Don’t miss an episode of our podcast, Personal Finance for Long-Term Investors. Available on all podcast players.

Here’s the latest episode:

With all this ink being spilled over the 50-year mortgage proposal, we’re reaching an asymptote.

Seriously.

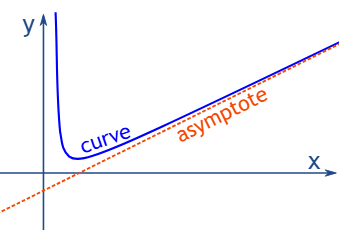

An asymptote is “a line that continually approaches a given curve but does not meet it at any distance.”

Technically speaking, the blue line below never touches the red one, but the gap between them gets infinitesimally small, approaches zero, and might trigger your inner Isaac Newton to invent calculus.

And in the purest mathematical way, mortgages eventually hit their own asymptote. Long-duration mortgages become identical to infinite (aka interest-only) mortgages.

In my mortgage scenario above ($500,000 borrowed at 7%), the difference between a 50-year payment and an infinite, interest-only payment is:

- 50-year monthly payment = $3008

- Infinite monthly payment = $2916

That’s a 3% difference in monthly payment. So let’s cut the B.S. They’re the same thing.

It’s semantics. “Paying a 50-year mortgage” already exists in our economy. We call it “rent.”

Rather than institute the 50-year mortgage, just skip to the real ending point: an infinite, interest-only mortgage. The lender is a landlord and owns the property outright forever. The resident is a renter. Equity in the home is never transferred.

As consumers, our choice then becomes clear.

If you want to build equity, choose a 30-year mortgage (or less). At my chosen 7% interest rate, the 30-year mortgage is 14% more expensive than the infinite mortgage. The 15-year mortgage is ~54% more expensive than the infinite mortgage.

If you don’t mind never owning your home, choose an infinite mortgage.

The 50-year proposal is too close to the asymptote to make any sense. Just make it interest-only and move on.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

Thanks for this great explanation! And for teaching me a new word 😉

You’re very welcome, Janet! You’re now one word closer to the asymptote of learning the complete English vocabulary!

We almost had an infinite mortgage.

We bought our first house in 1976, then moved and got a new mortgage, then moved-new mortgage, and repeat 5 times.

About seven years in on our last one, we started playing the refinance game, and then again three years later. We were tempted again in the 2020’s.

We became empty nesters and focused on our payoff during our first year of retirement.

So, after almost 50 years of payments, we were done.

Yeaaaaaa……this was a political posturing move. Its a better deal for lenders and banks than individuals.

Given that average home ownership tenure is 12 years (admittedly it bounces around a little, has been as low as 7 year or as high as 13/14 year like in 2020)….it is exactly what you say it is….interest only. Might as well do a balloon payment mortgage if that is where your head it at.

Honestly, I wish I had more exposure to “big picture” financial planning” as a young man, I would have done a 15 or 20 year mortgage for my first home. Sure, it would be tougher that first 0-3 years, but that kind of pressure incentives you to be resourceful when you are young.

Now I am over 40, I would never consider a 30 year mortgage at almost any rate. Reason is, I want to be done at SOME point. There is SOME validity to holding a mortgage with a certain mix of variables (if rates are low, you have a high home office expense you write against your business, market is down AND you have a strong emergency account and stable employment)…so I am not 100% anti-mortgage for more financially stable people (not Dave Ramsey here)…but have SOME light at the end of the tunnel and ASSUME your preferences WILL change over time as you age (most likely to have more simplified and conservative financial management). A 50 year mortgage is a trap for those with financial ignorance sadly, and a 30 year mortgage is just a milder trap.

30 year mortgages might be good for those in HCOL areas or first time home buyers, but there should be a stigma against getting your 2nd, 3rd, 4th homes with 30 year mortgages.

Great take, it really puts the words and mathematical structure to the way the concept of a 50 year mortgage made me feel.

Many thanks, Tim! Hope all is well w/ you and Gwen.