Room for error is one of my favorite problem-solving frameworks. To describe what I mean, Morgan Housel recently wrote:

Room for error is underappreciated and misunderstood. It’s usually viewed as a conservative hedge, used by those who don’t want to take much risk. But when used appropriately it’s the opposite. Room for error lets you stick around long enough to let the odds of benefiting from a low-probability outcome fall in your favor.

Morgan Housel

I don’t know what the future holds. Neither do you. But leaving room for error ensures I can roll with the punches. I don’t know all the answers right now (…do you?). But room for error means I’ll be ok.

From an investing point of view, I’ve created the following framework:

- I don’t need my annual returns to beat 80% of investors. I don’t need to be remarkable.

- But I refuse to be beaten by 80% of investors. I cannot be terrible.

- As long as I’m around average – consistently – my long-term prospects look good.

Of those three bullets, the middle is the most important. In investing and in life, prioritize avoidance of terrible situations.

An oft-cited example of this is told by Charlie Munger from his days as a U.S. Army Air Corps meteorologist. He created weather reports for airmen and pilots in World War II.

Munger was unsure how best to approach his job, so he applied a math technique from his university education. In complex math, inversion can be used to, in essence, turn a math problem inside out**. The solution to the inside-out problem can then be “reverted” to find the solution to the original problem.

**Some problems, in turns out, are way easier to solve inside-out than normally.

Rather than ask, “how can I be a great meteorologist?,” Munger inverted the question: “How can I be a terrible meteorologist?”

The answer: create life-threatening scenarios for the pilots. Specifically, the two most common weather-related life-threatening risks were:

- Cold weather forms ice on the planes’ wings, disrupting aerodynamics and adding unwanted weight.

- Wind pushes planes so far from their home base they’d run out of fuel before returning.

Munger then inverted the answer. Avoid those life-threatening risks at all costs. And to do so, Munger needed room for error against those risks at all times. Sure, there were always military benefits to these flights and missions. But Munger’s duty was to always include room for error against the two biggest life-threatening risks.

Applying this idea back to investing, Howard Marks writes:

I feel strongly that attempting to achieve a superior long term record by stringing together a run of top-decile years is unlikely to succeed. Rather, striving to do a little better than average every year — and through discipline to have highly superior relative results in bad times — is:

– less likely to produce extreme volatility,

– less likely to produce huge losses which can’t be

recouped and, most importantly,– more likely to work (given the fact that all of us are

Howard Marks

only human).

When the market is up 30%, Marks feels fine being up only 15%. But when the market is down 30%, Marks wants to only be down 5%. These “highly superior relative results in bad times” have separated Marks from other investors. Why?

- Catastrophic returns lead to getting fired. Marks’ clients don’t fire him because he avoids those catastrophes.

- The simple math of loss and returns. A 10% loss requires a subsequent 11% gain to return to even. But a 70% loss requires a 233% gain to get back to even. Marks avoids situations where his only hope is a miracle.

Marks isn’t alone in this approach. Many professional money managers – whose mission should be ensuring great long-term outcomes for their clients – focus on risk mitigation. But this risk aversion is commonly criticized on a mathematical basis. The criticism usually sounds something like:

Since stocks historically return 10% per year and bonds historically return 5% per year, why should anyone ever own bonds? How can you ignore this obvious math?!

Let’s invert the scenario. How do I ensure a terrible long-term outcome for an investing client?

- Avoid investing their money at all.

- Invest their money in such low-risk assets that they barely receive a return on investment.

- Expose them to terrible, painful outcomes. Invest their money in such high-risk assets that their brain short circuits when an inevitable 50%+ crash occurs, and they swear off investing forever***.

Now let’s invert that answer back to what we need. To ensure great long-term outcomes for clients, I need to:

- Invest! Harness the power of humanity’s economic engine and compound returns.

- Take enough risk to merit long-term reward.

- Avoid over-exposure to “pain.” We each have different pain thresholds. But make no mistake: painful investing outcomes (even if short-term) can completely derail a decades-long financial plan***

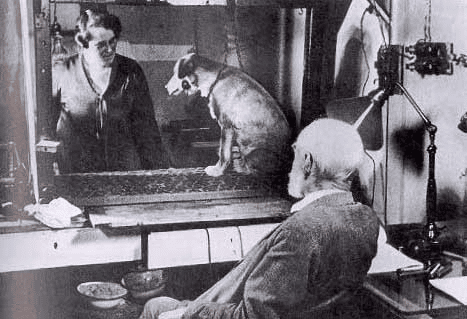

***There’s a little-known epilogue to the famous story of Pavlov’s dogs. Warning – it’s pretty sad. It’s also eye-opening.

In 1924, St. Petersburg flooded. Many of Pavlov’s dogs were trapped in their kennels as the water rose around them. Needless to say, it was extremely stressful for them. And this stress broke their conditioning. They forgot their training, forgot their bonds with humans and other dogs, and forgot that bell-ringing meant “meal time.” They suffered doggie PTSD! And their reactions – extreme anxiety, withdrawing, refusing to eat – were self-harmful.

Humans share this brain-wiring. Severe stress re-wires our brains. For some people, large losses of capital (even if only for a short period of time!) can be extremely stressful. And the subsequent reactions – “I’m never investing again!” – are often self-harmful.

Room for error helps us avoid these situations.

Going back to the criticism – why should anyone ever own bonds? Put another way, why would anyone ever ignore the mathematically-optimized quest for the greatest total returns?

Because somewhere on that journey to maximized returns, you might end up as a dog in a kennel with floodwaters rising around you. Or as a pilot too far from home with ice built up on your wings.

Those scenarios can break you. Avoid them at all costs. Using room for error is in your best interest.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

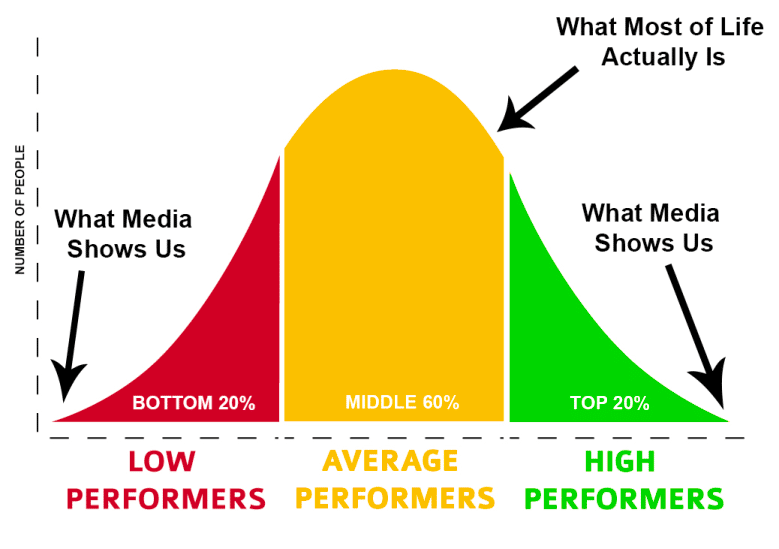

While many people do make bad decisions under stress, mature and stoic individuals do not. It is very possible to train your mind to not react unfavorably to negative stimuli. Just as there are people on the bad end of the bell curve when it comes to sound decision making there are people on the extreme good side of the curve. That includes people like Munger, and I’d say from the excellent advice you give, people like you, Jesse. And hopefully me too. I haven’t enjoyed my pretty significant bond exposure this year, but also I have not even thought about changing my investment plan.

Well said, Steve. As with all bell curves, the outliers are limited in number. And if I had to guess, I think the “wide middle” of the curve does not possess the strong stoic mindset that you refer to. At least, it feels that way from my anecdotal life sample.

I think Munger and Buffett have had such outsized success because they are statistical stoic outliers.

The FIRE movement certainly espouses being a stoic outlier. And I think many FIRE aspirants have drunk that beneficial Kool-Aid. But reciting stoic philosophy is different than enacting the philosophy. I hope we’re all able to continue staying the course, even throughout the most challenging times in our future.