After 8 months in financial planning, one of my top 3 favorite conversations is explaining to a potential client when they’re not a good fit. It’s not me, it’s not you…it’s both of us.

Would you rather listen to this? I discuss this article in Episode 40 of Personal Finance for Long-Term Investors (formerly The Best Interest Podcast), below.

Sometimes it’s awkward. But it’s always transparent and usually welcomed in earnest. I might refer them to another planner who’s better equipped. Or I might just say, “Hey – just start a budget and read these books.”

This will piss off some advisors. Not everyone needs professional financial help.

I use the following analogy to explain why.

Dining Out, Grocery Stores, and Gardens

We all eat a little bit differently.

Some people never cook. They burn burgers and overcook eggs. The whole endeavor is too time-consuming, from prep to clean-up. They prefer to dine out as much as possible.

Others enjoy cooking…at least, somewhat. They have a balance between cooking and dining out. They shop for groceries and prep food, and save a lot of money.

Other people grow such immaculate gardens they don’t grocery shop at all. Their chickens lay eggs, their cows make milk. They are completely self-sufficient.

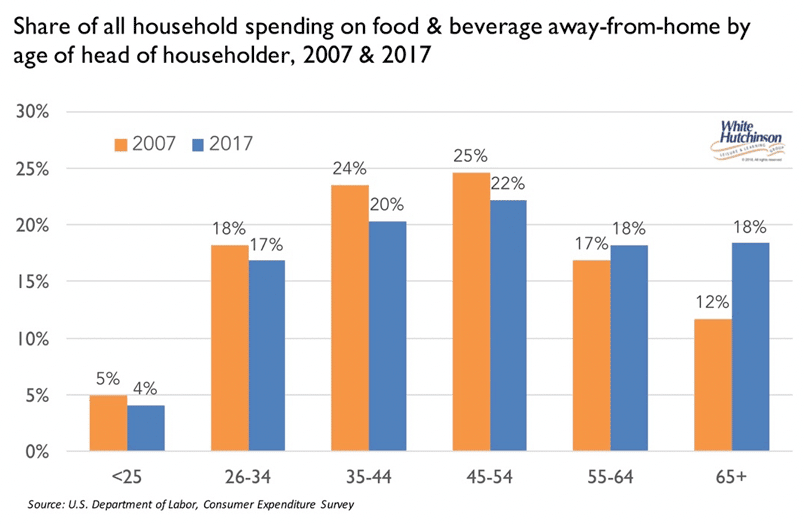

Most of us fall somewhere on this spectrum. But we aren’t stagnant. Americans, for example, cook their own ramen as young adults, only spending ~5% of food/beverage money away from home. But that number jumps to over 20% in our 30s and 40s. As life changes, so does our diet.

Financial planning and wealth management work the same way.

Different Money Habits

DIY investors are gardeners. Their shelves are full of personal finance books (but not Kiyosaki, I hope). They develop and enact their own investing systems. They self-study retirement planning, tax efficiency, estate planning, etc. They are nerds! They are completely self-sufficient and go far on it!

Financial planning clients dine out much more than the gardeners. They might know how to cook, but prefer not to. They expect expertise though, just as you would from a gourmet chef.

Or perhaps they are 50/50 between cooking at home and in the restaurant. “Help me with some stuff, but not all of it.”

And yes – there’s a fee for those professional services! We’ll come back to that…

Like the food analogy, there’s a spectrum.

Most people I speak with fall into one of three camps:

- They’ve always been gardeners (a Constant Gardener?), but aren’t sure they want to stay gardeners forever.

- They’ve always been in the middle, 50/50. But as their lives get more complex, “cooking” becomes more complicated and easier to screw up.

- They’re starving. That is, they’ve never considered the world of personal finance and investing whatsoever. Food? Investing? What are those?

Some “starvers” need the simplest directions: here’s a grocery list, boil that water, and stick these seeds in the dirt. In financial terms: create a simple budget, learn investing basics, and follow the financial order of operations. They don’t need professional help! They need the free basics.

But other folks – even the most self-sufficient – decide to dine out to make their lives easier.

That might mean hiring an hourly financial planner. A few hours once a year (just one meal out!) and they’re ok to go back to DIY self-sufficiency.

Others want to hang up the spade altogether. The complexity of their situation (and downside risk if they screw it up!) leads them to seek out comprehensive wealth mangement.

But…what is comprehensive wealth management? Or put another way: how can you tell you’re going to a worthwhile restaurant?

They Better Be Good!

If you’re paying someone to cook your dinner, they better be better than you. The problem with finanical services, though, is that there isn’t a Yelp to see ratings.

I put together 12 questions you should ask a financial advisor before you even think of working with them. I was inspired by Jason Zweig’s version of 19 questions. When you use these lists, some of answers you hear will shock you.

My 12th question is:

“What’s your value proposition? In other words, why is your cost worth it?”

It’s such an important question because (from the original article):

If your advisor only invests your money, that’s a bad value proposition. (This is similar to #5 in this list.)

Why?

Because the average advisor provides average returns. That’s just math. And you can seek out average returns on your own. Why pay for average returns?

A worthwhile advisor, however, provides significant value through:

- Financial planning

- Retirement planning

- Goals-based investing

- Investment withdrawal strategies

- Systematic rebalancing

- Tax-efficient investing and withdrawals

- Asset allocation

- Asset location

- Behavioral coaching

- Stress reduction

- Financial education

- Tax-loss harvesting

- Unique/private investing opportunities

…all of which is stuff that you might not know how to do on your own.

Some advisors provide a few of these services. Some provide all these services.

Some of these services directly save you money. Others save time. And some simply reduce your stress levels.

The important goal is that your advisor provides value in return for the fees you pay. Investment management isn’t enough.

Would You Like To See Our Dessert Menu?

You don’t want to pay $50 for an average steak and soggy pommes frites.

You might be a gardener or a Ramen cooker. You might stay that way or your circumstances might change.

If you decide to seek out professional finanical planning, ask yourself:

- What kind of help do I need? What responsibilities do I want to keep doing myself?

- Am I getting my money’s worth on this “meal?”

See you at the buffet (…Buffett?!)

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!