and stomach, then long-term stock investing is great place to be.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

If you dollar cost averaged from around the first 10 year period you listed (1.99) through the end of the last period (12.21) I think you did very well. You were buying low for 10 years and then watched your balance shoot up over that second 10 year period, unless I’m missing something.

You’re certainly right Jeff.

Most 22-year periods are positive. Less than 3% have negative IRRs.

That particular 22-year period saw a terrific 9.13% annual IRR – putting it in the 79th percentile of all 22-year periods.

Goes to show that 10-year periods aren’t long enough for our purposes 🙂