Don’t miss an episode of our podcast, Personal Finance for Long-Term Investors. Available on all podcast players.

Here’s the latest episode:

Brenda Aubin-Vega is a 20-year-old woman from Montreal who recently hit the top prize on a lottery ticket. Winner winner, poulet dinner.

But her choice – to collect $1000 per week for life, instead of collecting a $1 million lump sum – has created some controversy. Did she make a poor financial move? I’ve looked at the numbers and…I think it’s a gray area.

A few of you have asked me for my financial two cents. There are incredible retirement lessons here. Let’s dive in.

The Numbers

Instead of taking a one-time $1 million payout, Brenda opted to receive $1,000 every week for life.

In most lottery scenarios, we need to consider taxes. It’s not about what you win. It’s about what you keep.

The United States does impose taxes on lottery winnings, but Canada does not. Roughly speaking, my amateur research shows a pretty even split around the world – some countries tax lotteries, others don’t.

For Brenda, though, there’s no tax on her lottery winnings. As we’ll get into later, though, she will/would have paid tax on her investment growth if she used her winnings to invest.

The numbers, therefore, are easy to understand: $1M in hand today vs. $1000 a week for life.

The Soft Side

We could make subjective, psychological, behavioral, “soft side of money” arguments in either direction here. We all know, I hope, that life isn’t lived in a spreadsheet.

I’m not saying those arguments aren’t valid. But I am saying that we could use that subjectivity to argue anything, to put our finger on either side of the scale.

For that reason, I’m just sticking to the numbers today.

“…For Life” – But What If She Dies Early?

What happens if a lotto winner dies young? Does their $1000 for Week for Life simply…stop?

Let’s go to the source. Here it is from the Loto Quebec website:

In the event the winner dies within the first 20 years after the prize claim date, the annuity is transferable to the winner’s legal heirs, who will receive the same annuity, paid at the same frequency for the balance of the 20 years that have not elapsed.

In other words, Brenda and her estate are guaranteed at least 20 years of payments. That’s her worst-case financial baseline.

Editor’s Note – We all hope Brenda lives a long, fruitful life. C’est la vie, I think?

The Base Case – Cash vs. Annuity

Let’s start our analysis today with an easy idea.

On one side, we have the $1000/week that Brenda chose. It’s an annuity that pays her 5.2% per year.

The annuity’s guarantee is essential here. It’s risk-free. If we’re going to make an apples-to-apples comparison against the lump sum side, it also needs to be risk-free.

So let’s examine a lump-sum invested in a simple, safe fixed-income asset; something like a high-yield bank account or, more reasonably, a long-dated government bond. A 30-Year US Treasury is yielding 4.83% as I write this. Note – Canadian long-term bonds are yielding 3.83%.

But, we need a little nuance.

Brenda’s $52,000 per year is tax-free. It’s a lottery winnings. Per Canadian tax law, she nets 100% of the gross.

But if we chose the lump-sum option and bought a 4.83% Treasury bond, that bond income would be taxed. While Canadian federal tax rates are generally on par with US federal rates, Canada’s provincial tax rates (e.g., Quebec taxes) are much higher than US state taxes. It’s reasonable to assume a 30% total tax on the lump-sum bond income.

We can now compare these options over 20, 30, 40+ years.

At the end of the period, no matter the length, there’s no remainder from her annuity. The only benefit to Brenda is the cash flow itself. But the lump-sum option, invested in risk-free assets, will still have $1M left over. That is a significant difference between the two choices.

Let’s crank the spreadsheet.

The lump sum is easy to analyze:

- On Day 1, Brenda commits $1M to the long-term Treasury bond

- Every year, it yields $48,300 gross, or $33,810 net of taxes.

- Then, at the end of the period, we can say the bond “matures,” and she gets her $1M back.

This is a simple, easy 3.381% internal rate of return, no matter the time period.

The annuity rate of return changes over time, though. The longer the annuity, the closer the return approaches its upper limit of 5.2%. Hopefully, this chart below makes sense to you…but in case it doesn’t, read on:

- At age 40, Brenda has collected $1.04M of weekly distributions. We can (and should) consider her “initial investment” to be the $1.00M she forgoed on Day 1. Therefore, she has earned $40,000 over 20 years on her $1M investment, which leads us to an IRR of 0.38%

- But by age 52 (or 32 years of collecting $52,000 per year), Brenda’s IRR is now 3.44%. That’s better than the lump sum option. It’s purely coincidental that 52 is Brenda’s age tipping point and she’s collecting $52,000 per year. That, or the aliens are tweaking the simulation again.

- And as Brenda lives longer and longer, her IRR approaches the upper limit of 5.2%, or $52,000 / $1M. Bonus point if you remember our calculus vocab from November – this is another asymptote.

In other words, if Brenda lives to be older than 52, then her choice was correct through the lens of making the better risk-free investment. I feel good about a 20-year-old living until at least age 52. Don’t you?

With this set of assumptions, Brenda’s choice makes sense.

Case #2 – Adding Some Risk

I hope you’re asking yourself,

“But would Brenda (or would I) invest all of my lump sum in long-duration bonds?”

We must start there. And we did.

But the Canadian government didn’t offer Brenda any “higher risk” avenues. We, though, might choose a different investing strategy if we could. We might introduce riskier long-term assets (e.g. stocks) into our lump sum portfolio mix.

What if Brenda invested in a 60/40 asset mix forever? Surely, over time, she’d outperform the simple long-duration bond…right?

But in the 60/40 example, what question do we ask of Brenda’s portfolio? Which historical periods do we use?

Do we require that her portfolio generate at least $52,000 in net income and never run out?

Do we measure her portfolio’s returns over time (or across different historical backtests) and compare those returns to the IRR of her annuity? That’s another good option.

All good questions. Let’s dive in.

Case 2A – Creating $52,000 Per Year

In this first scenario, I’m going to ask Brenda’s hypothetical 60/40 portfolio to generate at least $52,000 per year and never run out.

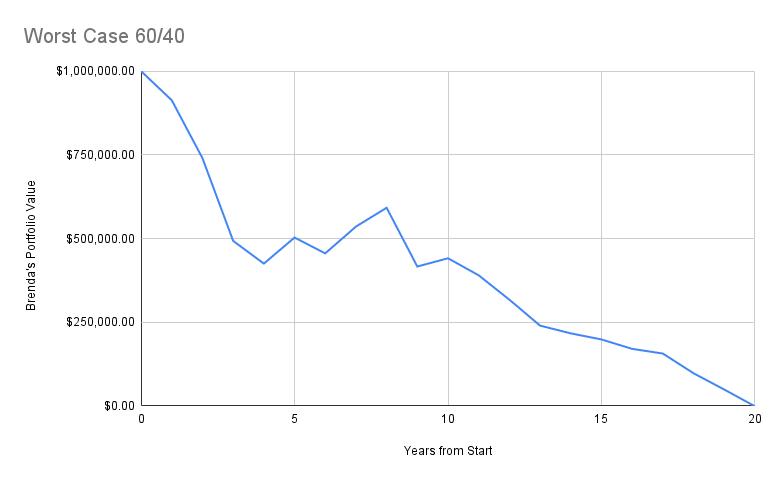

The only good way I know to do this involves historical backtests. And, because we’re trying to stress-test these scenarios, it makes sense to start with the worst-case scenario.

Using Aswath Damodaran’s data, the worst 60/40 period in history started in 1929. It’s the Great Depression. Not surprisingly, the Great Depression would have created a terrible sequence-of-returns risk for Brenda. Her portfolio would totally expire at exactly Year 20.

The chart below includes both market returns and her annual $52,000 withdrawals.

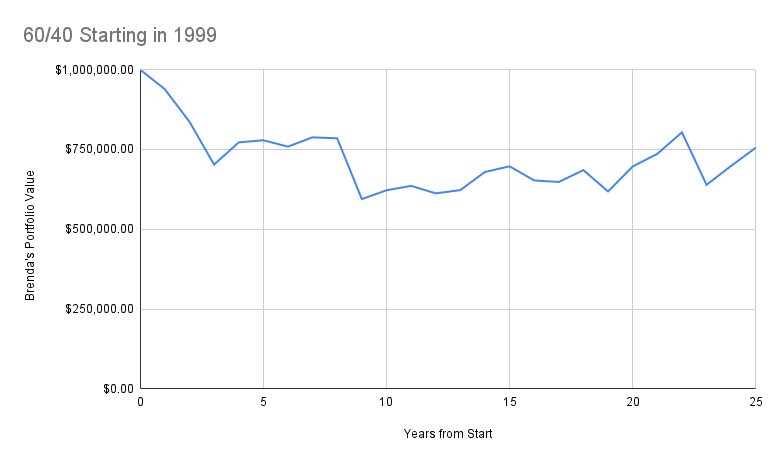

Let’s dial up the optimism, at least a little bit. Let’s start Brenda’s 60/40 journey in 1999 – the second-worst time she could have chosen.

Despite the terrible 2000s decade, we see that Brenda would actually be doing just fine. After 25 years of $52,000 annual withdrawals, and after the challenging 2000’s decade, she would still have $750,000.

Last, let’s look at a “median” scenario encompassing the past 60 years of American investing. I’ll start the analysis in 1964 and run it through 2024.

Your eyes don’t deceive you.

- After 20 years, Brenda would have $1.76M (and would have collected $52,000 per year all along).

- After 40 years, she’d have $11.4M (plus $52K per year).

- And after 60 years (from 1964 to today), she’d have $49 million dollars.

What a range of outcomes.

In the worst scenario, Brenda’s lump sum would have expired after 20 years.

But avoiding those awful outcomes, it’s highly likely Brenda would have created generational wealth. (I think it’s fair to call $50M “generational wealth.”)

Case 2B – Comparing Rates of Return

Before we even start comparing rates of return, we should expect similar results to Case 2A. If a particular scenario runs out of money, we expect its rate of return to be bad. If a scenario turns $1M into $49M, we expect its rate of return to be good.

Our “Great Depression” scenario from before had a 20-year annualized return of 3.0% per year, including a terrible starting sequence of (-12.1%) per year for the first 4 years.

Our “$49M” scenario saw 8.7% returns for 60 years.

If Brenda knew she was getting 3.0% annualized returns, she would pick the $1000 per week every time.

And if Brenda knew she would receive 8.7% returns for 60 years, maybe she would have chosen the lump sum.

Case 3 – Treating Brenda’s Winnings Like a Retiree

How would a retiree approach this problem, where they want to “create” $52,000 in annual income, forever, from a $1M portfolio?

I’d start with goals-based asset-liability matching. We’re going to take the near-term years and match them to low-risk bonds, then begin adding risk (in this case, stocks) as those liabilities extend into the future.

You can choose your own preferred risk tolerance here. I’m giving you an overly simple framework below:

- I’ll be matching Years 1-6 to 100% bonds.

- …Years 7-12 to a 50/50 mix.

- ….and Years 12+ matched to 100% stocks.

Each asset mix has its own discount rate / expected rate of return. We use those rates to allocate today’s $1M lump sum. I’m using 4.8% for bonds (just as before) and 8% for stocks. I’m going to use the 30% tax rate on any capital gains and income, just as before.

For the full picture, here’s the Spreadsheet.

In brief:

- We earmark ~$435K to cover the next 10 years of $52,000 annual outflows.

- …and then earmark ~$224K to outflows from years 11-20.

- …$108K to cover outflows from Years 21-30

Hopefully, this makes intuitive sense. For Brenda to have $52,000 in the year 2060, she doesn’t need $52,000 today. Instead, I’d argue she only needs about $5000 today, plus 35 years of compounding. That is the core of asset-liability matching.

We conclude that the $1M lump sum could cover all of Brenda’s $52,000 per year requirements, net of all taxes, for the rest of her life (and technically, until the end of time. It’s another asymptote!). She would still have ~$150,000 left over to do anything she wants with.

This, to me, is a better outcome than Brenda’s chosen annuity. This process is a terrific approach to retirement modeling, too.

But still – should Brenda put her trust in financial modeling and historical backtests? Or, should she just trust that Canada will pay its bill?

If we’re being honest and fair, Brenda’s decision was not clear-cut. Where other critics see, apparently, black and white, I see nothing but gray.

Brenda, je te soutiens et te souhaite bonne chance!

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

Suppose Brenda invested the 52000 rather than spending it. How long before the annuity is worth more than the lump sum?

Hey Max –

By your same logic, I think we’d have to also answer, “Suppose Brenda invested the lump sum forever and never invested it at all. Could the $52,000 per year ever catch up with the lump sum?”

The answer is, “It would ALL depend on the sequence of investing returns that you assume.”

I’d take the $1,000 a week. My reasoning is that it affords the mental freedom to, A: not work, and live freely and frugally, in a kind of Portlandia ideal. Probably not the realistic option for most. 2: live and work knowing your stable asset mix is covered for life, which is a great relief to many, and invest ongoing assets as aggressively as possible.

Being (fairly) financially independent at age 20 without having to lie awake worrying about downside risk is a big psychological and emotional benefit. I’d argue it might spread to everything in her life, boosting optimism, outlook, and opportunities.

But that’s me. Cover that base and move forward with peace of mind.

Good reasoning, Andy. Makes sense to me.

Before making a decision, I would write down where I am in my life, what I expect or want my future to be and what my risk tolerance is. Then I would call Jesse and ask him to help me make the decision. Having flexability in your life options is wonderful and she just acquired it.

Cheers Hank, thanks for writing in!

LA vie. C’est la vie. 😉

Oui oui, merci!