One of the core tenets of financial literacy is keeping a tidy budget. But a common question in creating a budget is how many budget categories are required?

The Pros and Cons of Budget Categories

Your budget categories help you fine-tune your spending data to make smart spending changes in the future.

Whenever you create a new budget category, you should be asking, “Do I care about this budget category so much that I might want to adjust my spending behavior in the future?“

Let’s look at housing costs. They seem important to track. And considering they typically account for 30% of the average American budget, it’s definitely a budget category that is ripe to be improved upon.

For me, housing costs are a category where I want to understand changes over time. If you’re like me in that way, then you should have a budget category for housing.

But should just one category track all of your housing spending? Or should it be divided up across multiple categories? Without trying hard, I can think of: rent/mortgage, property tax, maintenance, and home improvements. There are myriad expenses associated with maintaining a home, and they could all be tracked independently in your budget.

It all comes down to personal choice. It’s a balance between your desire for data vs. your preference for simplicity.

Personally, I have two budget categories here. One category represents my normal monthly mortgage payment, including the loan repayment, interest, insurance, and taxes. The second budget category is for home maintenance—all expenses associated with maintaining and improving my home, both inside and out.

More Data, More Options, More Hassle

Budget categories provide you with data. That data helps you understand your mind and your spending habits. And in the long run, that additional data will help you improve.

But more data is also a hassle. It requires more time, more dedication, more effort. With too many options, humans tend to freeze up. This is the so-called ‘analysis paralysis’ or the ‘paradox of choice.’ It’s why Costco serves a limited number of options to its customers.

Just think about basketball stats. Comparing players would be easiest if all we cared about were points scored—one category, nothing more. More points equate to a better player.

Enjoying this article? Subscribe below to get new articles emailed straight to your inbox

While this correlation is partially true—more talented players tend to score more points—it’s far from perfect data. If we collect more stats, like rebounds and blocks and steals, we’ll surely get a more complete picture of each player’s value.

The same idea applies to your budget. Less data is simpler, but more categories provide a finer picture of your financial status.

Should you track normal groceries for typical trips to the store and special groceries when you throw a party and dining out when you eat at a restaurant? Or does it all fall under the umbrella of one category: food?

You have to find your preferred balance between too much data and too little data.

But here’s what I do and what some experts I spoke with do.

What Do Experts Do?

I asked my Twitter followers what they do, and about 70 responded. Keep in mind—these folks are fairly “money-minded,” but so are you if you’re reading this today!

40% of the respondents use between 1-8 categories. 30% use between 8-16 categories. And the remaining 30% use more than 16 categories.

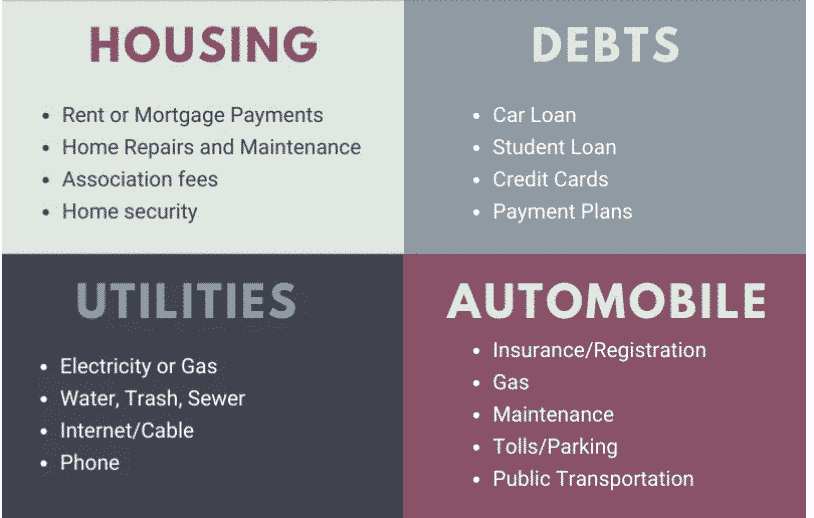

What categories should you use? Almost all budgeters divide up their budget into a few high-level budget categories:

- Stable monthly bills (e.g. mortgage or rent)

- Variable monthly expenses (e.g. groceries, electric bill)

- Sinking funds—expenses that don’t occur every month, like car repair (which might run you $1K-$2K per year over the life of the car)

- Fun stuff/wish list—a place to put long-term savings for future fun (like a vacation)

But those high-level budget categories aren’t where the nitty-gritty details go. Below the high-level categories sit detailed sub-categories.

Personally, I use 29 detailed budget categories (I’ll list them at the end of the post). These include traditional categories like groceries and mortgage and include unique categories like blog expenses and dog stuff.

Every dollar I spend gets associated with one of those 29 categories.

But let look at a great example of where I could (and maybe should) consolidate my categories. I have separate categories for my water bill, my gas/electric bill, and my internet bill. I bet that 95% of people out there think I’m dumb and should just use one Utilities category instead. I get it! That makes sense!

A good starting point is to shoot for the vicinity of ~10 budget categories. Here are the categories of one such budget example that someone emailed to me:

- Housing

- Food

- Utilities & Monthly Bills

- Transportation

- Consumer Goods

- Fun

- Debt Repayment

- Gifts & Charity

- Investments

- Long-term Savings

I think this is a great place to start. Each of these budget categories could be broken down further. For example, transportation can be separated out into car payments, fuel, and maintenance. It all depends on how much data you want.

What Are Your Budget Categories?

How many categories are in your budget? What’s the most unique category you use? Let me know in the comments below!

Thank you for reading! Here are three quick notes for you:

First – If you enjoyed this article, join 1000’s of subscribers who read Jesse’s free weekly email, where he send you links to the smartest financial content I find online every week. 100% free, unsubscribe anytime.

Second – Jesse’s podcast “Personal Finance for Long-Term Investors” has grown ~10x over the past couple years, now helping ~10,000 people per month. Tune in and check it out.

Last – Jesse works full-time for a fiduciary wealth management firm in Upstate NY. Jesse and his colleagues help families solve the expensive problems he writes and podcasts about. Schedule a free call with Jesse to see if you’re a good fit for his practice.

We’ll talk to you soon!

**If you’re interested, my 29 categories are: Mortgage, Annual Bills, Car Insurance, Gas/Electric, Dog Stuff, Water Utility, Internet, Charity, Streaming Services, Blog, Dining Out, Bars, Other Fun Money, Groceries, Gas Money, Stuff I Forgot to Budget For, Future Rental Property, Brokerage Account, Roth IRA, Home Maintenance, Medical, Gifts, Clothing, Auto Maintenace, Emergency Fund, EuroTrip, [TBD Secret], Summer Fun, and a couple now extinct categories.

Hi Jesse – Since I’m 4 years from retirement, I’m keeping things simple with only 6 categories (5 essential & 1 discretionary): home, transportation, grocery, healthcare, and other are my 5 essential categories and then discretionary (travel, entertainment, restaurants, hobbies, pets, etc…).

I’m doing this because my pension and social security will cover my essential expenses and my investments will cover my discretionary. Each year I’ll provide myself with a certain amount of discretionary spending and I’ll stay within that amount, regardless of how I spend it.

I had more categories as I was trying to get my expenses identified and under control but I’m not needing that now. Thanks for the article.

Hey Scott, thanks for writing in.

First, very exciting that retirement is around the corner. It’s still a blip on the horizon for me. Any big plans?

Second, that budget totally makes sense to me. Keep it simple. Perhaps you can tell me if you agree with this…

As we get used to budgeting and develop smart spending habits, the true need for a budget (i.e. to identify overspending) diminishes.

We don’t overspend! We’ve developed better habits than that!

So why make it any more complicated than it needs to be?

Thanks again for writing in.

Best,

Jesse

I completely agree with your assessment. At first, we wrangle our expenses to get control and understand where our money is going. As we get a handle on it, we find waste and redirect those dollars toward savings or debt. Eventually, you continue to simplify until you get to retirement.

My retirement thesis is simple, before we can even consider retiring we need to what expenses will keep us alive and well … trying to keep those expenses on par with our essential lifestyle. I call these essential expenses. Once we have those identified and covered (pension, annuities, social security, savings, etc…), we can consider what fun might look like in retirement. And the more fun I want to have the more miney I will need for discretionary expenses. I don’t care about discretionary categories because it’s all fun and spent only after you essential expenses are covered.

Those are my thoughts. Stay fluid and continue improving your process.

Good luck!

I don’t really have a budget. I just track my expenses, my worksheet only has two categories

Necessary and Discretionary. Currently there are 18 sub categories under “Necessary” and 8 under “Discretionary” The sub categories can change over the years for example we just removed the Necessary Orthodontist sub category as we completed our final payment for the kid’s braces.

Having these two main categories allows you to quickly see your your lean FIRE expenses(25x Necessary) and your normal FIRE expenses(25x total Expenses). Having years of personalized expenses and the sub categories lets you dive into your numbers and see where you money goes year over year. I think only us nerds like doing this kind of thing. I can tell when showing my wife our numbers how her eyes glaze over. 😉

Hahaha yes – I agree that “nerds like us do things like this”

100% agree, Tech!

Can you share your 29 categories?

Sure thing Ronil. I added them to the end of the post.

Thanks for reading!

-Jesse S

Thank you. Here are our categories I have used. 25 in total.

Type

Principal + Interest, Extra Principal, Homeowners Association, Edison, Water

Sewer/Trash, So Cal Gas, Cell Phone Bill, Internet, Taxes, Home Insurance

Auto Insurance, Umbrella Insurance, American General Life Ins,Protective Life Insurance

Amazon Prime, Medical, Banfield Plan, Hulu, Ronil, Rachana, Online/Misc,Food

Pet,Gas