In 2002, Warren Buffett wrote:

Charlie [Munger] and I are of one mind in how we feel about derivatives and the trading activities that go with

Warren Buffett

them: We view them as time bombs, both for the parties that deal in them and the economic system

Not to mince words, Buffett has also called derivatives, “financial weapons of mass destruction.”

Then in the 2007 Berkshire Shareholders’ meeting, Buffett shared how derivatives hide leverage in the financial system, and the combination of the two is the real cause of “financial mass destruction.”

What are derivatives? What is leverage? Why should it matter to small fish investors like you and me?

Derivatives and Leverage 101

Derivatives, quite simply, derive their value based on the price movement of a different asset.

It’s like a sports bet. The actual competition between the Lakers and the Celtics has NBA implications. But bets (with real financial implications) can derive their value from the outcome of the game.

Leverage is borrowed money that’s used to invest. Just like a lever arm helps us lift more weight than we otherwise could, financial leverage gives us more money to invest (and earn more profit) than we could on our own.

Simple example:

- You have $10,000

- You convince a bank to let you borrow $100,000. You are levered 10-to-1.

- You invest the full amount.

- Your investment goes up 5%. You’ve turned $110,000 into $115,500.

- The bank charges you a small borrowing fee…$500…and you give them back the $100,000 loan.

- You’re left with $15,000….a 50% return on your original capital! You levered a 5% investment gain into a 50% total return.

But what if the investment went down 5%?

- …Your investment goes down 5%. You’ve turned $110,000 into $104,500.

- The bank charges you a small borrowing fee…$500…and you give them back the $100,000 loan.

- You’re left with $4000….a 60% loss on your original capital! You levered a 5% investment loss into a 60% total return.

The physics analogy holds. The same leverage that boosts your portfolio can catapult it away.

Neither derivatives nor leverage is free. Both involve counterparties who are charging/paying a fee. When you borrow mortgage money from your bank, you pay them interest. This is the same exact thing.

But how can these simple instruments be weapons of mass destruction?

The Danger of Derivatives and Leverage

Buffett went on to write in 2002:

The range of derivatives contracts is limited only by the imagination of man (or sometimes, so it

Warren Buffett

seems, madmen).

Derivatives are often complex bets involving huge sums of money. The following explanation from The Big Short is frighteningly accurate.

Bets on bets on bets that “transform an original $10 million investment into billions of dollars.

Warren Buffett pointed out that this creates an incentive problem in accounting. Namely, if we both think that we’ll win our bet (even though only one of us can possibly win), then neither of us will accurately account for our downside risk. We’ll both be too optimistic in our accounting. And when repeated and multiplied over thousands and thousands of bets, Wall Street ends up trillions of dollars too optimistic.

…until the music stops.

But the parties to derivatives also have enormous incentives to cheat in accounting for them. Those who trade derivatives are usually paid (in whole or part) on “earnings” calculated by mark-to-market accounting. But often there is no real market…and “mark-to-model” is utilized. This substitution can bring on large-scale mischief. As a general rule, contracts involving multiple reference items and distant settlement dates increase the opportunities for counterparties to use fanciful assumptions…In extreme cases, mark-to-model degenerates into what I would call mark-to-myth.

Warren Buffett

The 2007-2008 Great Financial Crisis was caused by derivatives and leverage. The long explanation is here. The short explanation is:

- Mortgages were turned into bonds.

- Derivatives were sold against those bonds. “If a bond goes to zero, you pay me a lot of money.”

- Many of those derivatives involved leverage. “The bond might only be worth $1 million. But if it goes to zero, the derivative contract pays me $10 million.”

- Neither party in the derivatives was accounting for them fairly (Buffett’s “mark to myth”)

- And when the bonds did fail, many firms had far too few assets to cover their derivatives debts.

Here’s Professor Brad DeLong discussing the ’07-’08 financial crisis on the Odd Lots podcast:

And it was the fact that [mortgage derivatives] were held by guys who were leveraged 40 to 1, you know, as their core reserves that made a simple crash of an asset into an enormous interlinked chain of bankruptcies where at the bottom no one is sure they’re solvent because everyone has so much counterparty risk, they do not understand that everyone pulls into their shells and sells what they can and otherwise hunkers down.

Brad DeLong

Solvent? Counterparty risk? Most major players in ’07-’08 found themselves thinking,

Firms A and B owe us big money. And we owe Firms C and D. But if we don’t get paid by A and B, we’re insolvent and going out of business. So we can’t pay C and D until we’re sure we’ll survive.

Thus, the global economy freezes. Financial weapons of mass destruction.

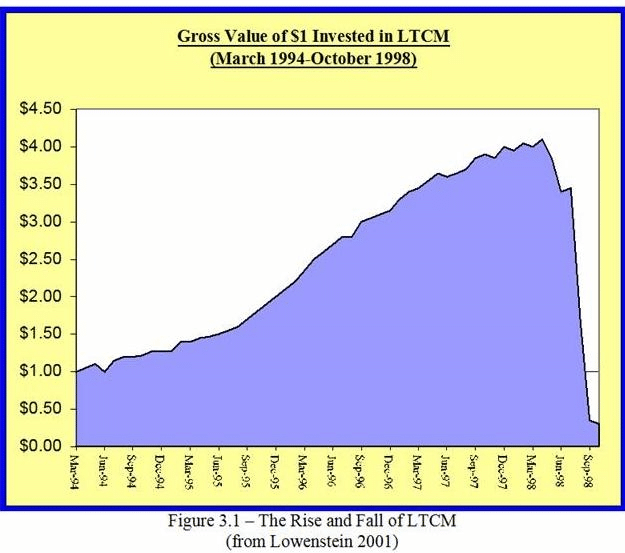

I recently finished When Genius Failed by Roger Lowenstein, chronicling the rise and fall of Long-Term Capital Management (LTCM). Long story short, LTCM failed because their leveraged derivatives eventually stopped working in their favor, and did so catastrophically.

LTCM – a firm of ~190 employees – had serious effects on the global economy.

Why does any of this matter to you?!

My first-level thought is: don’t mess around with leverage or derivatives. You don’t need them! Most investors don’t understand them anyway. Just avoid them.

The second-level thought is: if you don’t have an opinion on leverage and derivatives, you probably shouldn’t like them. We’ll explain why below.

But the deeper lesson is: be aware they exist and don’t let their destruction scare you.

Public markets are similar to casinos. We’re using the same chips, the same cards, the same dice. We’re all trading stocks and bonds, right? Some of our games differ, as do our bet sizes. But to the untrained eye, it appears we’re all playing the same games.

But I disagree. Some of us are playing slow-and-steady games with the odds in our favor. Others are playing flashy games with huge sums of money. Worse yet, some people are borrowing (leverage) and making side bets (derivatives).

When the flashy, levered, derivatives bets go bad, it can feel like the whole casino is crashing around you. Huge sums lost. Gamblers entering default. Should you cut your losses are run for the door? It’s completely human to panic.***

No! You’re playing a different game than them. You still own your chips. Your process has been working. The casino is still afloat.

***And for this reason, many people (including Buffett and Munger) think derivatives and leverage should be limited by law. These instruments almost took down the global economy in 2008. The casino almost wasn’t afloat anymore. That’s scary stuff.

Yes, their leverage and their derivatives affect what you see, hear, and feel. But the chaotic sideshow is over there. They’re losing their money. You can carry on.

Many investors don’t realize this. They assume they’re playing the same game as everyone else. So when everyone else runs to the door, they run too. But investing doesn’t have to work that way.

You and I can play our slow and steady game, keep calm, and carry on.

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

Re:blog post on derivatives.

Jesse, I’m not sure I agree with you on ignoring the huge derivatives crashes. As you noted, the LTCM and subprime CDOs almost caused the whole casino to fail. The failure of huge leveraged derivative bets does matter to everyday investors if the financial system and global economy are put in serious jeopardy.

I think the lessons are more akin to guarding against black swan events: larger emergencies funds, perhaps a futures fund that can profit in declining markets (I personally use BLNDX for that purpose).

Thanks again for your reliably thought provoking posts.

Regards,

Chris Viscomi